Table of Contents ![]()

3 Tools of Monetary Policy

What are Monetary Tools

In the developed world, central banks decide monetary policy. The US has the Federal Reserve, the UK has the Bank of England, and the EU has the European Central Bank. In general, these are independent institutions, free from political interference. However, that does not necessarily mean political factors do not influence decision making.

Monetary policy is made through three main channels: open market operations, the discount rate, and the reserve requirement. With that said, there are many other tools that they have at their disposal. But the purpose here is to look at the main tools and those that are most commonly used.

Key Points

- Monetary policy refers to the control and supply of money in the economy.

- Central banks create and dictate monetary policy.

- The main three tools of monetary policy are – open market operations, reserve requirement, and the discount rate.

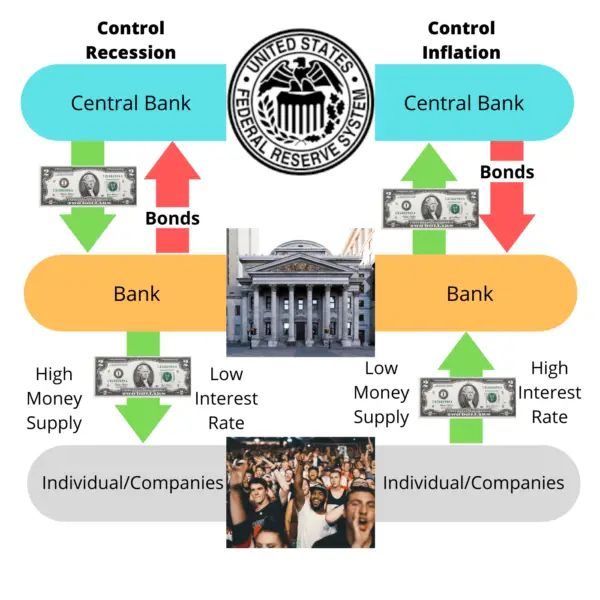

During periods of inflation, monetary policy becomes increasingly important. Central banks will increase interest rates to slow the flow of money with the aim at reduction inflation. At the same time, it may consider reducing its stock of government bonds/gilts in order to reduce the amount of cash within the economy. There are many types of monetary policy central banks can use, but will depend on the specific circumstances the nation finds itself in.

1. Open Market Operations

One of the main tools of monetary policy is Open Market Operations, which refer to the buying and selling of financial instruments by central banks. For instance, the Federal Reserve purchases:

“Holdings of Treasury, agency, and mortgage-backed securities; discount window lending; lending to other institutions; assets of limited liability companies (LLCs) that have been consolidated onto the Federal Reserve’s balance sheet, and foreign currency holdings associated with reciprocal currency arrangements with other central banks (foreign central bank liquidity swaps).”

These financial instruments are also known as securities. Central banks purchase these from private banks by creating money and adding it to the banks’ central reserves. These reserve accounts are like our current accounts. The central bank buys securities from private banks and puts money in their reserve accounts.

If we compare this to real life, it’s a bit like selling your old car and the customer transferring the money to your account. The main difference being that the customer essentially creates the money from thin air.

So, when central banks purchase securities from private banks, money goes into their reserve account. In turn, these securities are added to the central banks’ asset sheet, whilst private banks now have the extra cash flow to use for other means.

What does this mean and what is the purpose?

When the central bank buys securities, we call this an expansionary monetary policy. This is because it is expanding the money supply. So, when it adds money into private banks’ reserve accounts, it is creating money. In turn, they have more money to circulate throughout the economy. Meaning there is more money to lend and invest.

Open market operations have the potential to cause inflation, so central banks must exercise extreme caution. They normally take place during periods of economic decline, with the aim of boosting the money supply and decreasing its value.

“Open market operations have the potential to cause inflation, so central banks must exercise extreme caution.”

Ultimately, the central bank provides liquid funding to private banks. The aim is for them to lend to businesses to create jobs and invest in the economy.

What we saw in 2008 was an example of open market operations, but on a scale unseen before. Also known as Quantitative easing, the Federal Reserve increased its balance sheet from $800 billion to over $4 trillion by 2019. The aim was to reduce the impact of the financial crisis and preserve aggregate demand.

2. Reserve Requirement

The second tool of monetary policy that a central bank has is the reserve requirement. This is a percentage each bank must keep when loaning out depositor’s funds. For instance, the reserve requirement may be 10 percent. So, if a depositor puts $100 into the bank, they must keep back $10 and are then allowed to lend out the other $90.

The reserve requirement is a regulation employed by most central banks across the world, although to varying extents. In turn, commercial banks must keep the specified reserve requirement to hand. So, this could be stored as cold hard cash or in their central reserve accounts. The point is so that they have enough money to meet the immediate demands of their depositors.

What does this mean and what is the purpose?

Central banks use the reserve requirement to expand and contract the money supply indirectly. It does this by requiring banks to hold more money on hand instead of lending it out. So rather than the money circulating around the economy, it is doing nothing in the bank’s vaults or account sheet.

“Reducing the ratio can increase the money supply and create inflation.”

When the reserve ratio is low, the more money banks can lend out. However, when it is high, it means the banks must keep more aside. In turn, this means less money circulating through the economy. So restrictive reserve ratios can reduce the money supply, meaning there is less money to reflect the goods and services that are being produced. This has the potential to cause deflation as there is less money in circulation.

The main purpose of controlling the reserve ratio is to allow central banks more control over the money supply. Reducing the ratio can increase the money supply, which in theory, should help boost aggregate demand in the economy. By contrast, increasing the ratio will reduce the money supply. Central banks may do so if inflation is getting out of hand. So, it is another way of controlling inflation.

3. Discount Rate

The final tool of monetary policy is the discount rate, which refers to the rate of interest the central bank charges to private banks. So, if they are unable to find enough liquidity from other banks, they will have to borrow from the central bank as a lender of last resort. For instance, a private bank may be unable to meet its liabilities and may require a short-term loan to cover it.

The Federal Reserve offers the discount rate in three formats: primary credit, secondary credit, and seasonal credit – each with its own interest rate.

Primary credit is extended to the most secure of financial institutions and receive the best rates. Secondary credit is available for those institutions that do not quite meet the same standards and offer greater risk. And finally, seasonal credit is extended to relatively small depository institutions that have recurring intra-year fluctuations in funding needs, such as banks in agricultural or seasonal resort communities.

What does this mean and what is the purpose?

By increasing the discount rate, the central bank makes it more expensive for banks to do business. It costs them more if they need a short-term loan, so the higher the rate, the more risk-averse banks become. At the same time, when the central bank decreases the discount rate, it makes it cheaper to borrow money. Both actions influence the money supply. So, a higher discount rate decreases the money supply whilst a lower rate increases it.

Related Topics

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Consumer Goods: Definition, Types & Examples - A consumer good, also known as a ‘final good’, is the end product a business produces and is purchased by…

Consumer Goods: Definition, Types & Examples - A consumer good, also known as a ‘final good’, is the end product a business produces and is purchased by…  Offshoring: Definition, Pros, Cons & Examples - Offshoring is where a business moves its operations abroad.

Offshoring: Definition, Pros, Cons & Examples - Offshoring is where a business moves its operations abroad.  Chi Square Test - The chi-square test is a statistical test used to determine if there is a significant association between categorical variables in…

Chi Square Test - The chi-square test is a statistical test used to determine if there is a significant association between categorical variables in…