How Does Quantitative Easing Work

What is Quantitative Easing

Quantitative Easing is where a nations Central Bank purchases financial instruments from the private sector. These are predominantly government bonds and mortgage-backed securities, although some Central Banks also include stocks as part of their purchases.

For example, the Central Bank of Japan purchased Y4.1 trillion ($37 billion) of stocks in 2019, whilst other Central Banks such as the Federal Reserve in the US limit its purchases to government denominated debt.

With that said, the vast majority of Quantitative Easing programs focus on purchasing long-term government debt. Central Banks will look to create money electronically and then use this money to purchase government debt from private institutions. This debt is then stored with the central banks who can then sell it back to the market at a later date.

Key Points

- Quantitative Easing is where the Central Bank purchases financial instruments from the private market – usually government denominated debt.

- It works by injecting money into private markets with the aim of that money filtering down to businesses and consumers.

- The main aims of Quantitative Easing are to control inflation, stabilise financial markets, and boost economic growth.

How Quantitative Easing Works

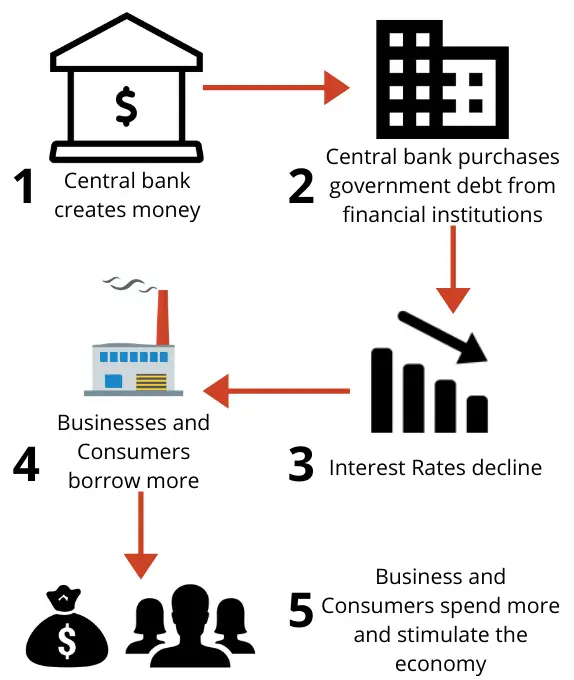

Quantitative Easing works in 5 sequential steps:

Source: https://www.iconfinder.com/

1. Central Bank Creates Money

The central bank creates money through an electronic process that adds funds onto its balance sheet. In a real-life example, it’s similar to adding an extra zero to your savings account.

2. Central Bank Purchases Government Debt

Central bank uses money to purchase government denominated debts such as bonds and gilts from financial institutions. This includes banks, pension funds, insurance companies, and foreign-owned entities. These assets are then transferred over to the central banks balance sheet where it is held as an asset.

3. Interest Rates Decline

Reduced interest rates occur as a result. This is because central banks purchase government debt which increases its price and reduces the yield. For instance, the government may borrow $1 million at 5 percent interest, earning $50,000 in interest per year.

On the market, it will sell for $1 million. However, this price can fluctuate based on demand in the market. So if there is significant demand, its price will go up. In turn, central banks significant purchases push the price of government debt up.

So in this example, it may increase its value to $1.1 million. However, the interest is still $50,000. In turn, this would reduce the real interest rate to 4.5 percent. At the same time, interest rates across the economy tend to fall in line with yields on government bonds.

4. Businesses and Consumers Borrow More

Business and people borrow more as interest rates fall. This is because the central bank depresses the interest rate of government bonds, which has a knock on effect to other forms of debt.

In turn, mortgages are cheaper, loans are cheaper, and businesses that are doing well can access cheaper credit to expand their operations. Therefore, they are actively incentivised to borrow and move purchasing decisions forward.

5. Businesses and Consumers Spend More

Businesses and consumers spend more, thereby creating jobs. As interest rates fall and borrowing is incentivised, consumers and businesses start spending and investing more. For instance, businesses may hire additional workers to increase production, whilst consumers may start buying more products.

Does Quantitative Easing Work?

The above flow shows how quantitative easing works in practice. However, it relies on a number of assumptions. First of all, it assumes that the financial institutions will spend the new money they have. As the central bank buys government bonds, it increases the amount of cash they have to lend.

Yet we did not see this during the aftermath of the financial crisis. Billions of US dollars, Euros, and Great British Pounds were put into the pockets of financial institutions. However, rather than lend these out, they were stored in their reserves with the central banks.

The reserve funds that banks have is the cash they have to meet sudden liabilities or a potential run on the banks. In other words, they were holding back the cash in case another crisis occurs. If we look at the reserves held in the US, they increased from $1.9 billion in August 2008 to $2.6 trillion in January 2015.

Over the same period, the Federal Reserve pumped $3.6 trillion into the system. Yet whilst some went through into other parts of the economy, the vast majority filtered into the reserve accounts of financial institutions.

So not all of the funds went into the wider economy. However, we cannot judge the success of quantitative easing by one example, nor on this factor alone. Instead, we are best to look at the aims of quantitative easing and whether these were achieved.

Aims of Quantitative Easing

It is important to judge quantitative easing based on meeting its set objectives. We cannot say that it has worked if it has not achieved the desired results.

1. Increase Economic Activity

Central banks resort to Quantitative Easing when the nation is facing a dire economic crisis. For example back in 1929, during the Great Recession, the Federal Reserve undertook a large bond buying programme to stem the worst recessions to date.

We also see a huge increase in government spending to try and boost demand within the economy. As the government borrows from banks, it takes money away from the private sector. In turn, that causes a natural decrease in business investment.

So central banks try and ensure private firms have enough access to capital by buying up government debt in order to free up cash to lend to the private sector.

At the same time, as interest rates decline, banks are more incentivised to lend to businesses as the rates are higher.

The aim is simply put by the Central Bank of England: “We aim to boost spending and investment in the economy”. It does this through making debt cheaper, thereby incentivising consumers to borrow at lower rates. At the same time, lower interest rates make it cheaper for businesses to invest and expand.

Does it Meet this Aim?

As with most questions in economics, it really depends. There are a number of other variables that can impact how effective quantitative easing is. For instance, consumers may not react in a way we would expect from lower interest rates. They may continue to save despite low returns.

With that said, quantitative easing is generally effective at boosting the economy in the short-term. It injects money into the system where there was none before. This transfers into the wider economy, although not all of this filters through. So whilst it can boost the economy, its effectiveness can vary.

For example, only 50 percent of the monetary stimulus may reach the wider economy. The overall economy will benefit, yet it’s not as effective as it could be if 100 percent filtered through. At the same time, if done incorrectly, it can cause long-term problems such as persistently high levels of inflation.

In conclusion, quantitative easing does benefit the economy in the short-term, but may present long-term issues.

2. Increase Inflation

Quantitative Easing is generally employed during periods of sharp economic decline. That means the demand for goods and services is in decline. As a result, deflation is likely to take hold as businesses react to falling demand by lowering prices.

Most central banks in the developed world target an inflation rate of 2 percent. So when the economy goes into decline, it signals that prices may also start to fall. In turn, central banks use quantitative easing to help bring back up inflation to the target rate by pumping money into the economy.

The reason for such is to prevent demand falling further. For instance, consumers may start to expect prices to continue to fall; thereby pushing their purchasing decisions back and deflating demand further.

Does it Meet this Aim?

Without doubt, quantitative easing causes inflation. When the central bank creates money, it is adding it into the economy in some shape or form. As more money is injected into the economy, it means there is more money that is representing the same number of goods and services that is produced.

Let us take a very basic example. If Nation A produces 100 bananas per year, with $100 circulating, then each banana is worth $1. However, if the central bank of Nation A creates an extra $50, there is now $150 in the economy, meaning each banana represents $1.50.

So quantitative easing naturally creates inflation. However, it relies on money circulating through the wider economy. As we saw in the aftermath of the 2008 Financial Crisis, money was injected into the system, but it got stuck in the Banks reserve accounts, with only a percentage of it reaching the wider economy.

In conclusion, quantitative easing is inflationary, but to what extent depends on whether and how it filters into the wider economy.

3. Lower Interest Rates

Interest rates are an important aspect of monetary policy. It effectively acts as a tap to release money into the economy. When interest rates are low and the taps are open, money is flowing into the economy and circulating.

However, in the same way, you don’t want to leave your tap on for too long at home, you don’t want to leave the monetary tap open for too long either. Left open for too long, and serious levels of inflation may occur.

Central banks aim to lower interest rates and open the tap for two main reasons: boost the economy, and increase inflation. So this third aim of the central bank is purely so it is able to meet its first two aims.

Does it Meet this Aim?

From the rounds of Quantitative Easing after 2008, interest rates hit rock bottom, although they were assisted by lower base rates. In turn, QE is significantly effective in reducing interest rates. It does so by buying government bonds, thereby increasing their value and reducing their effective yield.

In turn, the demand for bonds declines, and shifts demand to other financial instruments. We then see other asset prices rise and yields fall. This then filters into the wider consumer market for instruments such as mortgages and consumer credit.

In the US, the average mortgage rate before QE came in after the Financial Crisis, was 6 percent. However, it fell down to just under 4 percent by 2017 as the Federal Reserve tapered back on its purchases.

4. Stabilise the Market

In recent times, we have seen three major crashes in the stock market. First was 19 October 1987, otherwise known as Black Monday, the US’ S&P 500, and Dow Jones fell by over 20 percent in one day. We then had the 2008 Financial Crisis which saw the Dow Jones fall 18 percent in the week of October 6 – 10, with the S&P falling over 20 percent.

We recently saw the Coronavirus crash in 2020, which took off 36 percent from the Dow Jones between late February and March. The S&P also lost around 34 percent during the same period, with international markets crashing to a similar degree.

What central banks aim to do is stop asset prices from falling further and bring confidence to the market. Under such circumstances, the effects extend beyond stocks and into the realms of finance.

During major crashes, stock prices and confidence in big firms fall. In turn, corporate bond markets are also affected. So in order for a firm to take out a loan, it may struggle to find investors and if they do, the interest will be extortionately high. As a result, a lot of businesses that rely on short-term loans could struggle to survive.

So by injecting money into the market, central banks stabilise prices and restore confidence. As a result, businesses get greater access to credit and may be able to survive the turbulence.

Does it Meet this Aim?

Without a doubt, quantitative easing stabilises markets. For instance, in March 2020, the US’ Federal Reserve announced a $2 trillion stimulus package which boosted the Dow Jones by nearly 10 percent and the S&P 500 by around 8 percent.

With that said, the markets can also react unfavourably or un-movingly. For instance, the European Central Bank introduced a 750 billion Euro stimulus in late March. The markets reacted, but only marginally as the European market rose by 3 percent.

When markets are going crazy, traders and investors have a tendency to get stuck in a downwards spiral. Everything seems to be bad news for the markets, which depletes any confidence. As humans, they only naturally see the negative side, so the central bank looks to bring back some positivity to reassure markets that they will be supported whatever it takes.

Related Topics

FAQs on Quantitative Easing

Quantitative Easing works in 5 sequential steps:

1. Central Bank Creates Money

2. Central Bank Purchases Debt

3. Interest Rates Decline

4. Businesses and Consumers Borrow More

5. Businesses and Consumers Spend More

Quantitative easing creates money by purchasing government debt. The Central bank adds money onto its balance sheet and transfers it over the financial institutions in return for government debt. So although ‘money’ is created, none is actually printed.

Quantitative easing is not paid by anyone, however, if it results in inflation, then everyone in society will pay – particularly those with cash as it loses its true value.

Further Reading

Natural Monopoly: Definition, Characteristics & Examples - A natural monopoly occurs when there are high fixed costs meaning that it is unprofitable for more than one to…

Natural Monopoly: Definition, Characteristics & Examples - A natural monopoly occurs when there are high fixed costs meaning that it is unprofitable for more than one to…  Effective Annual Rate - The Effective Annual Rate (EAR) is the true annual interest rate that takes into account compounding effects, providing an accurate…

Effective Annual Rate - The Effective Annual Rate (EAR) is the true annual interest rate that takes into account compounding effects, providing an accurate…  Economies of Scale: Definition, Types & Examples - Economies of scale occur when a business benefits from the size of its operation. As a company gets bigger, it…

Economies of Scale: Definition, Types & Examples - Economies of scale occur when a business benefits from the size of its operation. As a company gets bigger, it…