Discount Rate in Economics

What is the Discount Rate

The discount rate is the interest rate by which the central bank charges commercial banks to borrow money or cover short-term liabilities. In other words, the central bank lends money to the likes of Goldman Sachs, and in turn, they pay interest of that loan. The interest paid is known as the discount rate.

Commercial banks have what is known as a ‘reserve account’. Essentially, this is money that they keep over to meet short term liabilities, such as consumers wanting to take money out. This is why after the financial crisis; commercial banks significantly increased their reserves.

Key Points

- The discount rate is the interest rate which the central bank charges commercial banks to borrow from it.

- Commercial banks tend to borrow from the central bank in order to cover short-term liabilites than it is unable to cover due to the level of illiquid assets it has.

Some countries have a legally enforced reserve requirement, which means commercial banks may need to keep 10 percent in their reserve accounts. In turn, banks may find that during their day to day trading, they may fall short of this requirement. They, therefore, require a short-term loan in order to cover the discrepancies.

Such a loan may come through the inter-bank market, or, through the central banking system whereby the discount rate is applied.

So commercial banks may use central bank loans and pay the discount rate to cover its reserves. However, they can also use it to lend to the final consumer, which, in turn, can influence the price of mortgages and credit card repayments.

The higher the discount rate, the higher the cost to commercial banks, which is then passed on to the consumer.

Discount Rate Explained

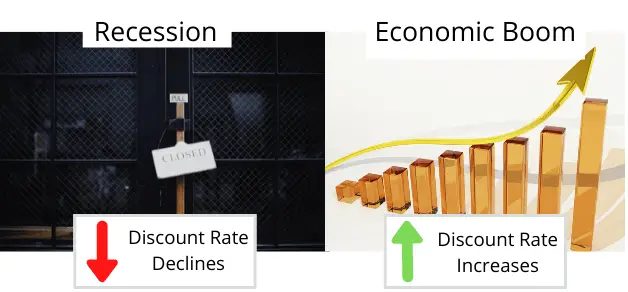

The central bank controls the discount rate. Usually, in periods of economic growth, the discount rate is higher than the inter-bank rates. In other words, the central bank wants to charge higher interest rates than commercial banks charge to each other.

The reason being is so that banks lend between each other rather than depending on central bank loans. When a commercial bank takes a loan from the central bank; it is effectively introducing new money into the economy. If done on a large scale, it has the potential to contribute to inflation.

So central banks keep the discount rate higher than the inter-bank rate during periods of economic boom. However, during periods of recession, they tend to want to expand the money supply and increase its circulation.

The reason is twofold. First, central banks want to stave off deflation. Normally, a recession period comes with unemployment and declining consumption. What can result is falling prices as businesses seek to attract consumers in a struggling market.

So by lowering the discount rate, banks have access to cheaper levels of credit. In turn, this creates cheaper credit for both consumers and businesses. By encouraging greater spending in the economy, it is able to stave off deflation. Which brings us onto the second reason.

Central banks lower the discount rate to boost economic activity. By creating lower rates for businesses, they are actively incentivised to invest. So a more efficient machine or other capital equipment may become much cheaper.

At the same time, consumers don’t have to pay so much back in interest. Whether this is a mortgage or consumer loan, they have a greater level of disposable income. In turn, this can filter into the wider economy as consumers spend that extra income that would have previously go on interest.

Discount Rate vs Interest Rate

It is easy enough to get the discount rate and interest rate mixed up. The difference is that the interest rate is what is charged to the final consumer for borrowing money. This compares to the discount rate that charges interest to financial institutions for borrowing from the central bank.

We can look at it as a chain. Financial institutions borrow money from the central bank at the discount rate. Then, they lend money to the consumer based on the interest rate that they charge.

As a result, the discount rate can have an impact on the final interest rate charged to consumers. The higher the central banks’ discount rate, the more banks have to pay to borrow money, which in turn means higher costs to the consumer.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Chi Square Test - The chi-square test is a statistical test used to determine if there is a significant association between categorical variables in…

Chi Square Test - The chi-square test is a statistical test used to determine if there is a significant association between categorical variables in…  Examples of Socialism in America - In America, examples of socialism include the New Deal programs, progressive taxation and social welfare policies, public education and healthcare…

Examples of Socialism in America - In America, examples of socialism include the New Deal programs, progressive taxation and social welfare policies, public education and healthcare…  EBITDA: Definition, Pros, Cons & Example - EBITDA stands for Earnings Before Interest, Tax, Depreciation, and Amortization.

EBITDA: Definition, Pros, Cons & Example - EBITDA stands for Earnings Before Interest, Tax, Depreciation, and Amortization.