Economics: What is Economics, Types, Systems

What is Economics

Economics is the study of scarce resources that have alternate uses – looking at how best to deploy those resources. This covers the production, distribution, and consumption of goods as well as how individuals, businesses, and governments interact to allocate those resources efficiently.

This is done through two main branches – macroeconomics, and microeconomics. First of all, macroeconomics focuses on factors that impact on the whole of the economy, such as, interest rates, economic growth, and unemployment. We can look at macroeconomics as the study of resources on a nationwide scale.

Second of all, we have microeconomics, which looks at individual actions and incentives. For instance, what impact does increasing the price of product A have on its demand? Common topics include supply and demand, the elasticity of demand, and market failure.

Key Points

- Economics is the study of scarce resources that have alternate uses.

- In economics, the three main factors of production are crucially important – they are labour, land, and capital. Economics studies how these come together to create an output.

- There are two main categories of economics – microeconomics and macroeconomics.

Economics itself is known as a social science, even though it does not resemble a science. For instance, it is impossible to conduct any scientific experiments as the economy is constantly evolving. We can never conduct a test with a single independent variable. Everything is constantly changing and evolving – which means economics is never an open-closed case.

For example, if we look at the minimum wage, there is evidence that it has negative effects on youth employment. Yet there is also contrary evidence to suggest otherwise. The reason being is that there are a plethora of other variables at play. For instance, many employees have benefits instead of higher wages, so when the minimum wage goes up, they lose those benefits. At the same time, businesses will find it far easier to pay workers a higher wage during an economic boom when it is selling more goods. However, when the economy is doing badly, a minimum wage may prove to be a drag on employment growth.

The conclusions drawn by economists are never complete due to the inability to test dependent variables. This leads to a number of debates around economic topics that are never fully scientifically resolved. This was succinctly demonstrated by Winston Churchill in his quote:

“If you put two economists in a room, you get two opinions unless one of them is Lord Keynes, in which case you get three opinions.”

What is Economics the Study of

In economics, there are three main factors of production. They are labor, land, and capital. Economics itself is the study of how these three factors come together to create goods and what is the most efficient way to allocate those resources, in order to maximize the output of goods. Equally, what type of system is best to ensure the optimal outcome for society?

Economics also studies human behavior and how, as consumers, we react to changes in price, quality, and quantity. For instance, the value of water and diamond paradox explains why we value diamonds so much more highly than water – a good we need for survival. As water is relatively abundant and available, we value it much less than a scarce resource such as diamonds.

“Economics studies the three main factors of production: capital, land, and labour, and how these can affect economic output.”

Scarce resources are at the heart of economics because with unlimited resources, we need not worry about how we economize resources. We use economics in our everyday decision making. We only have a certain amount of money in our bank account, so we prioritize what we buy with that money. Decisions are made on a daily basis. For instance, instead of getting an expensive premium brand, we may choose a cheap basic one because we know we do not have enough resources (money) to live that lifestyle.

Economics itself studies why individuals, businesses, and governments react to limited resources. For instance, should the government spend more money to boost the economy? How higher taxes affect the wider economy? How do higher prices affect consumer demand?

“Economics looks at how individuals, businesses, and governments react to limited resources.”

These decisions link back to the three factors of production – land, labor, and capital. Employees and consumers have to decide how much of their labor they are willing to exchange for capital (cash). At the same time, how much of that capital they are willing to exchange for other people’s labor.

Land is also an important factor as shops and factories need land, as do people to live in their homes. So economics studies how these factors of production work together and how best to deploy these resources to the most efficient use.

Types of Economics

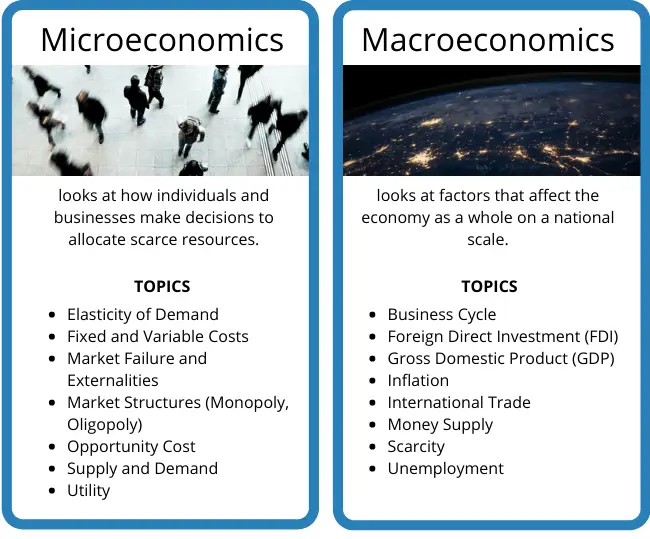

There are two main types of economics – macroeconomics, and microeconomics. First of all, macroeconomics covers topics that are broad in focus and on a national scale. This includes the economy’s performance, structure, behavior, and decision making as a whole.

Second of all, microeconomics covers topics that are more specific to businesses. More specifically, it looks at how individuals and businesses make decisions to allocate scarce resources.

There are a number of key economic concepts that are necessary to understand how the economy works. These can have overarching effects in our everyday life without us even knowing about them. It is important to understand these core concepts to make sense of the news and politics that surround us.

Politicians may say they have achieved record economic growth and that unemployment has never been so low. Central banks may claim they have kept inflation down and stimulated the economy. Whilst environmentalists may demand government intervention to deal with the negative externalities of pollution.

By understanding these core economic concepts, we can start to understand these claims in a more analytical way.

Macroeconomics

Macroeconomics looks at factors that affect the economy as a whole. For instance, inflation is something that affects more than the local town. Equally, the money supply and unemployment are issues that concern the whole country.

1. Business Cycle

The business cycle is the upward and downward trend of economic growth. More specifically, it refers to the transition between economic expansion, towards economic decline and a recession.

2. Foreign Direct Investment (FDI)

FDI is where international businesses invest money in other countries. This could be to start a new business or invest in an existing foreign-owned business.

3. Gross Domestic Product (GDP)

GDP refers to the total number of goods and services the nation has made in a set period.

4. Inflation

Inflation refers to the price increases of goods and services over a period of time. It is most commonly measured using the Consumer Price Index (CPI).

5. International Trade

International trade looks the numerous factors that affect trade between nations. These include tariffs, quotas, regulations, and other protectionist policies.

6. Money Supply

Money is a medium of exchange that represents the value we place on a good or service. Its supply is crucial to the exchanges we make on a daily basis. Too much money supply can lead to inflation and too little can lead to deflation.

7. Scarcity

In economics, scarcity refers to the limited resources we have available. We study how these scarce resources can be used most effectively.

8. Unemployment

Without employment, people are not producing an economic output – which often leads to lower standards of living and quality of life.

Microeconomics

Microeconomics looks at specific factors in economics – largely looking at the behaviour and actions of individuals and firms.

1. Elasticity of Demand

Demand can be either elastic – where consumers are highly responsive to price. So when prices go up, they will go elsewhere. Demand can also be inelastic – where consumers are largely irresponsive to price increases.

2. Fixed and Variable Costs

Fixed costs and variable costs make up to two main costs to businesses. They help explain why some markets are more competitive than others. For instance, markets that have high fixed costs may require new competitors to invest millions before they can enter.

3. Marginal Cost

A marginal cost is an additional cost to a business to produce a further good or service. In other words, how much it takes to produce one more.

4. Market Failure and Externalities

Market failures occur when businesses do not allocate costs effectively to the end consumer. This may lead to negative externalities in the form of pollution, or, positive externalities in the form of education.

5. Market Structures

Market structures include monopoly, perfect competition, oligopoly, monopsony, and monopolistic. Each describes how competitive the market is, with benefits and disadvantages to each.

6. Opportunity Cost

An opportunity cost is where we forego one option at the cost of another.

7. Supply and Demand

Supply, demand, and its reaction to prices is at the heart of economics. When prices go up, supply reacts and increases, whilst demand falls. Similarly, when prices go down, supply reacts and declines, whilst demand increases.

8. Utility

Utility simply refers to an individual’s enjoyment of a good or service. In other words, we receive utility from going to the cinema, bowling, or consuming a meal at a nice restaurant.

Economic Systems

In economics, there are four systems – traditional, capitalist, socialist, and a mixed economy. An economic system is basically what dictates the rules by which individuals are able to trade with each other. It sets the ‘rules of the game’ so to speak.

1. Capitalism

Capitalism refers to the private ownership of resources – so the government has no control. That means everything from the local shopping center to the roads is privately owned.

In this system, markets are primarily driven by supply and demand. So higher prices will encourage firms to increase supply, whilst putting customers off and lowering demand.

Under this economic system, the government has no involvement in the economic activities of individuals, apart from administering law and order. This is to ensure private property rights are protected and adhered to. That way, private entities can trade and do business in the comfort that their property will not be destroyed and contracts will be enforced. This gives confidence to economic parties that they can invest without the fear of loss.

2. Mixed System

A mixed economic system is essentially a mixture of socialism and capitalism. This is where some resources are owned and controlled by the government, and others are owned privately. This is the most prominent system used throughout the world today.

By mixing parts of the socialist and capitalist systems, it is argued that it is the best of both worlds. Not too much government intervention, but enough to prevent capitalism from running free and creating negative externalities.

3. Socialism

Socialism, also known as a command economy, is where power and ownership of property belong to the government under the banner of public ownership. This allows economic decisions to be taken by central powers. That means it controls what to make, how much to make, and where to make it.

Most socialist regimes operate on a long-term basis that is driven by a central economic plan. This may be to boost agriculture or manufacturing – which in turn dictates where it allocates resources. It may shift workers from working in call centers to manufacturing plants in another city.

The purpose of this is to ensure each individual is properly catered for in terms of food, water, shelter, and warmth – the basic human needs.

4. Traditional Economic System

A traditional economic system is very basic. There are no government regulations and trade between each other is generally done through a barter system. It relies on basic customs and traditions to ensure a collective responsibility between each other. This is best demonstrated through the indigenous population of America.

Under a traditional economic system, there are some elements of the division of labor. For instance, men would go off to hunt, whilst women would gather food and look after the children.

FAQs on Economics

In simple words, economics is the study of how we can use resources most efficiently. Resources are scarce and have alternative uses, so economics looks at the best way by which we can use them.

The two main branches of economics are microeconomics (individual actions and incentives) and macroeconomics (factors that impact on the whole of the economy).

We study economics to understand how resources have alternate uses and how they can be best used to maximise our utility (satisfaction) as humans.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Diseconomies of Scale: Definition, Types & Examples - It is an economic term that defines the trend for average costs to increase alongside output.

Diseconomies of Scale: Definition, Types & Examples - It is an economic term that defines the trend for average costs to increase alongside output.  Physical Capital - Physical capital refers to tangible assets, including machinery, equipment, buildings, and infrastructure, used in the production of goods and services.

Physical Capital - Physical capital refers to tangible assets, including machinery, equipment, buildings, and infrastructure, used in the production of goods and services.  Conflict of Interest - Conflict of interest refers to a situation where an individual or entity's personal or financial interests conflict with their professional…

Conflict of Interest - Conflict of interest refers to a situation where an individual or entity's personal or financial interests conflict with their professional…