Table of Contents ![]()

Variable Cost: Definition, Formula & Examples

What is Variable Cost?

A variable cost is a cost that changes depending on how much a business produces. In other words, the more goods a business produces, the higher the variable cost. Equally, the fewer goods a business produces, the lower the cost.

To explain, each additional good a business produces represents a variable cost. For example, McDonald’s will have a variable cost it pays to produce each Big Mac. For each one it produces, there are costs in the form of ingredients, such as the hamburger, bun, lettuce, gherkin, and other ingredients.

If McDonald’s produces 1 Big Mac, it may cost $5 for the ingredients. By contrast, if it makes 1,000 Big Macs, the variable cost will fall significantly as it benefits from economies of scale. In turn, it is able to negotiate a discount with its suppliers for key ingredients such as beef, lettuce, and buns. So as McDonald’s makes more Big Macs, it is able to lower its marginal variable costs. Although its total costs will increase, the cost to make an additional hamburger decreases.

Key Points

- A variable cost is a cost that changes in line with output.

- As output increases, variable costs increase, and when output declines, it declines.

- Examples of variable costs include: utilities, commission-based pay, raw materials, and transport costs.

We define variable cost by its relationship between output and cost. So when output increases, these costs increase, and when output decreases, variables costs decrease.

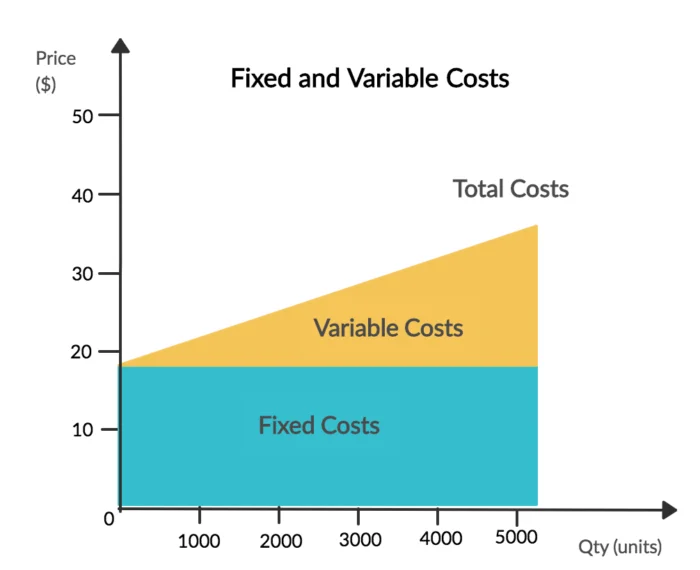

As we can see from the graph below, the variable cost is in stark contrast to fixed costs. Whilst a fixed cost remains constant, variable costs change in line with output. Whilst the graph depicts a straight line, this may vary in real life. For instance, companies may become less efficient at a certain point, thereby making the variable cost increase at a faster rate. Similarly, the firm may benefit from economies of scale, meaning the these costs go up at a slower rate.

Examples of Variable Cost

A variable cost is a type of cost which varies depending on the level of output. Some examples of variable cost include:

1. Direct Raw Materials

Direct raw materials are what the business uses to create the final product. Examples include wood, metals, meat, vegetables, and tobacco, among many others. An important distinction to make is that these materials only cover those that businesses use to create the final product – not other factors of production.

The more demand there is for a final product, the more raw materials the firm needs. In turn, this increases its variables costs that increase alongside demand and final output.

2. Commission-Based Pay

Commission-based pay is where workers get paid based on their output rather than a flat rate. For example, salespeople receive a low fixed salary as well as a commission based on the number of sales they make. Their base salary is considered a fixed cost as this will be paid whether the salesperson makes 10 sales or zero.

By contrast, the variable cost is the commission paid to the salesperson based on the number of sales they make. This is because the cost varies. So when the salesperson makes 2 sales, they get paid for those, whilst if they make 10 sales, they earn even more. So the cost to the business increases alongside the number of sales.

3. Utility Costs

We can consider utilities both a variable AND a fixed cost. For Supermarkets and other retailers, it must have its electricity on for 12 hours or so a day. This is a fixed cost – as it has no impact on output. On the other hand, the cost to run a production line has a direct relationship between cost and output. So for manufacturing and other such firms, utilities count as a variable cost.

The reason for such is that the cost to keep the lights on depends on how many goods the firm produces. For example, a surge in demand may require a manufacturer to stay open an extra couple of hours. In turn, there are additional utility costs associated with this – so the costs can vary month by month depending on demand.

4. Transportation Costs

For each additional unit the firm transports, there is an associated transport cost. Whether by sea, air, or road, the more goods the firm transports, the higher the cost. This allows for a level of economies of scale to be achieved, thereby reducing the marginal costs. However, a businesses transport costs vary depending on output, which classifies it as a ‘variable cost’.

Real World Example of Variable Cost

Let us take a real-world example and assume that it costs a manufacturer $100 to produce one television. This costs $50 in direct materials; $30 in utility costs; and $20 in transport costs.

| 1 Television | 3 Televisions | 10 Televisions | 0 Televisions | |

|---|---|---|---|---|

| Direct Material Costs | $50 | $150 | $500 | $0 |

| Utility Costs | $30 | $90 | $300 | $0 |

| Transport Costs | $20 | $60 | $200 | $0 |

| Total Variable Costs | $100 | $300 | $1,000 | $0 |

As the production of televisions increases, so too do the company’s costs. However, if the company was to make 0 televisions, its costs would decrease to zero. Yet at 10 televisions, its costs increase in line with the number it produces.

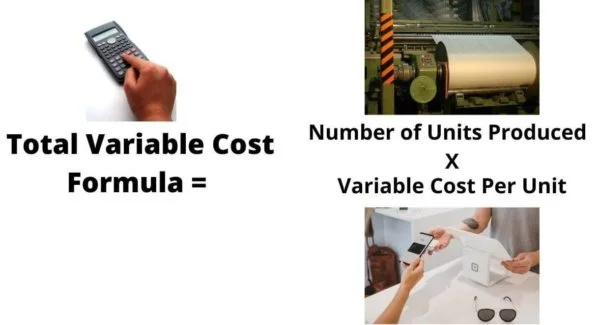

Variable Cost Formula

The total variable cost equals the total number of goods a business produces, multiplied by the cost per unit.

We can calculate the variable cost using the formula: total variable cost = number of units produced x variable cost per unit.

Variable Cost vs Fixed Cost

Variable costs differ from fixed costs in the fact that the cost can vary depending on how many products / services a business produces. Some of the key differences can be seen below:

- A fixed cost remains the same regardless of output. By contrast, a variable cost changes changes based on output.

- A fixed cost is one that is generally paid over a given period; usually a month, or year. By contrast, a variable cost is based on volume of output, rather than time.

- Businesses must always pay their fixed costs regardless of how well they are doing. By contrast, variable costs only occur once there is a good or service being produced.

- Fixed costs cover: new buildings, rent, contracted salaries, and insurance. By contrast, variable costs cover: materials consumed, product supplies, commissions, utilities, and transaction fees.

Related Topics

FAQs

A variable cost is a cost that changes with the level of production or output. As production increases, variable costs also increase, and as production decreases, variable costs decrease.

Examples include:

– Direct Raw Materials

– Commission-based pay

– Utility Costs

– Transport Costs

– Variable Credit Card Fees

The total variable cost equals the total number of goods a business produces, multiplied by the cost per unit.

We can calculate this using the formula below:

These vary based on output and include factors of production such as Raw Materials, Utility Costs, Commission-based pay, Transportation Costs.

Fixed costs are paid regardless of how much a business produces, so do not depend on output. By contrast, variable costs vary depending on how much a business produces.

Some key differences include:

– A fixed cost is one that is generally paid over a given period; usually a month, or year. By contrast, a variable cost is based on volume of output, rather than time.

– Businesses must always pay their fixed costs regardless of how well they are doing. By contrast, variable costs only occur once there is a good or service being produced.

– Fixed costs cover new buildings, rent, contracted salaries, and insurance. By contrast, variable costs cover materials consumed, product supplies, commissions, utilities, and transaction fees.

Technology has had a significant impact on variable costs, particularly in the areas of automation and material innovation. Automation has reduced labor costs, while new materials have reduced material costs. Advancements in technology have also led to improved efficiency, which can reduce variable costs.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Offshoring: Definition, Pros, Cons & Examples - Offshoring is where a business moves its operations abroad.

Offshoring: Definition, Pros, Cons & Examples - Offshoring is where a business moves its operations abroad.  Absolute Poverty: Definition, Examples & Causes - Absolute poverty is where an individual is unable to meet their immediate needs.

Absolute Poverty: Definition, Examples & Causes - Absolute poverty is where an individual is unable to meet their immediate needs.  Sunk Cost: What it is, Examples & Fallacy - A sunk cost is a payment that has been made but cannot now be recovered.

Sunk Cost: What it is, Examples & Fallacy - A sunk cost is a payment that has been made but cannot now be recovered.