EBITDA: Definition, Pros, Cons & Example

What is EBITDA

EBITDA stands for Earnings Before Interest, Tax, Depreciation, and Amortization. It is a useful financial metric which is found an a companies income statement.

Unlike net income, EBITDA includes the values of key metrics such as interest, tax, depreciation, and amortization. Net income is essentially the profit after these are taken away. So what the company makes after it pays for these costs.

As interest, taxes, depreciation, and amortization are included within EBITDA, it helps to compare profitability between industries. For example, the oil and gas industry is extremely capital intensive. This means that it is likely to have high capital costs which fall under depreciation. By including these costs, we are able to level out the profitability to compare against industries that are not so capital intensive.

Key Points

- EBITDA is the short abbreviation for ‘Earnings Before Interest, Tax, Depreciation and Amortization.

- Investors use EBITDA to compare companies profitability against each other.

- Although investors commonly use EBITDA, its calculation can vary from company to company as it is not a GAAP.

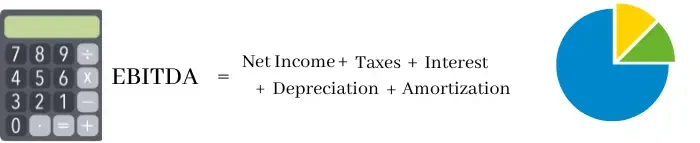

- EBITDA = Net Income + Interest + Tax + Depreciation and amortization.

EBITDA Formula and Calculation

EBITDA is relatively easy to calculate. It can be done using a companies figures found on its income statement and balance sheet. The formula can be seen below:

Net Income

Net income refers to the firms revenue minus its cost of goods, depreciation and amortization, interest, and taxes. It’s one of the firms key financial metrics which helps investors see how profitable the firm is.

Interest

Interest expense refers to the interest payments firms make on their debt. EBITDA includes this element in its calculation – noting it’s BEFORE interest. So it’s before interest is taken away.

Interest is important because companies have very different capital structures. Some may have high levels of debt with lots of interest payments, whilst others may have few. Some may also have higher interest payments, particularly if they are smaller are present greater risk to investors. By calculating EBITDA, it helps eliminate these variations and better understand the firms underlying profitability.

Taxes

There can be a great deal of variability with regards to taxes, particularly when firms are operating globally. This can create a misleading picture to a firms underlying profitability. For example, there are large global firms which pay almost 0 percent tax. However, there are more ethical firms that pay the given rate. That doesn’t necessarily mean the large global firms are more profitable, but rather, choose what is arguably unethical practices.

By including tax, we can therefore level the playing field and remove the variability that results from globalization and different accounting practices.

Depreciation & Amortization in EBITDA

Depreciation and amortization is an accounting term that spreads out the cost of an asset across a period of years. Depreciation covers tangible assets which decrease in value, such as machinery, computers, furniture, and vehicles. A machine that is worth $10,000 might have a lifespan of 10 years. So on a companies account, this would be spread out at a cost of $1,000 per year.

By contrast, amortization covers intangible assets such as patents, licences, and trademarks. These assets have a set lifespan by which they provide the company with a benefit. For instance, a patent generally has a lifespan of around 20 years. Once that patent has finished, it’s no longer an asset. So amortization covers the cost of this asset over the course of its life.

EBITDA Calculation

Usually, a firms EBITDA is reported within the income statement. However, some may not report this figure, so we may need to calculate it. We can do that by taking some key financial information from the income statement. First of all, we will look for net income. For some companies, this might come under the general term ‘Profit (loss) for the year’, or something similar.

To net income, we add any interest that the company has paid within the year. Some companies might call it ‘Finance costs’ or ‘Interest costs’. Once this is done, we then add on the relevant tax. This tends to be known as ‘taxation’. Then finally, we find out the Depreciation and amortization costs. This can also be found within the companies income statement – usually under some similar to ‘Depreciation, depletion, and amortization’.

Once the key figures are found, we add them into the formula:

EBITDA = Net Income + Interest + Tax + Depreciation and amortization.

For example, a company may have the following figures:

- Net income = $150,000

- Interest = $20,000

- Tax = $35,000

- Depreciation and amortization = $75,000

So the firms EBITDA would equal $150,000 + $20,000 + $35,000 + $75,000 = $280,000.

EBITDA Margin

The EBITDA margin refers to the percent of EBITDA to the firms revenue. In other words, it calculates the firms profit margins without subtracting the costs of interest, tax, or depreciation and amortization. We can calculate this using the formula EBITDA / Revenue = Margin.

The EBITDA margin can be a useful financial measure as it reduces the variable effects which might come about due to depreciation, amortization, and tax laws. Some firms might account for these differently, whilst different geographical location might alter taxation costs. So by effectively removing these factors, there is greater consistency not only between reporting years, but also comparisons against competing firms.

In comparison to other financial measurements such as net profit margin, EBITDA smooths out any variations in interest, tax, or deprecation and amortization. For example, a firm might invest heavily in new machinery which impacts the firms net profit. This may seem like the firm is producing lower returns, but merely shows a long-term investment into the business. By removing the depreciation cost, we are able to obtain a more stable financial metric by which we can compare profitability.

Drawbacks of EBITDA Margin

Although the EBITDA margin can be a useful measurement when factoring in significant year on year variations, it does have its drawbacks. For example, the exclusion of interest can hide a companies underlying debt. In turn, it may seem that the financial performance is better than it really is. After all, if a company is paying more on debt repayments than it is earning, it probably isn’t going to be a good investment.

Some firms that focus on the EBITDA margin may do so because it is more favourable to their financial position. So to investors, it may seem like the performance is better than it actually is. At the same time EBITDA isn’t regulated by Generally Accepted Accounting Principles, which means there is more scope for manipulating figures.

Investors should use the EBITDA margin carefully and use in conjunction with other metrics such as the operating or profit margins to help evaluate overall performance.

Pros of EBITDA

Excludes Fluctuations in Capital Expenses

EBITDA excludes depreciation and amortization costs which account for a companies capital expenditures. For industries which rely of high levels of capital investment, these expenses can provide a misleading picture.

Companies might make significant investments in one year. For example, one firm might undertake a significant capital investment project which increases the cost of depreciation and amortization. These investments may effect the firms short-term profitability until the investments start producing returns.

In the short-term, these investments show that the company is making significantly less profit than a competitor that is not undertaking capital investment. This can be misleading as it may suggest that the company making better profits in the short-term is a better investment. However, the firm investing may be setting itself up for the future.

By removing this variation, investors are able to better understand the companies current profitability. Such investments play no impact on the firms current profitability, which therefore provides a better comparison.

Focus on bottom line Profitability

EBITDA is a useful indicator of a firms profitability. Unlike gross profit, it factors in operating costs such as rent, utilities, and maintenance. However, unlike operating profit, it doesn’t include depreciation and amortization.

Gross profit takes the firms revenue and subtracts the cost of goods. However, it doesn’t include other operational expenses such as rent and utilities. These costs are taken away from gross profit to end up with operating profit. Whilst this doesn’t include tax or interest, it does include depreciation and amortization. So in a way, EBITDA is the next level beyond these two measurements.

By stripping back the layers or interest, tax, depreciation and amortization, we end up with a relatively reliable financial metric of profitability. It includes crucial operating expense costs, but removes the potentially misleading costs of depreciation and amortization.

Commonly Used

Although EBITDA is not part of GAAP, it is a widely used measure. The reason is that it can be an effective tool at comparing businesses across industry – particularly where there is significant levels of capital investment.

EBITDA is commonly found on companies financial reports, so it is an important concept to understand. It provides something unique and different to other metrics, so its presence can be useful if used in conjunction with other financial information.

Straight Forward Measurement

EBITDA is a relatively straight forward measurement as it includes commonly found financial information. Net income, interest, tax, and depreciation and amortization are all standard financial items that are found on a balance sheet.

EBITDA is essentially net income without the costs of interest, tax, and depreciation and amortization. So it’s essentially just profit without certain costs involved, which makes it a more straight forward metric to understand than many others.

Cons of EBITDA

Ignores Capital Expenditure

The fact that EBITDA excludes capital expenditure can be seen as an advantage in one way. However, companies can use it as a tool to hide its financial difficulties and shortcomings. By ignoring capital expenditure, a firm is ignoring a major cost.

Regarding EBITDA, Warren Buffet said “Does management think the tooth fairy pays for capital expenditures?” which sums the issue up quite well. A capital expenditure is a cost and if a company doesn’t factor that in, then the result can be misleading.

For example, a company may have five factories that have a lifespan over 10 years. During that period, its EBITDA may remain exactly the same, suggesting it has the same value. However, at the end of the period, its factories have no value and the firm must replace them. Yet this comes at a massive cost which would not be so obvious to investors following EBITDA.

Can be Manipulated

EBITDA is not a Generally Accepted Accounting Principle (GAAP), which means that the specific calculation can vary from one company to the next. This is because there is no official rule which companies should use to calculate it. In fact, many companies will actually use different calculations year on year.

A particular issue to note is where companies use EBITDA in its financial statements where it didn’t previously. There are various reasons why a company may do this, but sometimes this may not honest and transparent. For instance, an emphasis on EBITDA over net income might suggest that there are some significant issues with debt or rising capital costs.

Inconsistency

Although the formula for EBITDA may seem simple enough, there isn’t a general accounting rule, so firms may use different terminology to calculate it. Some may use different accounting techniques to manipulate the figures to achieve a beneficial EBITDA.

At the same time, due to the lack of consistency, it makes it more difficult to compare companies. If one measures EBITDA one way and another firm measures it another, there is no consistency between the two. Therefore any comparisons become meaningless.

Misleading Company Valuation

Investors frequently use EBITDA to calculate a firms Return on Investment (ROI). They do this by dividing the companies Enterprise Value (EV) by EBITDA. This then provides a financial valuation ratio which helps determine a companies valuation.

The issue is that this multiple does not take into account capital expenditures. As capital expenditures are not considered, it can lead to an inflated price. Investors commonly use the Price to Earnings (P/E) ratio to assist with investment decisions. By comparison, this is higher than the EBITDA multiple because capital expenditures are generally a massive cost for most businesses. In turn, this can make businesses look cheaper, and capital intensive industries more attractive.

Ignores working capital requirements

For companies that rely on heavy levels of capital re-investment, EBITDA makes the balance sheets look healthier. It boosts the firms perceived profitability, but completely ignores the firms working capital requirements. Any changes to the amount of cash a firm needs to cover its normal expenses is not considered within EBITDA.

This is a crucial point because if a firm doesn’t have enough cash to cover its short-term costs, it’s going to go under pretty quickly. Interest, tax, and depreciation and amortization are all costs that the business must pay, both in the long term, but crucially in the short-term as well.

EBITDA Example

Doug’s Donut store has sales worth $1.5 million. Of that, production costs such as the flour, eggs, milk, and sugar, among others, costs $200,000. Operating expenses such as utilities, rent, and insurance cost $300,000. Depreciation and amortization of goods such as the friers, hobs, and furniture amount to $150,000.

The store also has a small loan which incurs interest of $50,000 per year. At a tax rate of 20%, the store will also pay $160,000 in taxes, leaving a net income of $640,000. This is calculated by taking the revenue ($1.5 million) and subtracting away the costs (production costs: $200,000, operating costs: $300,000, depreciation and amortization: $150,000, interest: $50,000). This amounts to $800,000 in pre-tax profit. So after a 20% tax, we end up with $640,000 as the net income.

| Net Income | $640,000 |

| Depreciation and Amortization | + $150,000 |

| Interest | + $50,000 |

| Taxes | + $160,000 |

| EBITDA | $1,000,000 |

EBITDA Comparisons

EBITDA vs Revenue

Revenue measures how much money a company makes in sales. If a retailer sells a chocolate bar for $2, then $2 is the firms revenue. By contrast, EBITDA measures profitability. It includes revenue, but subtracts the cost of doing business both in terms of the cost of products, as well as operational costs such as rent.

EBITDA vs Gross Profit

Gross profit is the firms income once the cost of production is taken away from the firms revenue. This includes items such as raw materials and labor. However, it doesn’t include operating expenses such as utilities, insurance, and advertising.

By contrast, EBITDA includes the cost of production, as with gross profit, but also operating expenses minus interest, tax, and depreciation and amortization.

EBITDA vs Operating Profit

Operating profit and EBITDA are very similar in many regards. They both exclude costs for tax and interest. They both look at costs after the cost of goods and operating costs. However, EBITDA excludes costs for depreciation and amortization whilst operating profits includes this in its calculation under ‘operating costs’.

FAQs

EBITDA stands for Earnings Before Interest, Tax, Depreciation and Amortization.

You can calculate EBITDA by taking a firms net profit and adding back in the costs of interest, tax, and depreciation and amortization.

Amortization refers to the decreasing value of intangible assets such as trademarks, licenses and patents. For example, assets such as patents generally have a lifespan of 20 years. Amortization is the devaluation of this asset over time. This is in contrast to depreciation which relates to TANGIBLE assets instead of intangible assets which amortization covers.

EBITDA is a type of profit which measures different costs. Whilst it includes a number of operating expenses and the cost of production, it does not include important costs such as interest, tax, and depreciation and amortization. These are still costs that need to be paid for, so it is not a good proxy for profit.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Factors of Production: Definition, 4 Factors & Examples - The factors of production are all the various elements that are required to come together to create a good.

Factors of Production: Definition, 4 Factors & Examples - The factors of production are all the various elements that are required to come together to create a good.  Laissez-faire Economics: What it is & Example - Laissez faire economics is characterised by the absence of government involvement in the economic interactions between parties.

Laissez-faire Economics: What it is & Example - Laissez faire economics is characterised by the absence of government involvement in the economic interactions between parties.  Dependent and Independent Variables in Economics - An independent variable is one which is changed by the researcher in order to find out what impact it has…

Dependent and Independent Variables in Economics - An independent variable is one which is changed by the researcher in order to find out what impact it has…