Retained Earnings Definition

What are Retained Earnings

Retained earnings account for the net income of a business minus any dividend payments. For example, if a business makes $1 million in net income any pays its stockholders $300,000 in dividends, it is left with $700,000 in retained earnings.

The term ‘retained’ refers to the fact that these are profits that the company keeps. This includes ‘net income’, which is essentially income after tax. So the retained earnings of a company is everything it gets to keep, but only after it has paid the relevant dividends to its stockholders.

It’s important to note that retained earnings rollover from year to year. You can look at it as somewhat as ‘money in the bank’. The money doesn’t disappear from year to year, but instead is ‘retained’. So year on year, this will carry over and get added to the companies net income for that year. Once the company subtracts any dividend payments, we then have the retained earnings for the subsequent year.

Key Points

- Retained earnings are a compilation of previous years net profits and losses, minus and dividend payments.

- Retained earnings (RE) can be calculated using the formula: RE = Last year’s RE + Net Income – Dividends.

- Although retained earnings are a useful barometer for a companies performance, they don’t provide the full picture and should be used alongside other fundamental measures.

Retained Earnings Explained

Retained earnings (RE) represent shareholder value and is part of the equation that makes up total shareholder equity. The higher the RE, the higher the shareholders value and with higher shareholder value, stock prices can increase and create positive equity for investors.

As RE are part of shareholder equity, it is not considered as an asset. Instead, it can be found under the equity section of the balance sheet. However, executives of the company can use these earnings to re-invest in the company, purchasing machines, land, and other assets. Alternatively, executives may use it to reduce the firms liabilities. Both of which should help increase shareholder value.

RE do not represent the cash in hand value that the company has. Instead, it represents how efficient the company has been with its profits. For example, if it invests wisely, it will increase the value of its assets, or reduce the liabilities on its balance sheet. This closes the loop between the income statement by which RE are derived, and the balance sheet, whereby it reflects shareholder equity.

This helps to provide a clear and concise picture of a businesses financial position. It provides a long-term view of the companies profitability through the years. For each consecutive year, it helps to paint a picture of the companies performance on metrics such as how much it saves, earns, and invests.

Summary

- Retained earnings (RE) are not an asset. Instead, they are seen as an equity.

- RE is part of shareholder equity.

- Although RE is not an asset, it can be used to buy assets.

- RE helps investors get an idea on how efficient the company has been with its profits.

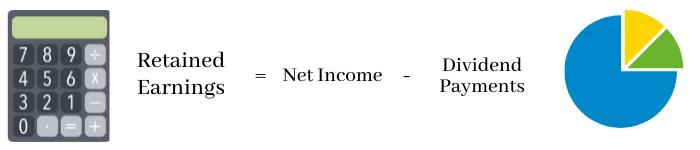

Retained Earnings Formula

In it’s most simplest of forms, retained earnings (RE) can be calculated using the formula:

This calculates everything the company has earned across the year, minus its expenses. It’s important to note that net income also factors in taxes. So it relates to profits the company makes after expenses as well as taxes.

The companies net income is essentially its ‘take-home pay’. However, it still has an obligation to its stockholders to pay a dividend. If the company is in good financial health, then it may award a generous payment. This comes out of the companies net income, which then leaves the companies final ‘retained earnings’.

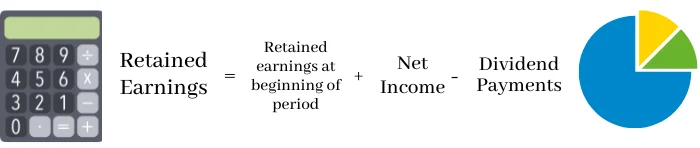

If we are looking at the longer term, for instance, longer than a year, we would use the formula below:

This carries forward the previous years retained earnings and follows a similar process. The net income is added to the RE from the previous year, with the dividends subtracted from that. This then leaves us with the RE for the current year.

You may now ask, what about when the company spends some of those RE? Will that not reduce the amount carried over? Well the value of RE is calculated at the end of the companies financial year. For example, this may be 31 March. The RE are calculated up till that date. This is then carried over onto the statement for next year starting 1 April.

If the company spends its RE, this would count as an expense and therefore affect the ‘net income’. For instance, funds that are used to produce goods would fall under ‘cost of goods sold’. For capital expenditures such as machinery, these would be booked as depreciation over a set period of years. So although the RE remain, the expenditures are compensated by a decline in the net income.

Retained Earnings Example

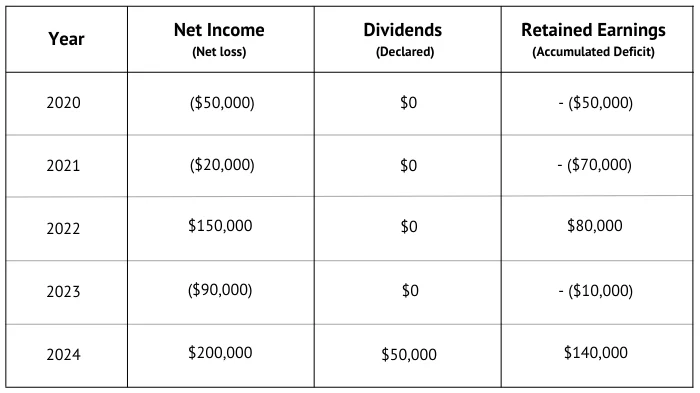

To explain retained earnings (RE), let’s look at an example of Doug’s Donut store. In the first year of business, the store has a net income of -$50,000. As this is a negative figure, we can also refer to this as a ‘net loss’. This then translates to a RE of -$50,000 as no dividends were paid out. Again, as the figure is negative, we can refer this as an accumulative deficit.

In the second year, the company makes a net loss of $20,000. When we add the previous years accumulative deficit (RE), we end up with a further decline to $70,000. So over two years, the firm has a negative value for RE of -$70,000.

After some difficulties in the first two years, Doug’s Donut’s manages to make a sizeable net income of $150,000. We then take the previous years RE and add it to the net income for the year. This then brings the RE to a positive figure of $80,000.

Faced with economic difficulties, Doug’s Donut’s end the fourth year with a negative net income of $90,000. This brings the RE back down to a negative figure of $10,000.

A successful fifth year ends with a net income of $200,000. This success is finally shared out among shareholders who receive a dividend of $50,000. So what effect does this have on RE? Well we take the fourth years RE, which was -$10,000. We then add the net income for the current year, which was $200,000. This leaves us with $190,000. Then, we take away the dividend payment of $50,000, which leaves us the final RE of $140,000.

Retained Earnings on Balance Sheet

So where do retained earnings (RE) show on a balance sheet? It isn’t an asset, but is considered under the liabilities section on the balance sheet. This usually comes under ‘Liabilities and Shareholder Equity’, or something similar.

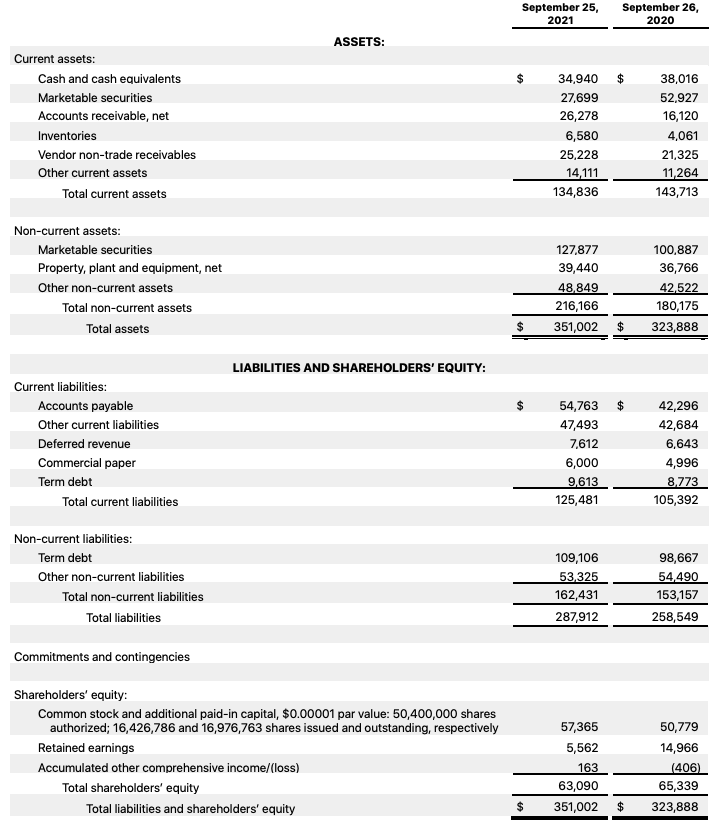

RE will come beneath total liabilities and are located specifically within the ‘shareholder equity’ sub-section. For example, we have Apple’s 2021 Financial Statement below which includes all the various elements of the balance sheet. This includes the main assets, liabilities, and shareholder equity.

From 2020 to 2021, we can see a huge drop in retained earnings from $14.97 billion to $5.56 billion. This may suggest a number of things. First of all, it may suggest that the company made a loss in that year. If it made a loss, then this would affect the net income and hence the subsequent retained earnings.

Second of all, it may suggest that the company re-invested some of those funds into the company. It may have brought some land or marketable securities – thereby increasing its asset value.

Third of all, it may have used those funds to reduce its liability. By paying off debt, it can reduce its liabilities. This can prove beneficial if interest rates are high.

Retained Earnings vs. Profit

In its purest of forms, profit is the money a company makes after its expenses. For example, if a motor vehicle costs $10,000 to make, but is sold for $15,000, then there is $5,000 of profit. In the real world, there are many other costs to consider, but that’s profit in its simplest of forms.

There is then retained earnings (RE). These are essentially the last stage of ‘profits’. The term profit is the first stage by which a firm makes money. Once a firm makes a profit, it must pay taxes. The resulting sum is then referred to as the firms ‘net income’. In other words, profit after tax.

This is where RE now comes in. It is net income minus any payments made as dividends to its stockholders. So this can be seen as the third level, or final stage of ‘profit’ that the firm makes. It has payments that need to be made firstly to the government through tax, and then to its stockholders through dividends.

Only once all recipients are paid, are we left with the final stream of income by which the company can use. However, it’s also important to note that unlike profit, RE is an open account. It roles over from year to year, whilst profit is just a snapshot of one year.

Key Differences

- Profit is income after expenses, whilst RE is profit after taxes and dividends are paid.

- Profit is a one off yearly snapshot, whilst RE offer an ongoing outlook of the company.

- Profit is located on the companies income sheet, whilst RE are on the balance sheet under shareholder equity.

Limitations of Retained Earnings

On its own, retained earnings (RE) provide but a snapshot of a company. It is a useful financial indicator, but does not present an investor with the full picture. Instead, it is far more useful to understand what has happened with those RE. For example, a sudden drop may sound alarm bells to investors. This could suggest a number of things. Perhaps the company is doing badly and losing money, or perhaps it is re-investing into the company.

If the company is re-investing RE, this raises a further question. Is it doing so efficiently, or is it poorly managing the funds? These are questions which cannot be explained by RE alone. It is therefore more useful to understand the wider context, which is what other financial indicators can provide.

There is also the context of the businesses lifecycle. Businesses in their first year are likely to have a negative figure due to initial start up costs and finding traction in the market. By contrast, more mature businesses that do not rely on heavy re-investment typically pay higher dividends which lowers the companies RE.

Tech companies and those which require high capital investments also see heavy re-investment into the company. This often means that these types of industries have lower levels of RE than others. The need for capital to maintain machinery, or develop new technology is necessary to compete.

FAQs

Retained earnings is not an asset. Instead, it is considered as part of shareholder equity. This is because it essentially belongs to stockholders. For example, if the company goes bankrupt, stockholders would receive these funds that are set aside.

Although it is part of shareholder’s equity, it is still up to the company on how to use these whilst the firm is still in operation. So although retained earnings is not an asset, management can decide to use these funds to purchase assets such as machinery etc.

For each accounting period, the previous years retained earnings are carried over. The firms net income is then added to the previous years retained earnings. But what happens if the company spent all those earnings? Well if it has, this would count as an expense on the firms balance sheet, thereby affecting the firms net income and thus the total retained earnings for that year.

A company can purchase new assets such as land, reduce its liabilities by paying off debt, or keep it for future years.

Retained earnings can be found under the shareholder’s equity section within the companies balance sheet.

To calculate it, we can use the formula RE = Last Year’s Retained Earnings + Net Income – Dividend payments.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Crowding Out Effect - The crowding out effect refers to the reduction in private sector investment caused by increased government borrowing and spending, leading…

Crowding Out Effect - The crowding out effect refers to the reduction in private sector investment caused by increased government borrowing and spending, leading…  Why is Communism Bad - Critics of communism argue that it often leads to authoritarianism, inefficiency, lack of incentives, and human rights abuses, making it…

Why is Communism Bad - Critics of communism argue that it often leads to authoritarianism, inefficiency, lack of incentives, and human rights abuses, making it…  Recession: Definition, Causes, Effects & Solutions - In economics, a recession is defined as a decline in economic growth.

Recession: Definition, Causes, Effects & Solutions - In economics, a recession is defined as a decline in economic growth.