Barriers to Entry: Definition, Examples & Types

Barriers to Entry Definition

Barriers to entry form an obstacle to businesses when entering a market. This can come in the form of high start-up costs, strongly branded competitors, or high import duties. For instance, car manufacturers require high start-up costs and face competitors that have high brand trust and loyalty.

Just imagine trying to start a new company to enter the market – it would be extremely difficult. Therefore, as a result of barriers to entry, new firms do not enter the market – thereby reducing the level of competition.

Key Points

- A barrier to entry is something that prevents or deters new businesses entering the market – this may come in the form of high start-up costs, regulatory requirements, or, brand loyalty among others.

- There are 4 main types of barriers to entry – legal (patents/licenses), technical (high start-up costs/monopoly/technical knowledge), strategic (predatory pricing/first mover), and brand loyalty.

- Barriers to entry are important as they can prevent free competition which reduces price and increases choice for the consumer.

So barriers to entry form a roadblock to potential new entrants. This is important because it allows existing firms to make higher profits than in a perfectly competitive market. Fewer competitors mean less downwards pressure on prices. As a result, barriers to entry can contribute to the creation of an oligopoly or a monopoly.

In economics, barriers to entry are crucial to understanding why some markets are inefficient – with consumers paying high prices. For example, utility firms often receive criticism for raising their prices in excess of inflation. However, because the industry has such high barriers to entry, it prevents competitors from entering the market – high start-up costs are one such example.

The Importance of Barriers to Entry

A barrier to entry prevents and restricts competition, so it is in the interest of existing firms to create or perpetuate new and existing barriers. Businesses often do this through lobbying governments to add new regulations, grant patents, or provided favourable treatment.

It is important to understand that some barriers to entry exist naturally and therefore little can be done about them. Brand loyalty, for instance, presents a barrier to entry. If we take Amazon for example – there are few online distributors that would be able to compete. This is because customers have become accustomed to trusting the brand. Trust that would not be so forthcoming to competitors.

We can look at barriers to entry in two ways. First of all, we have ‘un-natural barriers to entry’ – so those that are man-made via government. Then second, we have ‘natural barriers to entry’. For example, brand loyalty, geographical barriers, and economies of scale.

Un-natural barriers such as patents, regulations, and trade, are all government made. Yet they prevent competition. Each has a reason for existing, but it is whether these are worth restricting competition and increasing prices.

Barriers to Entry Examples – 4 Types

Barriers to entry can be categorised under 4 separate types: legal, technical, strategic, and brand loyalty.

1. Legal Barriers to Entry

Patents

A patent is a government-backed barrier to entry. It issues the exclusive right to produce a good for a given period of time, so competitors are legally prevented from entering the market. Some notable examples include pharmaceutical products and many in the field of technology.

Licenses/permits

Licenses and permits are another government granted barrier to entry. These are usually issued by the government to maintain quality, but reduce the level of competition at the same time. As a result, new businesses or individuals will find it hard to enter.

For example, in the US state of Arizona, a license is required for a hairdresser to be able to blow dry hair. It takes over 1,000 hours in order to obtain such a qualification. This dis-incentives would be hairdressers as it makes it unnecessarily difficult for them to enter the market, thereby reducing the level of competition.

Trade Barriers

When governments introduce quotas, tariffs, and other trade restrictions – they also restrict competition. If imported goods become too expensive due to tariffs, then customers won’t buy them – it becomes uncompetitive when compared to domestic suppliers. Consumers are more likely to buy from a domestic supplier that is half the price than a foreign import.

As a result, fewer goods come in from abroad, leaving domestic firms with little competition. Often, this is a consequence of domestic suppliers’ petition to the government to ‘protect’ jobs and the domestic market. Fewer goods coming in means less choice for consumers and higher prices as a result.

Standards and regulation

These can add extra costs to new entrants. First of all, it takes time, money, and effort to get the business up to speed with regulations. Restaurants, in particular, have a number of health and safety and other forms of regulation that owners need to be aware of.

This may require hiring a lawyer, or taking the time to research it all. Whether the final benefit is worth such costs is another matter. However, the cost imposed does provide a barrier to entry for a number of potential entrants.

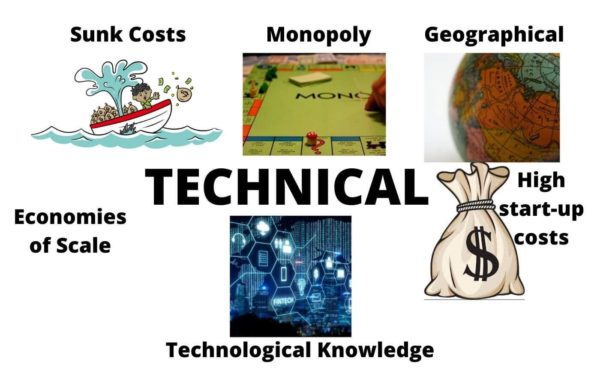

2. Technical Barriers to Entry

High Start-up Costs

Some industries such as oil and gas, banking, and airlines all have extremely high start-up costs. New entrants need millions just to even enter the market. An airplane alone would cost in excess of $10 million, that’s before any costs associated with the hiring of airports, staff, and other associated costs.

Sunk Costs

A sunk cost is a cost that is unrecoverable, so presents new entrants with a big risk. Examples include advertising, marketing, and research and development. So when a new entrant spends millions in new advertising expenditure, it won’t get it back. Consequently, firms consider this when trying to enter the market. In fact, it can deter initial investment as those costs may not be recuperated.

Economies of Scale

When businesses get larger they benefit from reduced input prices. For example, supermarkets can negotiate lower prices for bread and milk, whilst small stores will struggle to negotiate with suppliers.

This makes it difficult for new entrants because they already come into the market at a disadvantage. Big stores can charge lower prices due to their size, which means new entrants are unable to effectively compete.

Monopoly / Oligopoly

In some cases, certain markets contain firms that control a significant part of the market. Microsoft, for example, dominates the operating system market. Only equally big firms such as Apple and Google have managed to even try and compete.

When markets have such strong existing firms, it is almost impossible for new start-ups to compete. This combines with other factors such as brand image, economies of scale, and power of suppliers; all factors that new entrants cannot benefit from. As a result, the upward climb is too significant for new entrants to even consider.

Geographical

In some markets, certain countries obtain a geographical advantage. Canada, for example, is known for its forestry, whilst Australia is a massive producer of iron ore. These generally occur in commodity markets whereby the production of resources is more favourable or abundant. This adds a barrier to entry as new competitors will need to be located in such a favourable location.

Technological Knowledge

When starting a new business, most owners need a certain level of expertise. For example, a restaurant owner may have worked in other restaurants, thereby earning them experience in the day to day management. However, in industries such as airlines or software, there is a significant knowledge barrier.

In order to start a new software business, the owner either needs significant funds to hire a designer. Or, they need the technological knowledge required.

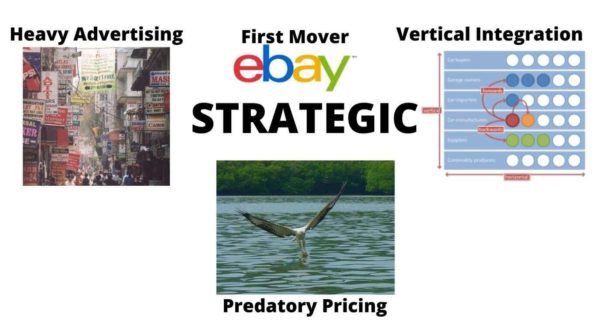

3. Strategic Barriers to Entry

Predatory Pricing

Another example of a barrier to entry is predatory pricing. Firms may artificially lower prices and take a loss in order to push new entrants out of the market. For example, an established local barber may reduce prices further as they know they are can compete on reputation. A new entrant may struggle to cover its costs as a result and be driven out of business.

Heavy Advertising

Upon the entrance of a new firm; existing firms may seek to entrench their position by re-affirming their image as a market leader. By spending heavily on advertising, it enforces trust in the brand. This can be a difficult hurdle for new entrants as existing firms usually have a bigger advertising budget as well.

First Mover

The first-mover advantage is another example of a barrier to entry. For example, eBay and Amazon are both two notable cases. eBay entered the online auctioning business in 1995; the first of its kind. What this did was cement the presence of the firm among customers and the wider population. So when the customer wanted to sell something, they automatically associate it with eBay.

The first-mover benefits from a greater brand image. If you want to sell something, you can easily go to eBay and for many, it’s the first point of call. To change that decision-making process in people’s minds is an incredibly difficult barrier to entry to overcome.

Vertical integration

When firms purchase or merge with another in the supply chain, they can benefit from cheaper supplies. What this does is give the parent firm the ability to undercut new entrants and achieve greater efficiencies.

4. Brand Loyalty – Barrier to Entry

Brand image plays an important part in economic decision making. It reflects trust and assurance of quality. In essence, it solves the problem of a lack of asymmetrical information. Bad brands get destroyed because, well, they are bad. By contrast, the brands that last; the likes of Coca-Cola, McDonald’s, and Walmart have offered quality products at reasonable prices. This sends a signal to the market and consumers that these brands are the best in the business.

Brands such as Coca-Cola, McDonald’s, and Walmart have taken years and millions, if not, trillions of dollars to build up. For a new business to compete against any established and trusted brand would take some work. It has to establish trust; perhaps spending millions on advertisements.

For a new entrant, it’s a bit like starting an extra 100 meters behind in a 100-meter race. It’s not necessarily impossible, but not many entrepreneurs will see it as worthwhile to start with such a handicap against existing brands.

Brands have such power that they create habits. Some customers would not even consider changing their usual purchase of Coca-Cola every week. Even though in blind taste tests, it may be indistinguishable from own-branded Cola, yet customers do it out of habit and trust.

Something that is completely ingrained into their way of thinking and their actions. To change such habits would take great investment, time, and energy; something new entrants just don’t feel is worth the risk.

Barriers to Entry FAQs

Barriers to entry are obstacles that make it difficult or costly for new companies to enter a market and compete with existing firms.

Some examples of barriers to entry include: high entry costs, economies of scale of existing firms, trade barriers, brand loyalty, and first-mover advantage.

There are 4 main barriers to entry:

1. Legal

2. Strategic

3. Technical

4. Brand Loyalty

Barriers to entry can limit competition by preventing new firms from entering a market and competing with existing firms. This can lead to market power and higher prices for consumers.

Barriers to entry can have a negative effect on consumers by limiting competition and leading to higher prices, reduced product variety, and lower quality products.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Related Topics

Further Reading

Perpetuity: Definition, Formula, Types & Examples - In finance, perpetuity refers to the ongoing payment of a bond or security with no end date. Payments are made…

Perpetuity: Definition, Formula, Types & Examples - In finance, perpetuity refers to the ongoing payment of a bond or security with no end date. Payments are made…  Human Development Index - The Human Development Index (HDI) is a composite measure that assesses a country's overall development based on indicators such as…

Human Development Index - The Human Development Index (HDI) is a composite measure that assesses a country's overall development based on indicators such as…  Factors of Production: Definition, 4 Factors & Examples - The factors of production are all the various elements that are required to come together to create a good.

Factors of Production: Definition, 4 Factors & Examples - The factors of production are all the various elements that are required to come together to create a good.