Fixed Cost: Definition, Examples & Effects

What is a Fixed Cost?

A fixed cost is a cost that a business must pay whether it produces one good or a million. Regardless of output, it must pay the same amount. In other words, it is a cost that does not change even at higher levels of output. For instance, rent is an example of a fixed cost. A business must pay this regardless of how many goods it makes and sells.

By contrast, this is the exact opposite of a variable cost, which varies depending on output. Both variable and fixed costs are the two main types of costs to business and make up what is known as total costs.

Key Points

- A fixed cost is set over a period of time and does not vary depending on output.

- Fixed costs differ from variable costs in the fact that it is paid at set periods of each year, whilst variable costs relate to volume and vary depending on quantity.

- Industries with high fixed costs tend to have reduces competition due to barriers to entry.

We can consider the investment in a new factory as an example of a fixed cost. For example, it may cost $10 million to construct the factory ready to manufacture new motor vehicles. Once built, there are no further costs other than maintenance. So this initial investment of $10 million is a one-off cost.

What we see when fixed costs are high, is a barrier to entry. New entrants may find it hard to raise the necessary capital, or, may be put off trying in the first place. Trying to find $10,000 for a new startup is much easier than $10 million. It is for that reason that industries with high fixed costs tend to consolidate and create oligopolies.

Fixed Cost in Economics

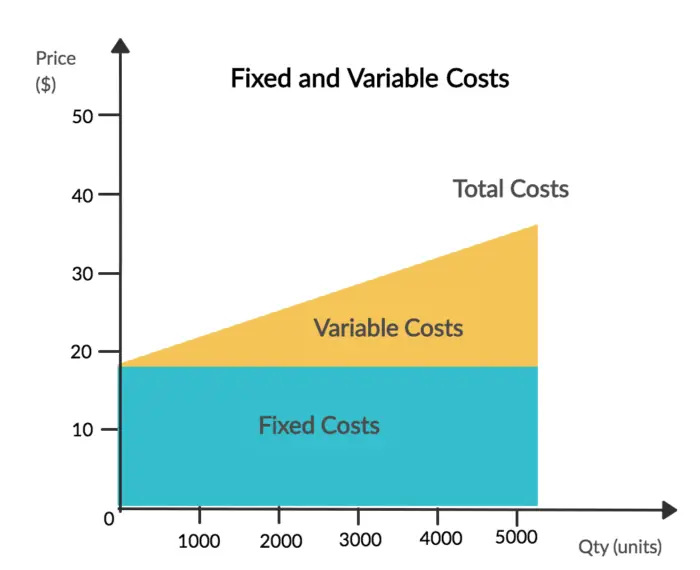

As we can see from the graph below, fixed costs remain constant regardless of output. At the same time, variable costs continue to increase as businesses produce more goods.

As firms produce more, variable costs continue to increase – whilst fixed costs remain constant. However, a fixed cost will increase when the business reaches a certain level of output. For instance, a factory may reach maximum capacity when it produces 1,000 motor vehicles. So in order for it to increase production and output, it must purchase and construct a factory, creating a new fixed cost.

Fixed Cost Graph

Let us take an example of a fixed cost below:

Business A produces 100 Cars a month in its single factory. Over time, demand for its cars increases to 110. Consequently, if it wants to meet demand, it must finance a new factory. The cost to build it is a fixed cost – although the cost of running it is a variable cost.

This new factory is a fixed cost because it is only payable once and does not vary depending on output. However, fixed costs can also include payments that are due on a monthly or yearly basis.

What differentiates it from a variable cost is that it does not directly increase in line with output. For example, rent is due every month and is a fixed cost the business must pay. There are also insurance payments that are payable each year but must be paid whether one good is produced or many.

Fixed Cost Examples

A fixed cost is a cost that is independent of how many products or services a business provides. So whether a company produces one hamburger or 100, the cost is the same.

Some examples of fixed costs include:

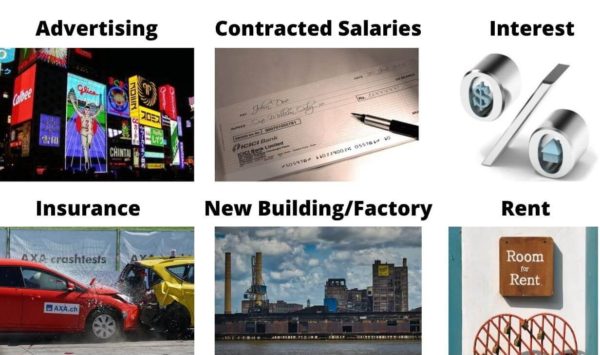

1. New Building/Factory

When a business invests $10 million in a new factory, it counts as a fixed cost. It is a one-off cost that does not vary based on output. In accounting terms, it is the depreciation that is considered a fixed cost. For instance, if the factory was to last 10 years, there would be an annual depreciation of $1 million per year. So rather than having a one-off fixed cost of $10 million, the costs are amortized so the cost is split out through the 10 years.

Effectively, the factory has a value as an asset during the 10 years – until it is no longer productive. As it could potentially be sold on and produce output for x number of years, it still has a value. So although it may cost $10 million to buy, it is still seen as an asset in accounting terms. In other words, $10 million isn’t spent but rather invested in an asset – shares are a similar example. It is only once the value of the asset starts to decrease by which we can consider as a fixed cost. Think of the depreciation of a car for example.

2. Rent

Rent is an annual or monthly charge which is a fixed cost. A business has to pay this regardless of how many customers it serves. For example, a barber will have to pay rent whether they cut one persons hair or twenty people. This may increase in line with inflation, but is fixed for a set period of time.

3. Contracted Salaries

Contracted salaries relate to the annual salary of a business’s employees. Once contracted, this counts as a monthly and annual fixed cost. The employee may be busy and produce 10 times the normal output, or, they may be extremely unproductive and produce half. No matter how productive the employee is, the cost remains fixed. By contrast over-time hours, or incentive based pay counts as a variable cost, as this varies month on month and increases with output.

4. Insurance

Businesses must pay for property and other forms of insurance each year. This is a fixed cost because it doesn’t matter how many products or services they provide, they still have to pay insurance. It could be argued that this is variable, as insurance costs can increase as the firm gets bigger. For example, the cost to insure a large multi-national is much higher than the local mom and pop store.

However, it is a fixed cost because insurance is charged based on risk rather than output. Insurance costs increase in line with risk rather than in line with output. Furthermore, insurance prices do not react to incremental increases in production as a variable cost does. In other words, production may increase by 10, but it has no impact on insurance prices as a fixed cost.

5. Interest

When taking out a loan, there are a number of fixed-rate options available. If a business takes up such an option, this can count as a fixed cost. A charge on the loan is due every month or year, independent of how much goods the business produces and sells.

6. Advertising

By itself, advertising does nothing to increase output. It is not like an additional employee, or the cost to keep the lights and machines on for an extra hour. It is a fixed cost. This is because businesses set an advertising budget, which tends to only vary quarter on quarter. On top of that, advertising costs are still payable whether the business serves one customer or one million!

Effects of Fixed Costs

In industries that have high fixed costs, competition tends to consolidate. That is to say there are fewer competitors than under a perfectly competitive market. This is because it is inefficient for ten separate firms to incur the same fixed cost ten times over.

“Markets that have high fixed costs tend to see consolidation.”

It may cost each business $1 million in fixed costs to enter the market. Across ten businesses, this would equal $10 million. Let us say these fixed costs are for the construction of a factory – which is capable of producing 100 units per year. However, the demand for such products is only 500. Each competitor could produce 50 units each and thereby meet demand. This works, but at a higher cost per unit.

At $1 million in fixed costs, this works out at $100,000 per unit, per business, per year. We calculate this by dividing the fixed cost by the quantity produced – $1 million / 100 units.

By contrast, if each business is producing only 50. This means that there is a cost of $200,000 per unit, per business, per year.

“It is cheaper and more efficient for fewer businesses to supply the market.”

So for industries with high fixed costs, it is cheaper and more efficient for fewer competitors to supply the goods and services. Take airlines for example. The cost of one individual aircraft can come in as much as $300 million. That is a huge expense, particularly if the airliners only fill up half the plane. In turn, these high fixed costs can dissuade potential competitors from entering the market.

Simply put, industries with high fixed costs have a much higher break-even point than those with purely variable costs. Just taking the airline example again – with over $300 million in fixed costs, it will take thousands, if not millions of customers to break-even. After this point, the cost of every sale is only dependent on very low variable costs, meaning higher profits.

Putting this all together – industries with high fixed costs will face lower competition than other types of industries. This is because there is often a high break-even point – meaning they need to make significant sales just to stay in business. This reduces the level of competition. However, at the same time, it means when that break-even point is met; profit-margins can be very large.

Fixed Cost vs Variable Cost

Fixed costs are paid regardless of how much a business produces, so do not depend on output. By contrast, variable costs vary depending on how much a business produces. Some key differences include:

- A fixed cost is one that is generally paid over a given period; usually a month, or year. However, a variable cost is based on the volume of output, rather than time.

- Businesses must always pay their fixed costs regardless of how well they are doing. By contrast, variable costs only occur once there is a good or service being produced.

- Fixed costs cover new buildings, rent, contracted salaries, and insurance. On the other hand, variable costs cover materials consumed, product supplies, commissions, utilities, and transaction fees.

FAQs

A fixed cost is a cost that a business must pay whether it produces one product or a million. Regardless of output, the business must pay the same. In other words, it is a cost that does not change with higher levels of output.

Fixed costs are paid regardless of how much a business produces, so do not depend on output. By contrast, variable costs vary depending on how much a business produces.

Some key differences include:

– A fixed cost is one that is generally paid over a given period; usually a month, or year. By contrast, a variable cost is based on volume of output, rather than time.

– Businesses must always pay their fixed costs regardless of how well they are doing. However, variable costs only occur once there is a good or service being produced.

– Fixed costs cover new buildings, rent, contracted salaries, and insurance. On the other hand, variable costs cover materials consumed, product supplies, commissions, utilities, and transaction fees.

Some fixed cost examples include:

Advertising

Contracted Salaries

Interest

Insurance

New Building/Factory

Rent

Fixed costs can really affect profitability as they have to paid regardless how well the business does. So during periods of low sales, it can really hit into the firms profitability.

Total costs include both fixed and variables costs. A fixed cost is only but a component of total cost.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Related Topics

Further Reading

Economic Growth - Economic growth is the long-term increase in an economy's capacity to produce goods and services.

Economic Growth - Economic growth is the long-term increase in an economy's capacity to produce goods and services.  Fiat Money: How it works, Examples, Pros & Cons - Fiat money is a type of currency whereby the value is guaranteed by government decree.

Fiat Money: How it works, Examples, Pros & Cons - Fiat money is a type of currency whereby the value is guaranteed by government decree.  Are Cryptocurrencies Worth the Risk? An Objective Analysis - Table of Contents What is Cryptocurrency What is Cryptocurrency Mining Types of Cryptocurrency How to Buy Cryptocurrency Advantages and Disadvantages…

Are Cryptocurrencies Worth the Risk? An Objective Analysis - Table of Contents What is Cryptocurrency What is Cryptocurrency Mining Types of Cryptocurrency How to Buy Cryptocurrency Advantages and Disadvantages…