Table of Contents ![]()

Economic System: Definition, Types & Examples

What is an Economic System

An economic system is a network that connects individuals in society and forms economic relationships between them. It determines how a nation’s people collaborate to conduct economic transactions and create a complex whole.

Economic systems are intricate because they rely on millions of people participating in the market, affecting supply and demand. For instance, if millions of people flock to the Apple store for the latest iPhone, it triggers a chain reaction. Apple must order more batteries, glass, electronic chips, and other components, which, in turn, stimulates demand in those industries.

Key Points

- An economic system refers to the framework by which individuals conduct business and trade with each other.

- There are four types of economic systems – traditional, socialist/command, capitalist/market, and a mixed economy.

- Most countries in the world operate under a mixed economy – relying both on aspects of a capitalist and socialist system.

An initial increase in demand can have a ripple effect throughout the economy, sending a signal to the entire supply chain that more products are needed. Economic systems can alter the way these supply and demand signals are transmitted in society.

For example, some systems may impose tariffs or quotas on imports, which can affect the signal between buyers, sellers, and suppliers. Tariffs can make it more expensive to bring goods to market, reducing demand and altering the natural state of the supply and demand signal.

In short, an economic system establishes the rules governing the supply and demand relationship between buyers and sellers.

Types of Economic Systems

Each country has its own unique economic system, with variations between Germany, France, and the US, for example. France has more stringent labor laws, such as the 35-hour workweek, but both the US and France have mixed economies with varying degrees of government involvement and free markets.

Although there are close to 200 different economic systems, they can be categorized into four broad types – traditional, socialist, capitalist, and mixed economies. While these categories do not capture the full diversity of economic systems, they provide a framework for understanding the major differences between them.

Let’s look at these types of systems below:

1. Traditional Economic System

Among the four types of economic systems, the traditional system is the most primitive one. It involves no government intervention, so individuals are left to conduct economic activities on their own. However, this system is limited as it relies on basic customs and traditions.

This economic system lacks modern advancements such as technology, property rights, and capital investment. The way of life is simpler, and economic relationships are more straightforward. Bartering is the most common form of trade, and the use of currency as a medium of exchange is almost nonexistent.

The traditional economic system relies on subsistence as the primary motive for economic trades, rather than profit. The system depends on local communities working together to provide for each other and sustain themselves.

While it may be considered primitive by some, it is a highly sustainable system that minimizes waste and ensures that only what is needed is produced.

This economic system operates at a micro level, with small tribes and local communities providing for each other. Countries like Bhutan and Haiti are examples of places where traditional economic systems are still in use today.

2. Socialism – Command economic system

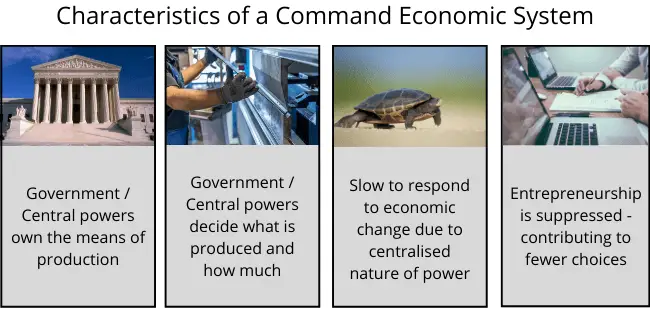

A command economic system, also known as a socialist or communist system, is characterised by centralisation of power to the government or a single ruler. Economic interactions are dictated by those in charge, who determine the rules of the game.

In this type of system, decisions about what goods to produce, how much to produce, and their prices are made by central authorities. These powers determine what is deemed socially optimal and allocate resources accordingly, whether it be for the production of consumer electronics or for investments in infrastructure or agriculture.

In a command economic system, the central powers own the means of production and have the authority to shift resources as they see fit. For example, they may move workers from one industry to another in order to fulfill long-term economic plans. These plans are a crucial aspect of command economies and are often carried out over several years, as seen in the five-year plans adopted in the Soviet Union.

However, this top-down planning can also be slow to adapt to changing economic trends. In some cases, the central powers may prioritize the production of a certain product or industry over others, regardless of demand. This can lead to inefficiencies and shortages, as people may want more of a particular product but the central powers are focused on producing another.

Examples include North Korea, Cuba, and the former Soviet Union.

3. Capitalism – Market economic system

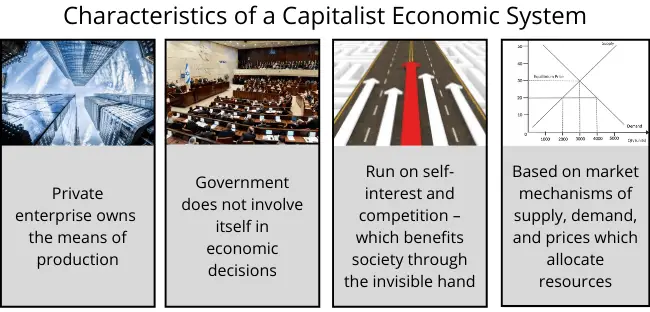

A capitalist economic system is characterized by private ownership and control of the means of production, rather than by government ownership. In this system, goods and services are produced in response to supply and demand, as opposed to being dictated by the government.

When consumers demand certain goods or services, it sends a signal to businesses to increase their production. Conversely, when demand decreases, businesses are signaled to decrease their production. This system also incentivizes businesses to innovate and offer new products that meet consumer demand.

Government involvement in a capitalist economic system is typically limited to enforcing laws and legal contracts. The economy is primarily regulated by market forces, including fluctuations in supply and demand, brand reputation, and competition.

The capitalist economic system relies on private individuals who use capital to produce goods and generate profit, thus increasing their private enterprise’s capital stock. However, this can result in the accumulation of great economic power and wealth among a few individuals, causing social unrest and unscrupulous business practices.

Private monopolies can emerge and overcharge consumers while providing low-quality goods, but some argue that the capitalist system is self-regulating over the long term. Monopolies are unable to persist as customers switch to competitors, and new businesses enter the market. Similarly, companies that offer inferior goods will be recognized for their poor quality and eventually go out of business.

4. Mixed Economy

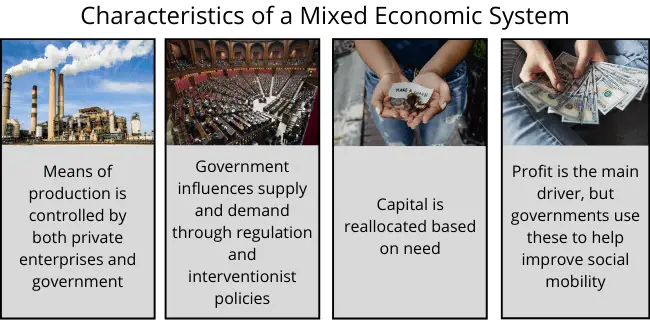

A mixed economy is a common economic system found in many developed nations worldwide, including the US, Japan, and most of Europe. This system is a blend of capitalist and command economic systems.

In a mixed economy, there is usually a level of private ownership of the means of production. However, some industries are controlled by the government, while others are privately owned. For example, in the UK, the government controls healthcare and the BBC, the main broadcaster.

The argument in favor of a mixed economy is that by combining aspects of a command and capitalist economy, we can achieve the best of both. However, there is a constant balancing act that must be achieved. Too much government intervention and markets may become suffocated, and the “invisible hand” has little effect, leading to shortages or wasteful oversupply. Conversely, too little government intervention may lead to unscrupulous business practices.

In a mixed economy, government involvement extends beyond mixed control of the means of production to include regulation and other forms of intervention. Subsidies, tariffs, and quotas are just some of the interventionist tools used by many mixed economy nations.

However, by using these tools, governments interfere with the supply and demand mechanism that allocates resources. Prices become distorted, and as a result, demand is artificially altered from its equilibrium with supply, which can contribute to shortages, undersupply, or other socially suboptimal outcomes.

Economic System Examples

United Kingdom (UK)

The UK is a mixed economic system with a partial command element, as the government owns entities such as the BBC, the NHS, and Network Rail. However, the majority of resources are owned by private enterprises, making it a capitalist economy.

Despite this, the UK government controls 40% of the economy due to its spending, which accounts for around 40% of GDP. This spending has a significant impact on resource allocation throughout the economy.

Government spending is primarily funded by taxation, though borrowing also plays a role. As a result, private resources are redirected into the hands of government officials who determine where and how to spend it. Overall, this demonstrates that the UK economy is a mixed system.

United States (USA)

The US, like the UK, is a mixed economy. The federal government owns entities like Amtrak, Fannie Mae, and Freddie Mac, while state governments own entities such as Alascom, New York Port Authority, and TVA. Although the majority of resources are owned by private enterprises, the government controls about 38% of the nation’s GDP. This means the US government decides where nearly 40% of the nation’s economic output goes, with a significant portion going towards the military.

Under a purely capitalist system, money would only be allocated to the military if it were profitable. In contrast, money is also diverted to numerous other government entities, which may not always align with public demands. However, the US government also imposes many regulations such as occupational licenses, which can limit individual business freedom and are commonly associated with command economies.

China

China’s economic system is unique as it originated from a command economy, making it distinct from the US and the UK. Although China has more characteristics of a command economy, it also exhibits a number of capitalist elements, which makes it a mixed system.

While private ownership of the means of production is limited, there are private enterprises in China, such as Amazon, Walmart, and Apple, with some involvement in the market. However, many companies are required to work with local suppliers to enter the market. The largest companies in China are state-owned, and corruption remains a significant issue in the country, with connections still playing a significant role in success.

Despite the government’s control over the majority of the means of production, China is still considered a mixed system. It has some level of private ownership and limited government involvement in certain sectors, which allows for supply and demand to interact.

With that said, China is a mixed system – despite government controlling the majority of the means of production. This is because it still has aspects of a capitalist system. There is some level of private ownership, and part of the economy has limited government involvement so allows supply and demand to interact.

FAQs

An economic system is a set of institutions, policies, and practices that determine how goods and services are produced, distributed, and consumed in a society.

The main 4 types of economic systems are:

1. Traditional Economic system

2. Socialist / Command Economic system

3. Capitalist / Market Economic system

4. Mixed Economic system

The US, UK, and most of Europe operate on a mixed economy. Although we know them as ‘capitalist’, they have a significant level of government involvement which cannot define it as a pure capitalist system. We also have the likes of North Korea and Cuba that operate under a command economic system that relies on government to control the means of production and allocate its output.

An economic system is the network that forms the economic relationships between individuals in society. In other words, how the people of a nation come together to create a complex whole.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Gross National Income Definition - GNI, or Gross National Income, is the total value of goods and services produced by a country's residents, including income…

Gross National Income Definition - GNI, or Gross National Income, is the total value of goods and services produced by a country's residents, including income…  Fixed Cost: Definition, Examples & Effects - A fixed cost is a cost that a business must pay whether it produces one good or a million. Regardless…

Fixed Cost: Definition, Examples & Effects - A fixed cost is a cost that a business must pay whether it produces one good or a million. Regardless…  Nash Equilibrium: Definition, Limitations & Example - Nash equilibrium refers to the situation whereby a group of individuals choose the most optimal strategy and do not deviate…

Nash Equilibrium: Definition, Limitations & Example - Nash equilibrium refers to the situation whereby a group of individuals choose the most optimal strategy and do not deviate…