Table of Contents ![]()

Monopolistic Competition: Characteristics & Examples

What is Monopolistic Competition?

Monopolistic Competition is a type of market structure where there are many firms in the market, but each offers a slightly different product. It is characterised by low barriers to entry and exit, which creates fierce competition.

As a result of low barriers to entry, new competitors constantly enter the market to prevent existing firms from making super-normal profits. One example of monopolistic competition is hairdressing. There are many firms which offer a slightly differentiated service, whilst competition is equally strong.

A market that has a Monopolistic structure can be seen as a mixture between a monopoly and perfect competition. Whilst monopoly and perfect competition are at completely different ends of the spectrum; monopolistic competition is somewhere in between. It is similar to a monopoly in the fact a firm can make supernormal profits in the short-term. Yet at the same time, there is easy market entry and exit, with few barriers to entry: similar to perfect competition.

In short, monopolistic competition is a market structure where many competitors sell slightly different products. In turn, they compete on factors other than price; such as quality, and reliability.

Key Points

- Monopolistic competition is a market structure in which many firms sell differentiated products.

- Each firm has some market power, meaning that they have the ability to set their own price to some extent.

- Product differentiation can be based on factors such as quality, design, features, or branding.

- Firms in monopolistic competition compete on price, product differentiation, and marketing efforts to attract customers.

Characteristics of Monopolistic Competition

1. Many buyers and sellers

Similar to perfect competition, there are many buyers and sellers in the market. However, there are fewer in Monopolistic Competition. Consumers have a wide variety of choices which is not offered by other market structures such as a monopoly or oligopoly.

2. Slightly differentiated products

Firms that operate in a monopolistic market have very similar products but are slightly differentiated to add value over the competition. Clothing markets are a prime example. There are many types of clothes, each with a slightly different style. This differentiation can be seen in four ways: Physical, Marketing, Human capital, and differentiation through distribution.

3. Maximise profits

Firms in a monopolistic market seek to maximize profit. In economics, this is where marginal costs equal marginal revenue. By doing so, the firm produces right up to the point whereby it becomes unprofitable to produce any more goods. To produce any further would create a loss for the firm. So up to this point, the firm is making a profit on producing an additional unit to sell.

4. Low barriers to entry and exit

New entrants are easily able to enter as there are none or very insignificant barriers to entry. The cost to start a new business is low and the risk involved in failing is also comparatively low. So the incentive to enter the market is high, whilst few tools are needed. In other words, there are many more people who are able and willing to compete.

5. Potential supernormal profits in the short term

Monopolistic firms can make supernormal profits if they can benefit from a gap in the market. Looking at clothing, for example, one company may create a new design that has never been done before.

If it goes down a hit with the customers, the firm benefits from high levels of demand. These lead to supernormal profits in the short-term until other firms become aware. They then try to make similar products, thereby reducing the level of profits of the original firm.

6. Normal profits in the long-run

Over the long-term, profits shrink as new entrants enter the market to compete. Due to low barriers to entry, new firms can see any supernormal profits that are made and come in to take their share. So whilst some firms may benefit from new products in the short-term, these supernormal profits are brought back down again with the introduction of competition.

7. Imperfect information

In perfect competition, the customer is able to gather information relatively easily as all products are the same. At the same time, the cost to gather information in a monopoly structure is relatively low as there is only one firm.

By contrast, in monopolistic competition, many firms offer slightly different products – which makes information gathering more time consuming and costly. Insurance is a prime example – which is why a number of comparison sites have come into existence.

8. Non-price competition

The market offers slightly different products, so businesses compete on product/service quality. This can come through shorter wait times or more attentive employees. At the same time, firms will also compete on other non-price factors such as location, branding/advertising, and quality.

Monopolistic Competition Examples

Taxi’s

Local taxi firms seek to differentiate themselves through factors such as pre-bookings, limousine service, or through a fleet of different cars. There are many firms in the market, yet cannot be considered perfectly competition due to: levels of differentiation, imperfect information on drivers, and the ability to make supernormal profits during peak periods.

Clothing markets

There are many clothing manufacturers that distinguish themselves based on style, yet also have a certain level of market power. At the same time, it is relatively straight forward to manufacture clothes, with low barriers to entry.

Hotels and pubs

There are thousands of hotels dotted over the country – each with a certain level of local market power. This classifies as monopolistic competition as there are many firms, each that offer a slightly different experience. At the same time, the cost to start a small hotel is relatively low. For instance, a business owner may be able to take out a loan to purchase a property, but they could leave the market relatively easily.

Restaurants

There are many separate restaurants all competing on the basis on slight differences. However, they are all competing for the same customer.

Hairdressing

Often a large number of firms that use quality of service as a differentiator. Many customers will come back to the same hairdresser as they obtain trust and offer a quality of service. At the same time, there are low barriers to entry, with new stores opening frequently.

Soap

There are many soap brands, each with a slightly different style and scent. It’s difficult to really tell the difference which is why some offer to ‘kill 99.9% of bacteria’ and other slogans.

Toilet Paper

A necessity product, but one that has many competitors offering slightly different qualities and styles.

Monopolistic Competition Graph

Short-run Curve

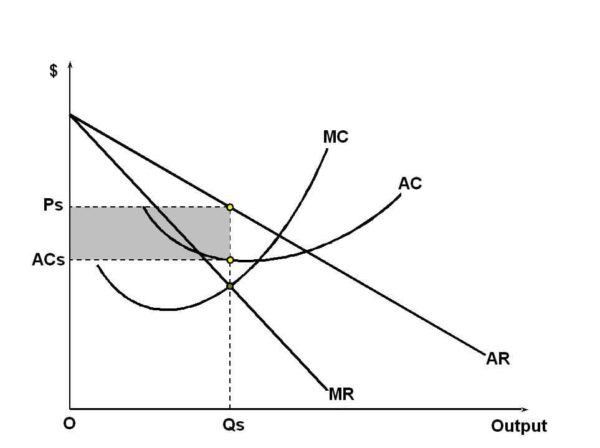

In the short-run, firms in monopolistic competition are able to make a supernormal profit. For example, a new clothing manufacturer may produce a new design that becomes an instant hit. In the short-term, customers flock to buy it.

However, competitors acknowledge this and will try and make similar designs, thereby taking customers back. In the long-run, competitors will flock into the market to make profits from the new design and reduce profits from supernormal to ‘ordinary’ profits.

As with all profit maximising firms, they will continue to produce until Marginal Revenue equals Marginal Cost. This means that if it is no longer profitable to produce a product, then the business will not do so. For example, Walmart will no longer sell its Cereal Brand for $2 if its Marginal Cost is greater.

As we can see from the graph above and below, average costs increase as new entrants enter the market. This is due to the fact that firms are unable to benefit from economies of scale.

To begin with, the firm making supernormal profits will increase production so that Marginal Costs = Marginal Revenue. However, when new businesses enter, they will take customers away; meaning the original firm will have to reduce production. In turn, this can lead to a more inefficient production process which increases the average cost to all businesses.

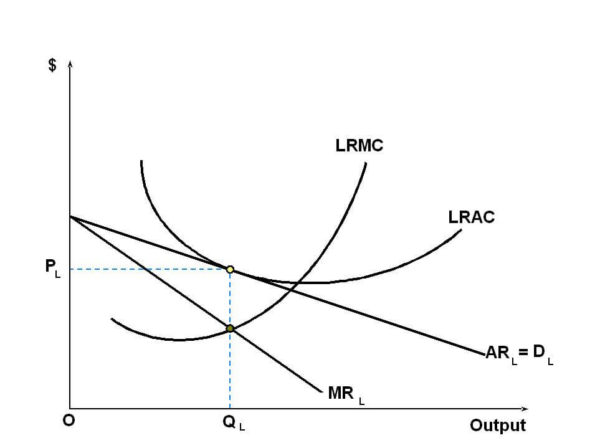

Long-run Curve

Over the long-run, average costs increase due to higher levels of competition, and profits fall to normalised levels. Firms will still aim to profit maximise, thereby increasing production until Marginal Revenue (MR) = Marginal Cost (MC).

This is shown on the diagram where MR and Long-run Marginal Cost (LRMC) intersects. The firm will then sell at the price at the point where it intersects the demand curve – which is at price PL. The long-run average costs then go through this point. At this point, the firm will make no profit in the long-run.

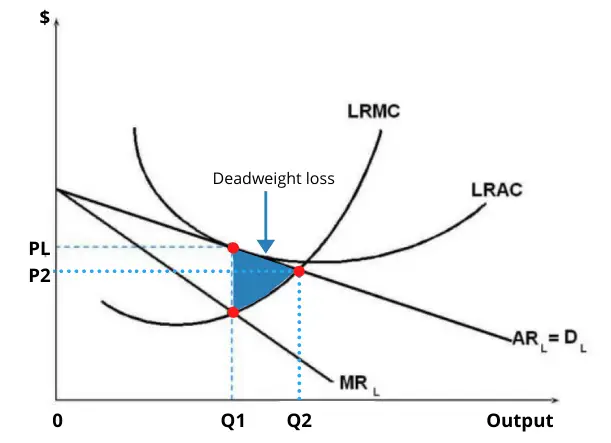

Deadweight Loss

In monopolistic competition, firms operate where MR = MC, which is shown at quantity Q1 on the graph. However, the firm could produce up to where demand is equal to long-run marginal cost. This is because, at this point, the firm is producing at the exact cost the consumer is willing to pay. Yet the firm chooses to produce at a lower quantity at Q1 because it seeks to maximise profits.

At Q2, it can produce more and sell more goods, but its profits would be lower because its marginal costs are in excess of its marginal revenue. So the firm looks to reduce output in order to maximise profits. However, this means that consumers who would otherwise be willing to pay a lower price are unable to do so because the firm seeks to maximise profits. In turn, this leads to a deadweight loss for society as output is not allocatively efficient.

Monopolistic Competition vs Perfect Competition vs Monopoly

So how does a Monopolistic market differ from that of Perfect Competition or Monopoly?

| Market Power | Number of Firms | Efficient Market | Product Differentiation | Profits | Elasticity of Demand | |

|---|---|---|---|---|---|---|

| Perfect Competition | None | Infinite | Yes | No | Ordinary profits | Perfect Elasticity |

| Monopolistic Competition | Low | Many | Not efficient | Mild levels | Supernatural in short-term / oridinary in long-term | Highly elastic in long-run |

| Monopoly | High | One | Not efficient | Only across industries | Supernatural | Inelastic |

Number of Firms

First of all, the number of firms is relatively low. As there is more than one firm, it does not classify as a monopoly, but significantly fewer than under perfect competition. This is due to the fact that in monopolistic competition, many firms slightly differentiate themselves from each other.

As a result, new entrants seek to add value in a slightly different way. In the end, this limits the number of firms that are willing and able to enter the market; but not significantly enough to deter the plethora of competitors.

Market Power

It is also important to highlight that in monopolistic competition, firms actually have very low market power. Firms have little ability to set prices and are instead ‘price takers’ which means they have to follow industry norms.

Whilst it sounds similar to monopoly; the ability of individual firms to set prices in the market is non-existent. None really have a significant market share, so are unable to force the hand of competitors. So unlike a monopoly, firms in monopolistic competition cannot set prices. Yet they have more power than under perfect competition.

Efficiency

Firms in both a monopoly and under monopolistic competition are inefficient; largely in contrast to perfect competition. To explain, firms in monopolistic competition are inefficient due to two main reasons: first of all, it operates with excess capacity; and second of all, it charges a price that is in excess of marginal cost.

Product Differentiation

Under monopolistic competition, firms slightly differentiate their products. For example, tea bags rely on quality and brand name to differentiate, yet under a perfectly competitive market, they would be exactly the same.

Profits

In a monopolistic market, profits can range from supernormal in the short-term, to ordinary in the long-term. By contrast, perfect competition is generally locked in equilibrium, only earning small amounts of profit. We then have a monopoly market, which, quite understandably, makes supernormal profits.

Elasticity of Demand

Demand in monopolistic competition can be highly elastic as there are a number of competitors. Switching costs are low, so consumers are easily able to switch to substitute goods. By contrast, perfect competition is perfectly elastic due to the infinite number of competitors. We then have monopolies which are purely inelastic. This is largely as a result of the lack of competition which leaves consumers with little choice but to pay the higher prices.

Related Topics

FAQs

An example of monopolistic competition are local taxi’s. Firms seek to differentiate themselves through factors such as pre-bookings, limousine service, or through a fleet of different cars. There are many firms in the market, yet cannot be considered perfectly competition due to: levels of differentiation, imperfect information on drivers, and the ability to make supernormal profits during peak periods.

There are 8 main characteristics of monopolistic competition:

1. Many buyers and sellers

2. Slight differentiated products

3. Maximise profits

4. Low barriers to entry and exit

5. Potential supernormal profits in the short term

6. Normal profits in the long-run

7. Imperfect information

8. Non-price competition

A market that has Monopolistic structure can be seen as a mixture between a monopoly and perfect competition. Whilst monopoly and perfect competition are at completely different ends of the spectrum; monopolistic competition is somewhere in between. It is similar to a monopoly in the fact a firm can make supernormal profits; in the short-term. Yet at the same time, there is easy market entry and exit, with few barriers to entry: similar to perfect competition.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Money Laundering - Money laundering is the process of disguising the origins of illegally obtained money to make it appear legitimate.

Money Laundering - Money laundering is the process of disguising the origins of illegally obtained money to make it appear legitimate.  Normative Economics - Normative economics is the branch of economics that involves making value judgments and subjective recommendations about what economic policies and…

Normative Economics - Normative economics is the branch of economics that involves making value judgments and subjective recommendations about what economic policies and…  Fixed Cost: Definition, Examples & Effects - A fixed cost is a cost that a business must pay whether it produces one good or a million. Regardless…

Fixed Cost: Definition, Examples & Effects - A fixed cost is a cost that a business must pay whether it produces one good or a million. Regardless…