Allocative Efficiency: What it is & Examples

What is Allocative Efficiency?

Allocative efficiency occurs when consumer demand is completely met by supply. In other words, businesses are providing the exact supply that consumers want.

For instance, a baker has 10 customers wanting an iced doughnut. The baker had made exactly 10 that morning – meaning there is allocative efficiency. Neither too few doughnuts were made, nor too many – which means no waste in terms of having to throw away doughnuts, nor unsatisfied customers wanting doughnuts.

Key Points

- Allocative efficiency occurs from the producers side as well as the consumers side. This is when demand is fully met, and production is optimised until marginal costs = marginal revenue – therefore no more profits are made.

- In economics, allocative efficiency occurs at the point where supply and demand intersect. This is also known as the equilibrium.

- In order to achieve allocative efficiency, markets must be competitive and free of externalities, monopolies, and other market distortions. In such a market, prices serve as signals of relative scarcity, and producers respond to those signals by allocating resources efficiently.

The second component occurs when consumers pay the marginal cost of production. In other words, businesses stop producing when the cost is higher than the price they can sell for. Just think of the supermarket making a loaf of bread, costing it $2, and selling it at $1.50.

Quite simply, allocative efficiency occurs where there is efficiency both from the consumers point of view, but also for that of the producer. That means there are enough goods to satisfy consumer demand, but also enough demand to maximise business profits – also known as Marginal Cost = Marginal Revenue.

Producer Side

To expand, the first side of allocative efficiency comes from the producer. When the market is allocatively efficient, the producer will continue to produce more and more up till the point where marginal cost is equal to price. In other words, where it no longer makes a profit. This is where the cost to make an additional good is equal to the price that it sells that good for. This may be due to a number of factors which make the good more expensive to produce as production increases (also known as diseconomies of scale).

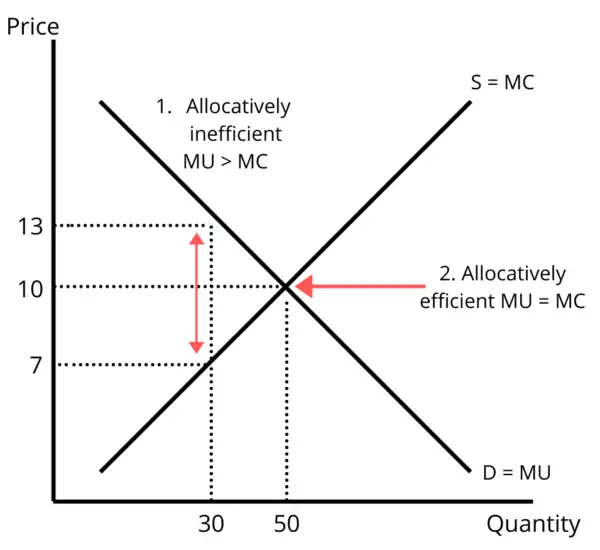

As we can tell from the chart below, the business will continue producing until the supply and demand curve intersect. In an allocatively efficient market, this would be where marginal cost equals marginal utility. This is also known as the equilibrium point – marked up as 2 below. If the producer produces at a lower quantity, there will be excess demand — meaning it is not allocatively efficient from the consumers side.

Consumer Side

From the consumer’s perspective, a market is allocatively efficient when the price reflects the maximum they are willing to pay. In other words, allocative efficiency is where the consumers satisfaction is maximized in relation to cost. For instance, the consumer may be willing to spend a maximum of $5 on a bagel. This is the price at which maximizes the consumer’s utility, but also the price paid to the producer.

As the price increases, the level of utility or satisfaction decreases. For instance, few would enjoy a croissant if they had to pay $50 for it. So allocative efficiency is where consumers maximize their utility, but also the price they pay.

Understanding Allocative Efficiency

We have looked at the producer and consumer side of allocative efficiency. So let us now define this in more detail.

In order to be allocatively efficient, the market must meet two criteria. The first is from the producer side. The producer must supply the market up until it is no longer profitable to produce another good. However, this must also fit in line with the second factor. This must also be at the price which maximises marginal utility. As we can see in the graph below, the two points must intersect to classify as allocatively efficient.

So in short, allocative efficiency applies when producers continue production up until a point where its marginal costs align to the maximum utility and price a consumer would be willing to pay.

Examples of Allocative Efficiency

The principle of allocative efficiency can be illustrated through several real-world examples across various sectors. Here are some instances where allocative efficiency comes into play:

- Agricultural Market The farming industry often closely approximates the condition of perfect competition, which leads to allocative efficiency. Many individual farmers produce the same goods (like wheat or corn) and compete with each other to sell them. If the market for corn, for instance, signals higher prices due to increased demand, farmers may shift their production to more corn and less of other crops, thus matching the production cost to consumers’ willingness to pay.

- Stock Market When operating efficiently, the stock market can represent allocative efficiency. Stock prices ideally reflect all the available information about the value of a company. This means that capital is allocated to firms where investors expect the highest return, thus aligning with the principles of allocative efficiency.

- Online Retailers Online retail platforms, such as Amazon and eBay, host numerous sellers providing similar products. Competition among these sellers tends to align the price with the marginal cost, demonstrating allocative efficiency. It’s particularly true for common and standardized goods such as books or electronic accessories.

- Commodities Market Markets for commodities such as oil, gold, and other raw materials tend to display allocative efficiency. The prices of these commodities are driven by global supply and demand. If demand for oil increases, the price rises, incentivizing producers to increase their supply until the price matches the cost of producing the last unit of oil.

Remember, these examples are simplifications. Real-world markets often exhibit imperfections, such as barriers to entry, information asymmetry, externalities, and market power, which prevent them from achieving perfect allocative efficiency. However, they serve to illustrate the concept and how it operates in different scenarios.

Allocative Efficiency vs Productive Efficiency

In economics, understanding the concepts of efficiency is fundamental to grasping how resources can be best allocated. There are two key types of efficiency: allocative efficiency and productive efficiency. Both concepts aim to optimize resource use, but they approach this goal from different angles.

Allocative efficiency, also known as Pareto efficiency, occurs when goods and services within an economy are distributed optimally in response to consumer preferences. This means that the allocation of resources corresponds to consumer demand, and goods are produced at a price that reflects their marginal cost. When an economy achieves allocative efficiency, it maximizes social welfare because every good or service is produced up to the point where the last unit provides a marginal benefit to consumers equal to the marginal cost of supply.

On the other hand, productive efficiency, also known as technical efficiency, focuses on the production side of economic activity. Productive efficiency is achieved when a good or service is produced at the lowest possible cost. This means that businesses use the fewest inputs, such as labor and capital, to achieve a given level of output. Productive efficiency emphasizes cost minimization and is generally achieved through economies of scale and the optimization of production processes.

While both allocative and productive efficiency contribute to economic welfare, they focus on different aspects of the market. Allocative efficiency looks at the ‘what’ and ‘for whom’ questions of economics – what goods and services are produced and who gets them. Conversely, productive efficiency focuses on the ‘how’ question – how are these goods and services produced. Both types of efficiency are essential for an economy to function optimally and use its resources in the best possible way.

Allocative Efficiency in Perfect Competition

In economics, allocative efficiency represents an optimal distribution of goods and services, taking into account consumer preferences. In a state of allocative efficiency, the price of goods or services is equal to the marginal cost (MC) of production. This means that the goods are being distributed to the consumers who value them the most.

Perfect competition is a theoretical market structure that features many buyers and sellers, identical products, and no barriers to entry or exit. Under perfect competition, firms are price takers as they don’t have any market power to influence the price.

Allocative efficiency is achieved in perfect competition for the following reasons:

- Price Equals Marginal Cost (P=MC) In a perfectly competitive market, price is equal to the marginal cost of production. This is because the competition among firms drives prices down to their minimum, which is the point where the marginal cost of producing an additional unit equals the price that consumers are willing to pay for it. Thus, resources are allocated to their most efficient use as firms will not produce goods at a price less than the marginal cost of production.

- Consumer and Producer Surplus Maximization Perfect competition also ensures that the combined surplus of consumers (consumer surplus) and producers (producer surplus) is maximized. This is another condition for allocative efficiency.

- Optimal Output Level In a perfectly competitive market, each firm produces at a level where the marginal cost is equal to the market price, thereby maximizing profit. This profit-maximizing condition also ensures that the total output of the market is at an optimal level.

- No Externalities Perfect competition assumes that there are no externalities or costs that are not internalized by the market participants. This means that the private costs and benefits of production and consumption coincide with the social costs and benefits. Hence, the market outcome is socially optimal, reflecting allocative efficiency.

It’s important to remember that perfect competition is a theoretical concept, and real-world markets may not fully meet these conditions. However, it serves as a benchmark to gauge the efficiency of real markets and understand how market structure can affect resource allocation.

FAQs

It is where demand is fully met by supply, with no excess. In other words, the amount supplied to market equals exactly the amount that is demanded.

One example is where a bakery makes baked goods. It produces 100 loaves of bread for customers. In the same day that those loaves are made, there are exactly 100 customers that come in looking for a loaf of bread. The baker has supplied 100 loaves, and equally, 100 loaves have been purchased – resulting in allocative efficiency.

Allocative efficiency comes as a result of the supplier knowing exactly how many goods they need to provide to the market. That way, the supplier can reduce any excess waste and capacity and the consumer is always able to get the goods they want.

Allocative efficiency is important because it leads to the highest possible level of consumer satisfaction and social welfare. It ensures that resources are being used in a way that maximizes the net benefits to society.

Yes, government intervention can improve allocative efficiency by correcting market failures through the use of taxes, subsidies, and regulations, or by providing public goods and services that are undersupplied by the private sector.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Related Topics

Further Reading

Cash Cow - A cash cow refers to a business or product that generates a steady and significant cash flow with minimal investment…

Cash Cow - A cash cow refers to a business or product that generates a steady and significant cash flow with minimal investment…  Degrees of Freedom - Degrees of freedom refers to the number of independent variables or data points that can vary in statistical analysis.

Degrees of Freedom - Degrees of freedom refers to the number of independent variables or data points that can vary in statistical analysis.  Consumerism - Consumerism is a socio-economic ideology that promotes the acquisition and consumption of goods and services as a measure of individual…

Consumerism - Consumerism is a socio-economic ideology that promotes the acquisition and consumption of goods and services as a measure of individual…