Law of Supply: Definition & Example

Law of Supply in Economics

In economics, supply is the number of goods an individual or business provides to the market – which refers to the amount they produce at a specific point in time. For example, if Apple manufactures 100 iPhones, then this is the supply that is brought to the market.

The law of supply simply refers to the relationship between prices and supply. As prices increase, so too does supply. If prices fall, then supply will also fall. However, it is important to note that this only applies ceteris paribus. In other words, all other variables are kept constant. So factors such as increasing costs or more competition are not considered and are held constant.

Higher prices give businesses an incentive to increase supply. For example, a motor vehicle manufacturer may take several actions in response to higher prices. It may expand production and invest in new factories. It may hire more workers. It may open its existing factories for longer. Or it may introduce a monetary reward to encourage its workers to improve their efficiency.

Key Points

- The law of supply states that at higher prices, businesses with supply more of the good to market.

- According to the law of supply, it assumes that all other factors are kept equal. In other words, higher prices leads to higher supply if all other variables remain the same.

- Other factors that can affect supply include changes in the cost of production, number of competitors, technology, and future price expectations.

Law of Supply Example

Let us take an example and say a bakery supplies 200 loaves of bread each day to its customers. Its staff work in the morning and supply them to customers when the shop opens. The supply of bread is therefore 200 loaves.

When looking at supply, it reacts to demand and prices. When demand increases, two things can happen. The bakery raises its prices, or it tries to make more loaves of bread – increasing supply.

The bakery is not going to supply more loaves of bread if there are no customers to buy them. That is wasteful and inefficient. They would have to throw good loaves away each day.

They will only start supplying more loaves of bread if they see they are selling out before the end of the day. If more customers come in wanting bread, this sends a clear signal that they need to increase supply.

The bakery may increase prices to capture extra profits, which would reduce demand, as many customers would no longer be willing to pay such a price.

Alternatively, it could hire more employees and increase the supply of bread. Or, in some cases, the store may increase prices and use those extra profits to invest in a new bread maker. This could help increase the productivity of its existing staff. They could then produce many more loaves of bread at the same time.

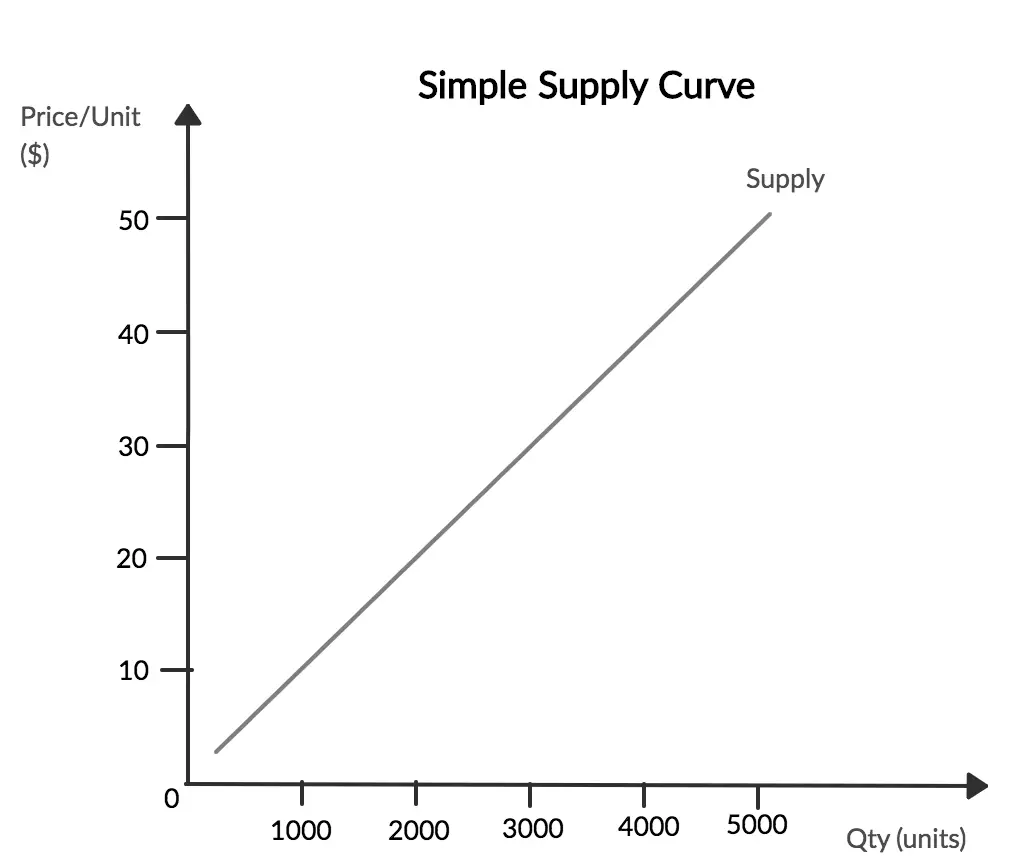

Law of Supply Curve

The supply curve shows the relationship between the number of goods produced and the price. As we can see from the graph below, the line goes from the bottom left towards the top right. This demonstrates that as supply increases, so to do prices. Similarly, as prices fall, supply also falls.

On the supply curve, there are two variables: price and supply. In the formulation of the supply curve, price is known as an independent variable. This means that it goes up and down no matter what supply does. It is not linked to supply in the fact that its variation does not depend on it.

By contrast, supply is known as a dependent variable in the supply curve. This means that supply only increases or decreases in reaction to price. So when prices increase, businesses look to expand output to capture those profits.

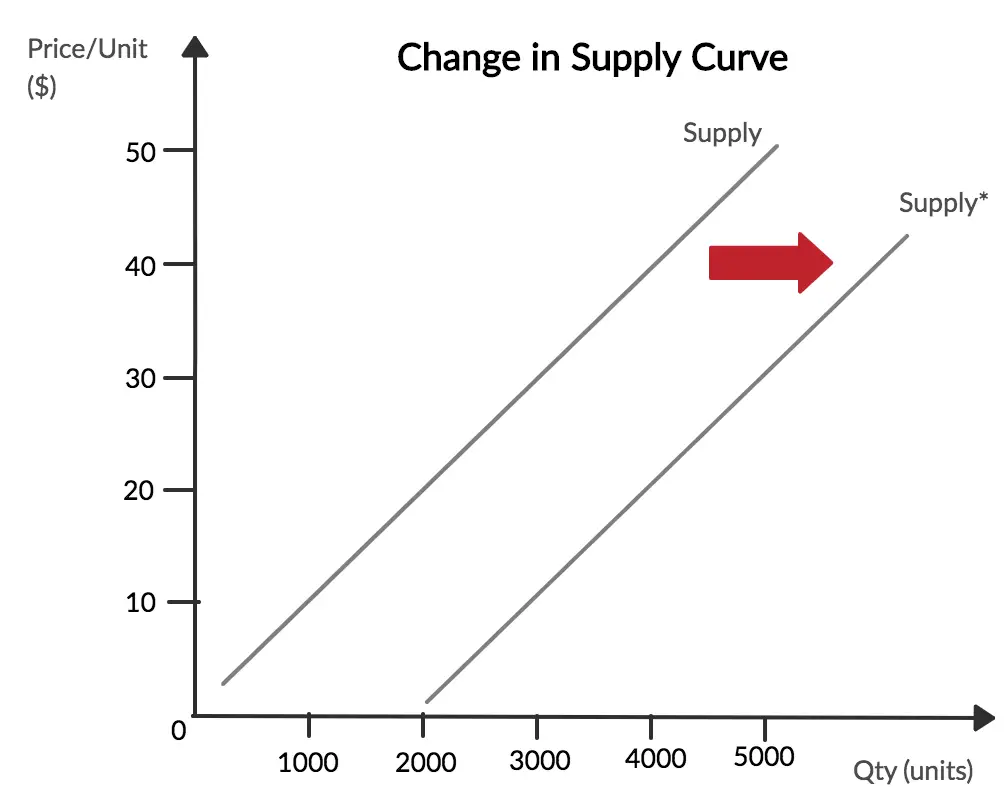

Factors Affecting the Law of Supply – Shifts in the Supply Curve

In reality, supply is not always consistent. It can increase and decrease irrelevant of price. For example, a bad harvest may reduce the amount of grain produced in one year. This can push the supply curve left, meaning the price paid would be the same, just at a lower quantity supplied.

The supply curve only shifts when there is a factor in play that does not relate to price. This shift can happen for a number of reasons:

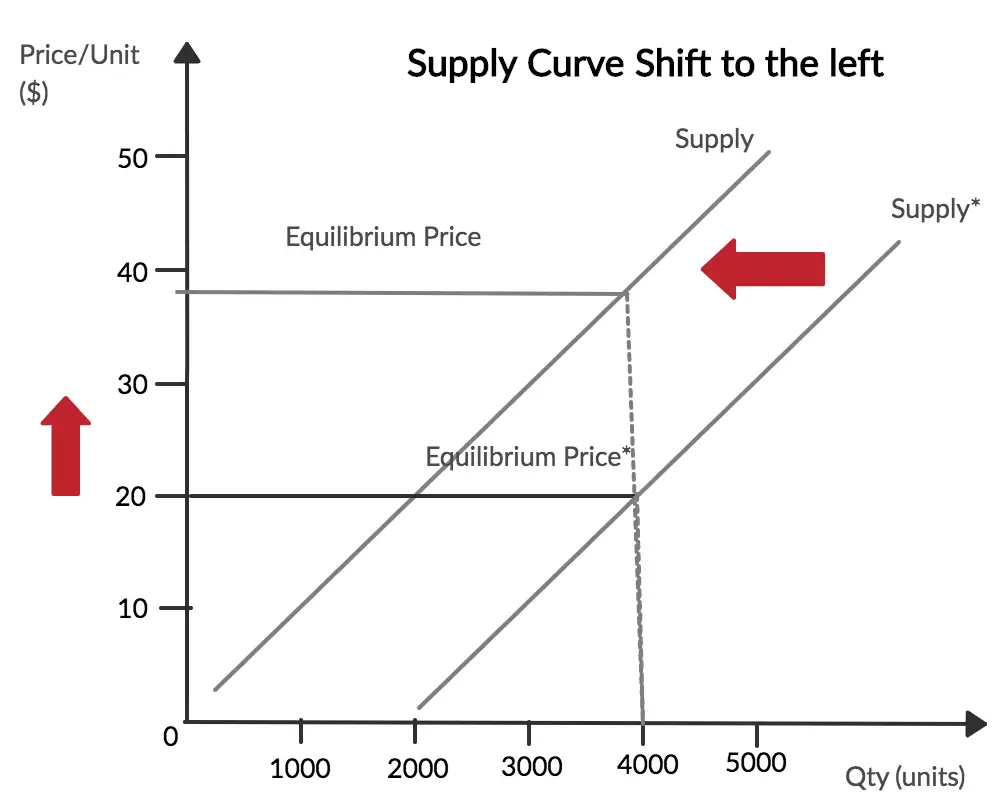

1. Changes to the Cost of Production

When the price of an input increases, supply decreases. This is because the producer of a good or service is less likely to produce it when costs are higher. For example, a Television manufacturer may see the price of its screens go up.

This means that the cost to manufacture televisions has increased. As a result, the manufacturer is unlikely to sell at the same price and quantity following the higher costs. The supply curve then shifts to the left. This demonstrates that when the cost of production increases, producers will only supply the same quantity at a higher price.

As we can see from the graph below, a shift in the supply curve to the left means that in order to maintain the same quantity, prices must also increase.

Lower costs of production can also shift the supply curve to the right. This means that at the same quantity, prices will be lower. For example, there may be a new piece of machinery that is able to help increase productivity. Workers can then supply twice as much. Supply then shifts to the right, meaning that the same supply will reach the market at a lower price.

2. Number of Sellers

When new businesses enter the market, supply increases, moving the supply curve to the right. If a new barber opens in the same neighborhood, there is a greater supply. This puts a downwards pressure on other barbers to reduce their prices. As a result, a higher quantity is provided, but at a lower price.

In the same fashion, when businesses leave the market, there is reduced supply and the supply curve shifts to the left. For example, the local barbers may close, meaning there is now only one barber in town. The supply has fallen, so the curve shifts left. In essence, this means that prices will go up to represent the reduced supply.

3. Technology

The use of new and advanced technology can push the supply curve to the right. As new innovative techniques enter the supply chain, businesses can create more products. For example, in a manufacturing plant, there may be a new piece of technology that is able to speed up the production process. As a result, it may be able to manufacture twice as many motor vehicles a day.

4. Natural and Social Factors

Natural and social factors generally cause the supply curve to shift to the left by reducing supply. In terms of natural factors, this could include something like a hurricane, the weather, or even a poor harvest.

Ice cream vans, for example, are unlikely to supply their services during periods of heavy rain. In the same fashion, social factors such as higher government taxes or a minimum wage may increase the cost of production. In turn, this can also push the supply curve to the left.

By contrast, favourable weather conditions can actually increase supply and shift the supply curve to the right. Nice sunny days are more likely to attract ice cream vans. Similarly, lower taxes put lower price pressures on businesses, which can react by increasing supply.

5. Future Expectations

The expectation of the seller is crucially important. When sellers expect future demand to rise, they may hold back supply in order to capture increased demand. This would reduce supply and shift the supply curve to the left.

For example, restaurants may increase the number of Turkeys that have in the run-up to Thanks Giving and Christmas. This is why some products can actually decrease in price during peak periods. Ice cream is another example. Manufacturers generally ramp up production coming into the summer months in order to meet future demand.

FAQs on Law of Supply

The basic law of supply is that at higher prices, producers will bring more of the product to market – driven by higher profits. In addition, at lower prices, producers will bring fewer goods to market as it becomes less profitable for them.

The law of supply is important as it is fundamental to economic thinking. When policymakers place a cap on prices, it is important to understand that lower prices means lower supply – so there are actually fewer goods provided to market.

There are many factors that affect supply, including production costs, technology, the prices of related goods in production, expectations about future prices, government policies and regulations, and the number of sellers in the market.

A change in supply is where the supply curve shifts as a result of factors other than price. For instance, advances in technology, changes in government policy, or increased costs. By contrast, a change in quantity supplied is where there is movement along the supply curve, which is as a result of a change in price.

Some exceptions to the law of supply include the case of goods with a limited supply (e.g., rare artwork or collectibles), where the quantity supplied remains constant regardless of price changes. Another exception can occur with certain agricultural products, where short-term supply may be relatively inelastic due to the time it takes to grow and harvest crops.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Related Topics

Further Reading

Bait and Switch - Bait and switch is a deceptive sales tactic that involves advertising a desirable product or offer to attract customers, only…

Bait and Switch - Bait and switch is a deceptive sales tactic that involves advertising a desirable product or offer to attract customers, only…  Marginal Revenue: How to Calculate with Formula & Example - Marginal Revenue is the money a firm makes for each additional sale. So if a baker sells an additional loaf…

Marginal Revenue: How to Calculate with Formula & Example - Marginal Revenue is the money a firm makes for each additional sale. So if a baker sells an additional loaf…  Monetary Policy Definition - Monetary policy encompasses measures implemented by a central bank or financial regulator to control a nation's money supply and accomplish…

Monetary Policy Definition - Monetary policy encompasses measures implemented by a central bank or financial regulator to control a nation's money supply and accomplish…