Table of Contents ![]()

Effects of Inflation: Positives & Negatives

Effects of Inflation

Inflation is not a new phenomenon; it has been well studied over the years, and its effects have been widely researched. That is why Central Banks try to keep its rate at around 2 percent. This is because too much inflation can lead to hyperinflation, as seen in the Weimar Republic or Venezuela today. While inflation can help stimulate economic activity, too much of it can destroy it.

Below, we will look at the main effects of inflation. However, it is important to note that these effects depend on the rate of inflation. For instance, a rate of 2 percent will not have the same effect as a rate of 100 percent per year. Therefore, we will primarily look at the effects that occur from prolonged and sustained levels of inflation that exceed 2 percent.

Key Points

- One of the most crucial effects of inflation is the loss of purchasing power.

- Those who have savings tend to lose to inflation, whilst those with debts generally benefit.

- Whilst the effects of inflation are seen as largely negative, there are some positives. For instance, it can help reduce the debt burden for private households and governments.

Negative Effects of Inflation

1. Money Loses its Value

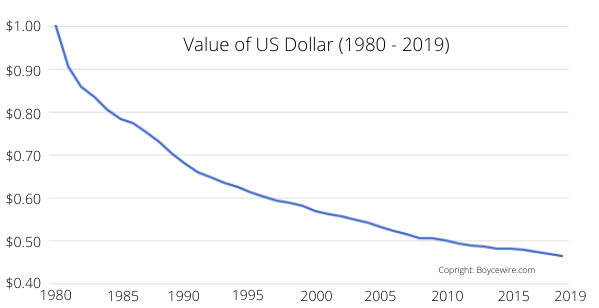

When the prices of products go up, the value of money decreases. For instance, if you keep $1 under your pillow for ten years, it will not have the same purchasing power as it does today due to inflation.

If we examine the value of the US dollar from 1980 to 2019, we can observe that it has lost over half its value. This implies that you can buy only half as many goods and services with one dollar as you could thirty years ago. Therefore, if you had kept $1,000 under your bed in 1980, it would be worth less than $500 today.

Inflation prompts consumers to seek a return on their capital because their purchasing power is reduced. They search for better returns instead of leaving their money in low-interest bank accounts or under the mattress. Consumers are concerned that the money they saved over the years may lose its value.

Furthermore, inflation creates pressure on businesses to invest any extra capital they have. Money that is not utilized is losing its value if it is not invested in the stock market or another form of investment.

2. Inequality

Inflation can harm low-income households the most since they spend the largest percentage of their income. Thus, when prices go up, it takes up a significant portion of their income. For example, if the price of necessities like food and housing increases, the poor have no choice but to pay more. A $10 per week increase in food prices impacts someone earning $12,000 a year more profoundly than someone earning $50,000.

Inflation tends to increase asset prices, including housing, the stock market, and commodities like gold, which outpace inflation. This creates inequality since richer households have more assets, including property, shares, and other assets. As a result, when inflation occurs, these assets increase in price more quickly than everyday goods such as bread, milk, and eggs. This allows the wealthy to acquire more wealth that can purchase more goods and services than before. Conversely, low-income households spend more to make ends meet.

Those with lower incomes tend to spend more of their income, so they have less to save and invest in stocks, bonds, and other assets. Moreover, they are unable to afford high capital expenses like a house. As a result, those who invest some of their income in inflation-protected assets such as stocks are left better off than those who cannot.

3. Exchange Rate Fluctuations

Increase in Money Supply

When the money supply and prices increase, a country’s currency can lose its value. For instance, if there is $1 million in circulation in the US and YEN30 million in China, the exchange rate could be 1:30. However, if the Federal Reserve creates an additional $1 million, making the total $2 million, the ratio may fall to 1:15. This is merely an indication, as the exchange markets fluctuate daily. Nonetheless, the concept remains the same: when prices inflate and the money supply expands, the currency’s value against other currencies declines.

Consider another scenario. A Chinese vase is worth YEN 100, which is exchanged with the US for a barrel of American oil worth $25. This results in an exchange rate of 1:4. However, when the Chinese print more money and inflation raises the vase’s price to YEN 200, its value to the US remains unchanged. Thus, they would not want to trade two barrels of oil for the same vase suddenly. Consequently, the exchange rate adjusts to the new reality. With the American oil worth $25 and the Chinese vase now worth YEN 200, the exchange rate increases to 1:8.

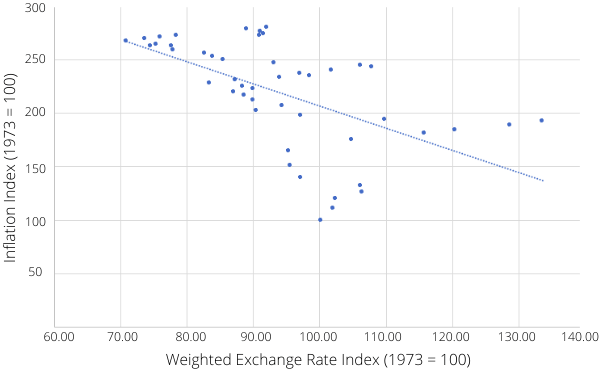

US Index Comparison between Inflation and the Weighted Exchange Rate

Exchange Rate Decline Causes Inflation

As we can see from the chart above, there is a relative correlation between inflation and the exchange rate. However, that does not necessarily mean that inflation causes the exchange rate to fluctuate. Often, inflation can result from other factors that contribute to exchange rate fluctuations. In other words, a fall in the exchange rate causes inflation rather than the other way around.

Although an increase in the money supply can create inflation and cause the exchange rate to fall, a decline in the exchange rate can create cost-push inflation. Simply, this is where the price of imported goods increases as the domestic currency can buy fewer goods. This may be a result of having a trade deficit, poor economic performance, or high-interest rates.

4. Impact on the Cost of Borrowing

If you borrow $200,000 through a mortgage, you have to pay that amount back, plus interest, over a 25-year period at a 5 percent interest rate. The total cost over 25 years will exceed $345,000, with over $145,000 in interest expenses alone.

However, when we factor in inflation over the last 25 years (1995-2020), the actual cost is $205,000. In other words, the total cost of $345,000 in 2020 prices is equal to $205,000 in 1995 prices. Thus, although the repayment amount appears exorbitant, inflation reduces the cost.

To put it differently, the borrowed amount loses value every year, reducing the resources required to repay the debt. For example, a debtor earning $20,000 annually after taxes takes out a $40,000 loan, which equals two years’ worth of wages. After five years, inflation increases their wages to $40,000, which is now equivalent to one year’s worth of wages.

However, consistent and high levels of inflation may prompt financial institutions to raise their rates to protect themselves from inflationary pressures. Consequently, debtors may find it harder to obtain credit.

5. Increased Cost of Living

As the prices of goods increase, consumers have to pay more to purchase basic necessities and luxuries alike. This may not be an issue if incomes rise in proportion to inflation, but those who do not experience this will face higher real prices. In other words, they must spend a greater portion of their income on the same quantity of goods.

Furthermore, inflation pushes taxpayers into higher tax brackets, resulting in higher taxes for some. If the brackets are not adjusted adequately to reflect the new reality, they may end up worse off.

Low-skilled employees are also significantly impacted as their wages are relatively inflexible due to intense market competition. With many low-skilled workers vying for employment, employers wield significant power, resulting in wages lagging behind the rest of the economy, making them worse off. Furthermore, minimum wage increases do not always keep pace with inflation, putting additional downward pressure on wages.

Positive Effects of Inflation

1. Increased Spending and Investment

As inflation rises, consumers are encouraged to make purchasing decisions earlier. Instead of waiting until next year when a product will cost more, consumers choose to buy now to avoid paying more later.

For the typical consumer, this involves purchasing new cars, refrigerators, phones, and other consumer goods. However, this extends beyond consumer goods. Consumers are also motivated to seek the best return on investment. As money loses its value under inflation, it is necessary to “beat” inflation to maintain the same purchasing power.

For example, a consumer may have $1,000 in the bank, but they are only earning a 1 percent interest rate. If inflation consistently sits at 3 percent, they lose money year after year. Therefore, they can either let inflation take its toll and see their money’s value diminish or try to find higher-yielding investments. This can benefit the economy since savers are looking to move their money to the most productive areas of the economy.

Nevertheless, this poses a risk because the average consumer may lack the necessary knowledge or skills to make sound investments. As a result, there is a higher chance of economic losses due to poor money management.

2. Higher Asset Prices

Historically, asset prices have risen more quickly than inflation. For instance, long-term house prices have historically outpaced inflation. In 1980, the average house sold in the US for $74,500, which is worth $231,000 in 2019 dollars when adjusted for inflation. In comparison, the average house sold for $375,000 in 2019, resulting in a significant $144,000 in real gains over 39 years.

The stock market is another prime example. Since the creation of the S&P 500 in 1926, it has returned an average of over 10 percent annually. After accounting for inflation, it has yielded a return of over 7 percent above inflation.

During periods of consistent inflation, consumers and businesses tend to speed up their purchasing decisions and spend more rapidly. They may also move their capital into illiquid assets such as stocks, bonds, and real estate. In reality, a combination of both tends to happen.

As a result of the higher levels of spending and the move toward illiquid assets, consistent inflationary environments are created. Individuals seek out investments that can better protect against the eroding effects of inflation, leading to increasing asset prices.

3. Reduces Effective Level of Debt

Whether it’s a business, government, or consumer, those with high levels of debt may actually benefit from higher levels of inflation. For example, if a borrower has an interest rate of 2 percent on their debt, and inflation is at 10 percent while their income increases at a similar rate, the effective rate at which they are repaying declines.

While this can be a positive effect of inflation for those in debt, it can be a significant disadvantage for individuals such as savers and institutions such as banks. Banks lose out because they are receiving lower levels of interest than the rate of inflation, and savers are likely to earn interest below the rate of inflation.

4. It’s better than Deflation

Economists debate the optimal rate of inflation, but generally agree that any positive inflation is better than deflation.

Deflation can be more detrimental to an economy than inflation because it increases the debt burden for governments, businesses, and individuals. This can lead to a paralysis of public services and a large number of bankruptcies as firms struggle to repay debt that becomes more expensive due to deflation.

Related Topics

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

GDP: Definition, How to Calculate & Characteristics - Gross Domestic Product (GDP) refers to a nations economic output, including the goods it produces and services it sells.

GDP: Definition, How to Calculate & Characteristics - Gross Domestic Product (GDP) refers to a nations economic output, including the goods it produces and services it sells.  Marginal Benefit Definition and Examples - Marginal benefit is the extra benefit or utility that an individual receives from consuming or producing one additional unit of…

Marginal Benefit Definition and Examples - Marginal benefit is the extra benefit or utility that an individual receives from consuming or producing one additional unit of…  Central Bank: Definition, Objectives & Functions - A central bank controls the supply of money as well as how it reaches the consumer.

Central Bank: Definition, Objectives & Functions - A central bank controls the supply of money as well as how it reaches the consumer.