Centrally Planned Economy: Definition, Comparisons & Examples

What is a Centrally Planned Economy?

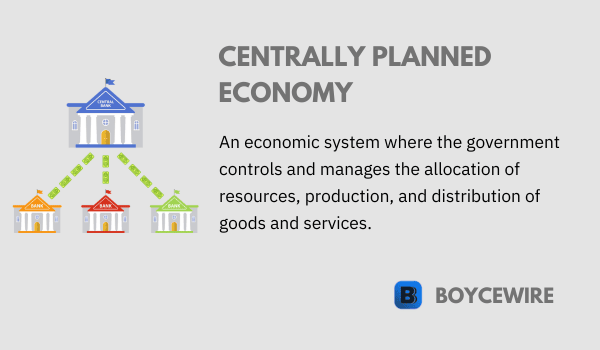

A centrally planned economy, also known as a command economy, is an economic system in which a central authority, usually a government, makes all decisions about the production and consumption of goods and services. This system stands in contrast to a market economy, where these decisions are guided by the invisible hand of supply and demand.

The origin of centrally planned economies can be traced back to societies which believed in collective ownership of resources and where decisions were made with the goal of societal benefit. This type of economic structure has been adopted by several nations throughout history, notably the former Soviet Union and Maoist China, and is still found today in countries like North Korea and Cuba.

Key Points

- In a centrally planned economy, the government plays a central role in making economic decisions and determining the allocation of resources.

- The government plans and directs production, sets prices, and decides on the distribution of goods and services.

- The objective of a centrally planned economy is often to promote social welfare and achieve specific economic goals.

Understanding Centrally Planned Economies

In a centrally planned economy, the government or a centralized power oversees the allocation of resources, including determining what types of goods and services to produce, how much of them to produce, and the price at which they should be offered for sale. These decisions are made based on the country’s needs and goals rather than on individual profit motives or consumer preferences.

- Resource Allocation In a command economy, the government has control over all resources. It makes decisions regarding the allocation of these resources with the aim of achieving specific social and economic goals.

- Planning Government planning is the hallmark of a centrally planned economy. All economic activity, including production, investment, and distribution, is laid out in a comprehensive plan.

- Production and Pricing The government determines the nature, quantity, and price of goods and services produced in the economy. It also decides on where to direct investments and where to deploy resources.

- Role of the Market Unlike market economies, where prices are set by supply and demand, prices in centrally planned economies are determined by the government. In such economies, market forces have minimal influence.

- Ownership In a centrally planned economy, the means of production – land, labor, physical capital, and enterprise – are commonly owned by the state.

- Social Welfare Theoretically, the main goal of a centrally planned economy is to cater to the collective needs and ensure equal distribution of resources among the population, hence achieving social welfare.

Understanding these features helps us to grasp the dynamics of centrally planned economies, laying the groundwork for an in-depth exploration of their advantages and challenges.

Comparisons with Other Economic Systems

Centrally planned economies stand in stark contrast to other types of economic systems, particularly free market economies and mixed economies.

- Centrally Planned Economy vs. Free Market Economy A free market economy, also known as a capitalist economy, is one where decisions regarding investment, production, and distribution are guided by the price signals created by the forces of supply and demand. The key distinction between a free market and a centrally planned economy lies in who makes the decisions—individuals and firms in a free market, or the government.

- Centrally Planned Economy vs. Mixed Economy A mixed economy blends elements of free market and centrally planned economies. It allows for private sector enterprise and profit motive, but with government regulation to promote welfare and curb negative externalities. A mixed economy attempts to harness the advantages of both free market and central planning to generate high levels of output and equality.

- Centrally Planned Economy vs. Command Economy While both types involve significant government control over economic activity, the term “command economy” often implies an authoritarian regime and lack of individual freedoms. In contrast, “centrally planned economy” can be seen as a more neutral term, focusing on the economic structure rather than the political context.

- Centrally Planned Economy vs. Traditional Economy Traditional economies are driven by customs, traditions, and beliefs of the community. Here, the what, how, and for whom to produce are often based on ritual, habit, or custom. These economies are often rural and farm-based. Comparatively, centrally planned economies are generally found in more industrialized nations with higher levels of development and are driven by government plans rather than customs or habits.

By comparing centrally planned economies with other economic systems, we can better understand their unique characteristics, strengths, and weaknesses.

Pros and Cons of a Centrally Planned Economy

A centrally planned economy, like any other economic system, comes with its own set of advantages and disadvantages. Its effectiveness can depend greatly on the context and implementation.

Pros

- Equality and Social Welfare Since the government controls the production and distribution of goods and services, it can theoretically ensure a more equitable distribution of wealth and resources, minimizing socioeconomic disparities.

- Control over the Economy The government can control the factors of production and can lead the economy in a specific direction to fulfill societal goals, such as industrialization or self-sufficiency.

- Planning for the Long-Term A centrally planned economy allows for long-term strategic planning as the state can direct resources towards industries and areas that align with long-term goals and objectives.

- Control over Wastage The system aims to eliminate waste and inefficiencies by directing resources only to areas where they are most needed, as per the state’s calculations.

Cons

- Lack of Efficiency Central planning can often lead to inefficiencies due to a lack of market competition. Without the profit incentive provided by market competition, industries may not have a reason to innovate or improve their products and services.

- Inadequate Information It’s challenging for a central authority to gather all the necessary information about consumers’ preferences, leading to potential mismatches between supply and demand.

- Lack of Consumer Choice In a centrally planned economy, consumers often face a lack of variety and quality in goods and services since the state controls production.

- Risk of Corruption The concentration of economic power in the hands of the state can potentially lead to misuse of resources and corruption.

While the concept of a centrally planned economy might seem appealing in theory, it has proved challenging to implement effectively in practice. Nonetheless, it continues to be an important model to study, and some elements of central planning are present in various forms in many economies worldwide.

Transition from a Centrally Planned Economy to a Market Economy

Transitioning from a centrally planned economy to a market economy is a complex and challenging process that requires significant structural adjustments. This section will delve into the steps typically involved in this transition and highlight some of the challenges encountered.

- Liberalization The first step usually involves liberalizing economic activity. This can mean reducing state controls on prices and trade, allowing private businesses to operate, and encouraging competition. This stage can cause immediate economic shocks as prices may increase and previously protected sectors may face new challenges.

- Privatization The government begins to transfer state-owned enterprises to private ownership. This process can be fraught with difficulties, as determining a fair value for these entities can be challenging, and there may be resistance from workers or others with vested interests.

- Institution Building A successful market economy requires institutions that can support it. These can include everything from a legal system that can enforce contracts to a regulatory system that can manage competition. Building these from scratch is a complex task that requires significant resources and expertise.

- Reforming the Financial Sector Central planning often leaves a country without the financial institutions necessary for a market economy, such as commercial banks and stock exchanges. Developing these can take time and requires careful regulation to avoid instability.

- Managing the Social Impact The transition can have profound social impacts, such as unemployment, wealth inequality, and social unrest. Managing these impacts is crucial to maintaining social stability and ensuring the benefits of the transition are distributed fairly.

Historical examples of this transition process include former Soviet Bloc countries, China, and Vietnam. Each has followed a different path with varying levels of success, providing valuable lessons for other nations considering similar reforms.

Examples of Centrally Planned Economies

This section highlights real-world instances of centrally planned economies, providing an insight into their implementation, successes, challenges, and evolution over time.

- Soviet Union The Soviet Union is one of the most notable examples. The government owned and managed all industry and services, with economic decisions made by central planners. Although this allowed for significant industrial growth, it also resulted in economic inefficiencies and shortages of consumer goods.

- People’s Republic of China China operated as a planned economy for many years after the founding of the People’s Republic in 1949. Over the decades, however, it has gradually introduced more market-oriented reforms while retaining elements of central planning. This mixed system has led to substantial economic growth, though it also presents its own unique challenges.

- Cuba Cuba has operated under a planned economy since the 1959 revolution. The government controls most of the economy, with central plans used to allocate resources and dictate production. More recently, however, there has been a gradual shift towards market economics, with the private sector growing in importance.

- North Korea North Korea remains one of the few countries to still operate a purely planned economy, with all industry owned by the state and economic output planned and managed by the government.

These examples demonstrate the diverse forms and outcomes of centrally planned economies in practice. They provide valuable case studies for understanding the complexities and potential consequences of central economic planning.

FAQs

A centrally planned economy is an economic system where the government has significant control over the allocation of resources, production decisions, and distribution of goods and services.

In a centrally planned economy, the government determines production targets, sets prices, and decides on the allocation of resources. State-owned enterprises often play a central role, and economic activities are directed by government planning agencies.

Advocates argue that a centrally planned economy can promote equity, reduce income inequality, and prioritize public welfare over individual profit. It allows the government to direct resources toward important sectors and plan for long-term economic goals.

Critics argue that centrally planned economies can suffer from inefficiencies due to the lack of market competition and the absence of price signals. The system can lead to reduced innovation, limited consumer choice, and potential inefficiencies in resource allocation.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Business Ethics - Business ethics refers to the moral principles and values that guide the behavior and decision-making of individuals and organizations in…

Business Ethics - Business ethics refers to the moral principles and values that guide the behavior and decision-making of individuals and organizations in…  Microeconomics Definition - Microeconomics is a study within economics that looks specifically at the behavior of individuals and firms. When considering limited resources,…

Microeconomics Definition - Microeconomics is a study within economics that looks specifically at the behavior of individuals and firms. When considering limited resources,…  Intangible Assets: Definition, Types & Example - An intangible asset is not physical in presence. It cannot be seen or touched.

Intangible Assets: Definition, Types & Example - An intangible asset is not physical in presence. It cannot be seen or touched.