Elastic Demand: Definition, Formula & Examples

What is Elastic Demand?

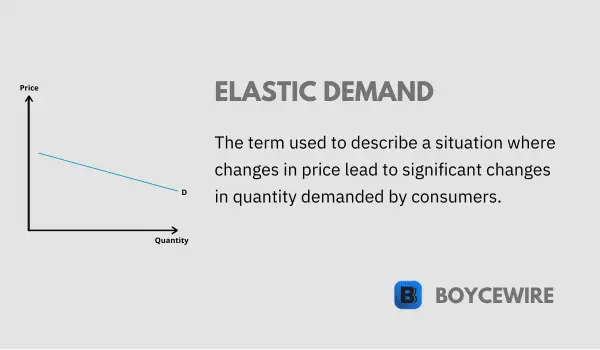

Elastic demand is a fundamental concept in economics that helps businesses, policymakers, and consumers understand how changes in the price of a good or service impact the quantity demanded. When demand is elastic, a change in price leads to a proportionately larger change in the quantity demanded, meaning that consumers are highly responsive to price fluctuations. This responsiveness to price changes can significantly impact a company’s revenue, marketing strategies, and government policies.

Understanding the concept of elastic demand and its implications is crucial for making informed decisions in various economic contexts. In this article, we will explore the determinants of elasticity, its relation to revenue and consumer behavior, the role it plays in government policy, and how to calculate price elasticity of demand. We will also examine real-world examples of elastic demand and discuss the limitations and criticisms of this economic concept.

Key Points

- Elastic demand refers to a situation where a change in price leads to a relatively larger change in quantity demanded.

- When demand is elastic, consumers are highly responsive to price changes, meaning that a small increase in price results in a significant decrease in quantity demanded, and vice versa.

- Elastic demand is typically observed for non-essential goods, luxury items, and products with readily available substitutes.

Characteristics of Elastic Demand

- Price Sensitivity: One of the most prominent characteristics of elastic demand is that consumers are highly sensitive to price changes. When the price of a good or service increases, consumers tend to reduce their consumption significantly, while a decrease in price often leads to a substantial increase in consumption.

- Availability of Substitutes: Elastic demand is typically associated with goods and services that have many close substitutes. The more alternatives available to consumers, the easier it is for them to switch to a different product if the price of their preferred good changes.

- Non-essential Goods: Goods and services considered non-essential or luxury items tend to have elastic demand. Since these items are not necessary for daily life, consumers can more easily adjust their consumption in response to price changes.

- Time Horizon: Elasticity can also depend on the time frame being considered. In the short run, demand may be relatively inelastic because consumers cannot immediately adjust their consumption habits. However, in the long run, demand may become more elastic as consumers have more time to explore alternatives and adjust their preferences.

- Proportion of Income Spent: Products that account for a small portion of a consumer’s income are more likely to have elastic demand. When the price of such goods changes, it has a relatively minor impact on a consumer’s overall budget, making it easier for them to adjust their consumption.

- Brand Loyalty: When consumers have strong brand loyalty, the demand for a specific product may be less elastic. In such cases, consumers are less likely to switch to a substitute good in response to price changes. However, if brand loyalty is weak, demand is more likely to be elastic as consumers will readily switch to alternative products.

Understanding these characteristics can help businesses, policymakers, and consumers make more informed decisions about pricing strategies, marketing efforts, and government policies.

Calculating Elastic Demand

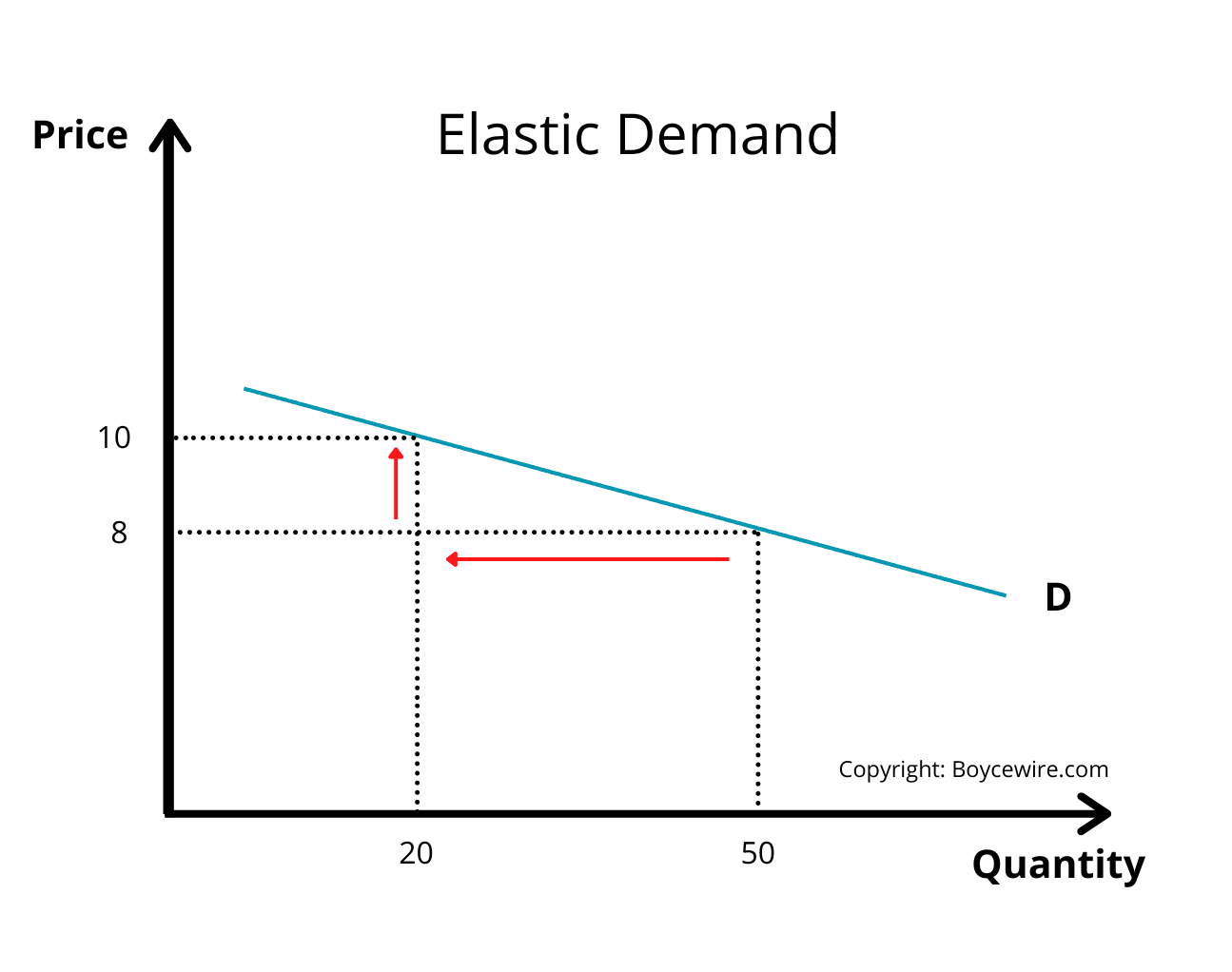

The price elasticity of demand (PED) is the measure used to determine how sensitive the demand for a good or service is to a change in its price. To calculate the price elasticity of demand, you can use the following formula:

Price Elasticity of Demand (PED) = (% Change in Quantity Demanded) / (% Change in Price)

Let’s break down the steps to calculate the PED:

- Determine the initial price (P1) and quantity demanded (Q1) of the good or service.

- Determine the new price (P2) and the new quantity demanded (Q2) after the price change.

- Calculate the percentage change in price: (% Change in Price) = [(P2 – P1) / P1] x 100

- Calculate the percentage change in quantity demanded: (% Change in Quantity Demanded) = [(Q2 – Q1) / Q1] x 100

- Divide the percentage change in quantity demanded by the percentage change in price to obtain the price elasticity of demand.

After calculating the PED, the result can be interpreted as follows:

- If PED > 1, the demand is elastic. This means that the percentage change in quantity demanded is greater than the percentage change in price, and consumers are sensitive to price changes.

- If PED < 1, the demand is inelastic. This indicates that the percentage change in quantity demanded is less than the percentage change in price, and consumers are less sensitive to price changes.

- If PED = 1, the demand is unit elastic. In this case, the percentage change in quantity demanded is equal to the percentage change in price.

By calculating and understanding the price elasticity of demand, businesses can make better decisions about pricing, production, and marketing strategies to maximize revenues and minimize costs. Similarly, policymakers can use this information to design more effective tax and subsidy policies that consider the responsiveness of consumers to price changes.

Examples of Elastic Demand

Elastic demand occurs when a change in price leads to a proportionally greater change in the quantity demanded

High-end items like sports cars and designer handbags typically have elastic demand. When the price of these goods increases, the quantity demanded decreases significantly, as consumers can easily substitute these products with more affordable alternatives or simply choose to forgo the purchase.

The demand for airline tickets is often elastic, especially for leisure travel. A significant increase in ticket prices may lead consumers to opt for alternative transportation methods, such as driving or taking the train, or to postpone or cancel their trips altogether.

Products with strong brand loyalty, such as smartphones, can also exhibit elastic demand. For instance, if the price of a popular smartphone brand increases substantially, consumers might switch to a more affordable alternative with similar features and performance.

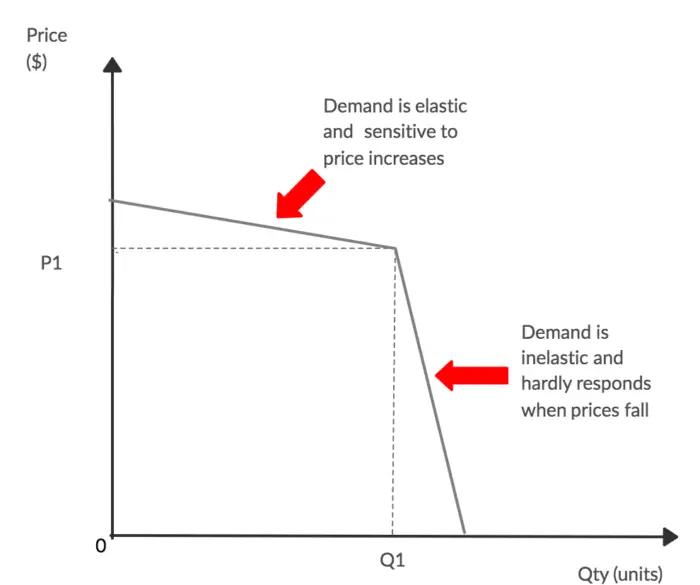

Goods and services that are not considered necessities tend to have elastic demand. For example, if the price of movie tickets or dining out at a restaurant increases, consumers might choose to stay home and cook a meal or watch a movie on a streaming platform, resulting in a significant drop in demand. The elastic demand curve represents the scenario in which a small change in the price of a product leads to a significant change in the quantity demanded. This type of demand curve is highly responsive to price changes and is typically associated with goods and services that have numerous substitutes or are not essential. The elastic demand curve is relatively flat, indicating that quantity demanded changes significantly more than the price. In other words, the percentage change in quantity demanded is greater than the percentage change in price, leading to an elasticity of demand greater than one. The elasticity of demand can be calculated using the following formula: Elasticity of Demand = % Change in Quantity Demanded / % Change in Price In terms of graphical representation, an elastic demand curve appears flatter or more horizontal compared to an inelastic demand curve, which is steeper or more vertical. The flatter curve signifies that consumers are more price sensitive. Products with elastic demand tend to be luxury goods, non-essential items, or goods with many substitutes. For example, a small price increase in a luxury chocolate brand may result in consumers switching to a less expensive brand, indicating a high price elasticity of demand. Understanding the concept of the elastic demand curve is crucial for businesses and policymakers alike. It helps businesses set their pricing strategies to maximize revenue, and it aids policymakers in understanding how tax changes can affect consumer behavior and the economy as a whole. Elastic demand refers to a situation where a change in price results in a relatively larger change in quantity demanded. Elastic demand is characterized by a high responsiveness of quantity demanded to price changes, while inelastic demand indicates a less sensitive response to price changes. Factors that contribute to elastic demand include the availability of substitutes, the proportion of income spent on the product, and the time available for consumers to adjust their consumption patterns. Non-essential goods, luxury items, and products with readily available substitutes often display elastic demand.

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.1. Luxury Goods

2. Airline Tickets

3. Brand-specific Goods

4. Non-essential goods and services

Elastic Demand Curve

FAQs

About Paul

Further Reading

Animal Spirits - Animal spirits refers to the emotional and psychological factors that drive human behavior in economic decision-making, including confidence, optimism, and…

Animal Spirits - Animal spirits refers to the emotional and psychological factors that drive human behavior in economic decision-making, including confidence, optimism, and…  Oligopoly: Definition, Characteristics & Examples - Oligopoly is derived from the Latin ‘olígoi’ – meaning “few”, and ‘pōléō’ – meaning “to sell”. So loosely translated, it…

Oligopoly: Definition, Characteristics & Examples - Oligopoly is derived from the Latin ‘olígoi’ – meaning “few”, and ‘pōléō’ – meaning “to sell”. So loosely translated, it…  Effect Size - Table of Contents What is Effect Size? Understanding Effect Size Types How to Calculate Interpreting Applications Limitations Examples FAQs Effect…

Effect Size - Table of Contents What is Effect Size? Understanding Effect Size Types How to Calculate Interpreting Applications Limitations Examples FAQs Effect…