Inelastic Demand: Definition & Examples

What is Inelastic Demand

In economics, inelastic demand is where the demand for a product is largely unresponsive to changes in price. In other words, the demand for the product is so strong that consumers are willing to pay almost whatever the price.

For example, the price of a Ferrari is unlikely to affect demand. Whether it costs $200k or $250k, the drop in demand is likely to be small. The reason is that demand for such premium products it relatively inelastic. The type of consumer buying these products tend to have substantial wealth in the first place. So a higher price won’t be that detrimental.

This is in contrast to when goods are elastic, whereby changes to price dramatically change demand and consumer behaviour. For example, if the price of a bag of chips increases by 10 percent, consumers may move to substitute goods such as popcorn, pretzels, or other snacks.

Key Points

- Inelastic demand is where the demand for a good remains relatively unchanged in response to changes in price.

- Goods where there are no substitutes make for inelastic demand as customers have no alternatives.

- A good is deemed inelastic if its Price Elasticity of Demand (PED) is less than 1.

- The PED can be calculated using the formula PED = percentage change in quantity demanded / percentage change in price.

How Inelastic Demand Works

Inelastic demand shows the relationship between price and demand. More specifically, it shows where the demand of a good fails to react in an ordinary way. Usually, higher prices lead to fewer people demanding those goods. However, in this case, higher prices lead to decline in demand which is unsubstantial. For small price increases, it may not even affect demand at all.

This might not run true following the standard economy theory of supply and demand. However, this can occur for a number of reasons, although most notably is the absence of a substitute good. If we look at goods such as gas or water utilities, there is no alternative. If you want gas, you have to pay the going rate or you can’t drive. For people that work out of town, thats pretty much a non-starter.

We can take another example. If we look at life saving drugs that treat cancer, we are looking at a non-negotiable good. Consumers that need this will pay almost whatever it takes. There is no alternative for them, and the benefit is to save their life. So whilst this is an extreme example, it demonstrates how the lack of alternatives can create an overwhelming demand for a certain good.

In contrast, when the demand for a product is elastic, a change in price results in a relatively large change in the quantity demanded of the product. This is because consumers have a choice of substitutes, and they can switch to a substitute product if the price of the original product becomes too expensive.

For example, if the price of some baked good increases, consumers have many other alternatives that are cheaper. In turn, the demand for the more expensive baked goods decreases significantly, suggesting the demand is elastic.

The concept of demand elasticity is crucially important. For businesses that have inelastic demand, they are able to set prices with little fear of lost sales. Yet for businesses where demand is elastic, consumers are more sensitive to changes in price. So any changes to the pricing strategy must seriously be considered.

Inelastic Demand Curve

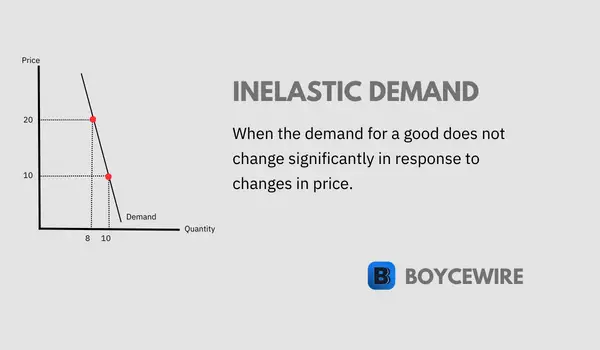

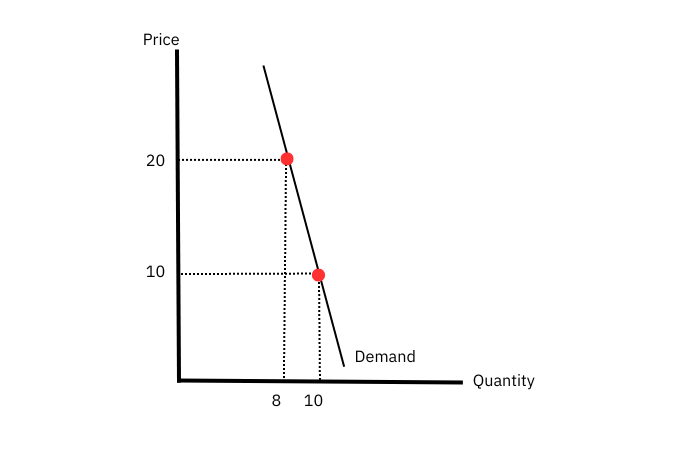

The inelastic demand curve demonstrates the relationship between price and demand. One helpful way of remembering this over elastic demand is to think of it as an ‘i’. The curve is relatively vertical, so it slightly resembles the letter.

As we can see from the curve above, it’s a steep upward line. This shows that changes in price have a minor effect on the quantity of demand of the product. In other words, when the price changes, demand remains relatively stable.

The graph is typically drawn with price along the y-axis and quantity along the x-axis. It is typically steep – representing a large change in price, but a small change in quantity.

This is in contrast to an elastic demand curve which is more or less horizontal. In other words, a small shift in price will dramatically change consumer behavior and demand. This is because goods that are elastic tend to have a wider variety of choice. In turn, they have greater negotiating power and can therefore put a downward pressure of prices. If businesses increase prices, they run the risk of losing customers.

Inelastic demand is not only limited to goods, but also various services and industries. It can come in different degrees. For example, the curve is steeper for certain goods such as insulin where people need it to live.

By contrast, there are inelastic goods which are slightly more sensitive such as sports cars. There are many consumers that would love to buy a Ferrari and would be willing to pay a high price. However, there comes a point where demand starts to fall as there are other manufacturers such as Lamborghini. So although demand is inelastic, it is not the same as goods like insulin.

How to Calculate Inelastic Demand

We can calculate inelastic demand by using the price elasticity of demand (PED) formula. This measures how responsive demand is in relation to changes in price.

The PED formula is:

PED = percentage change in quantity demanded / percentage change in price

When the PED is less than 1, demand is inelastic. This means that a 1% increase in price would lead to a less than 1% decrease in demand. In other words, the effect is not reflected between price and demand.

For example, if the price of a good increases by 5 percent, but demand only decreases by 1 percent, we can calculate the PED below:

PED = -1% / 5% = -0.2

So as the PED is less than 1, we can conclude that the demand for this good is inelastic.

One important thing to note about the PED is that it can vary at certain times. For instance, demand may become more inelastic during the Christmas period when consumers are looking for gifts.

Characteristics of Inelastic Demand

Here are some common characteristics of inelastic demand:

- Necessity: when goods are necessary, consumers have little choice but to buy them. For example, gas is a necessity to be able to run a car. Without it, consumers wouldn’t be able to drive to work. So often, there is little choice.

- Lack of substitutes: When there are few substitute goods, there are fewer alternatives for consumers. This lack of choice gives the sellers greater power to set prices and therefore create demand which is inelastic. With fewer goods to choose from, consumers will find it difficult to find an alternative if prices go up.

- Price sensitivity: Inelastic demand is characterized by low price sensitivity, meaning that changes in price have little effect on consumer demand. Even if the price of the product or service increases, consumers will still continue to purchase it.

- Income: When a good represents a high percent of a consumers wage, they are likely to be more sensitive to price changes. For example, those in the top 1 percent are unlikely to be bothered if the price of a meal goes up by 100 percent. Yet for the middle-class, this may stop them going out.

- Time: Over time, consumers may be able to adjust their behavior to account for price changes. For example, consumers may be out in town, but find drinks expensive. In the moment, they have little choice but to pay. However, next time, they may decide to bring their own drinks from home. Over time, they are able to adjust and find substitutes or cheaper alternatives.

Inelastic Demand Examples

Gasoline

Gasoline or petrol as it is known in Europe, is a virtual necessity to many across the world. Consumers need it to travel to work, leisure, or meet family and friends. Whilst there are alternatives such as the bus and train, it is can be very inconvenient for those who live outside the city. So gas is somewhat of a necessity to some, with fewer alternatives.

College textbooks

School textbooks are often a necessity for students. They may require them for study materials to help achieve their required grade. At the same time, there are few substitutes, with their education provider often providing specific books or ‘reading materials’. This presents students with little choice but to buy the specified books in order to assist with their studies.

Airline tickets

When looking at airline tickets, there are many locations whereby there is only one available airline. Even for those destinations that have some choice, there are few carriers to choose from – especially for longer-haul flights. This shortage of substitutes help contribute to inelastic demand. On top of this, there are time constraints. For example, a businessman might need a flight the next day. But if there is only one available ticket, he may have to pay whatever it costs.

Concert tickets

With concert tickets, they are often sold out. Sometimes within minutes. This naturally creates an artificial inflation due to the competitive nature to secure a ticket. Naturally, there are also no substitutes. If your favourite band are in town for one night only, there are no alternatives. So it’s either you pay or you miss out. For those fans, this increases their willingness to pay due to the scarcity. In turn, demand is inelastic due to the lack of substitutes, high level of scarcity, and due to consumer behaviour (i.e. favourite band).

Medication

For medical drugs, they are often life-saving and therefore necessary. There are many types where there is only one supplier. So not only is the good a necessity, but there are often no substitutes either. This makes it a common example of inelastic demand as it meets almost every criteria.

For example, those with diabetes need insulin to keep their blood sugar in check. Without it, there can be serious complications. So it is a complete necessary for day-to-day function of many. Therefore, the willingness to pay is extremely high as there are no alternatives. The only alternative is not to buy, but that comes at the cost of serious health implications.

Inelastic Demand vs Elastic Demand

The main different between inelastic demand and elastic is how demand changes in relation to price. Inelastic demand is where demand is relatively unresponsive to changes to price. In other words, the price can increase, but demand will stay strong.

By comparison, elastic demand is where demand is very responsive to changes in demand. In other words, a small change in the price can bring demand for a good dramatically down. Examples include vacations, luxury items, fast food, and clothing.

In terms of the types of goods – goods which have inelastic demand have four main characteristics. They tend to be necessities, have few substitutes, represent a small proportion of income, and have time constraints. This compares with elastic demand which has many substitutes, represents a high proportion of income, and is not a necessity.

Now the main difference between the two can be identified by measuring the price elasticity of demand (PED). If this value is greater than 1, then the demand is elastic. If it is less than 1, then the demand is inelastic.

FAQs

Factors that can influence inelastic demand include the availability of substitutes, the degree of necessity or addictiveness of the product, the time frame being considered, and the degree of brand loyalty or differentiation.

Inelastic demand can be a problem for consumers because it means that prices can increase without a corresponding decrease in demand. This can lead to higher prices and reduced affordability, especially for necessary goods or services.

Yes, inelastic demand can provide benefits to producers and suppliers by allowing them to maintain stable pricing and revenue even in the face of external factors such as changes in production costs or economic fluctuations.

Examples of goods with inelastic demand include necessities such as food, water, and medical supplies, addictive products like tobacco and alcohol, and highly differentiated luxury goods such as designer clothing and high-end electronics.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Variable Cost: Definition, Formula & Examples - We can define a variable cost as a cost that changes based on the output of the business.

Variable Cost: Definition, Formula & Examples - We can define a variable cost as a cost that changes based on the output of the business.  BATNA - BATNA, or Best Alternative to a Negotiated Agreement, is the alternative course of action that a party will pursue if…

BATNA - BATNA, or Best Alternative to a Negotiated Agreement, is the alternative course of action that a party will pursue if…  Economic Profit Definition - Economic profit is a firms total revenue minus its total costs, including implicit and explicit costs.

Economic Profit Definition - Economic profit is a firms total revenue minus its total costs, including implicit and explicit costs.