Phillips Curve: Definition, Short-run, Long-run & Example

What is the Phillips Curve?

The Phillips curve is a macroeconomic concept that represents the relationship between inflation and unemployment in an economy. It is named after A.W. Phillips, who first observed the relationship in the 1950s.

The basic idea behind the Phillips curve is that when unemployment is high, there is less pressure on wages and prices, which leads to lower inflation. Conversely, when unemployment is low, there is more competition for workers, which leads to higher wages and prices, and therefore higher inflation.

The Phillips curve was initially seen as a useful tool for policymakers, as it suggested that they could use monetary and fiscal policies to trade-off between inflation and unemployment. However, in the 1970s, the relationship between inflation and unemployment became more complex, and the Phillips curve began to break down. This breakdown was largely due to the impact of supply-side shocks, such as changes in oil prices, which can affect both inflation and unemployment at the same time.

Today, while the Phillips curve remains a useful framework for understanding the relationship between inflation and unemployment, it is no longer seen as a precise tool for policymaking. Nonetheless, it is still widely studied and discussed by economists and policymakers alike.

Key Points

- The Phillips Curve is a graphical representation of the inverse relationship between unemployment and inflation.

- The curve suggests that when unemployment is low, inflation tends to be high, and when unemployment is high, inflation tends to be low.

- The Phillips Curve is based on the observation that there is a trade-off between unemployment and inflation. When the economy is at full employment, there is upward pressure on wages and prices, which can lead to inflation.

- The Phillips Curve can be useful for policymakers in setting monetary policy, but it is not a perfect guide. There are many other factors that can affect inflation and unemployment, such as productivity growth, changes in oil prices, and shifts in aggregate demand.

History of the Phillips Curve

The Phillips curve is a macroeconomic concept that describes the inverse relationship between inflation and unemployment in an economy. It is named after A.W. Phillips, a New Zealand economist who first observed the relationship in a study of wage and price movements in the UK in the 1950s.

Phillips found that there was a consistent negative correlation between unemployment and wage inflation in the UK, with periods of low unemployment associated with higher wage growth, and vice versa. This led him to propose the idea that there was a trade-off between inflation and unemployment, which became known as the Phillips curve.

The Phillips curve gained widespread attention among economists and policymakers in the 1960s, as it suggested that governments could use monetary and fiscal policies to target either low unemployment or low inflation, but not both simultaneously. This idea was known as the “Phillips curve trade-off,” and it influenced economic policy in many countries during this period.

However, in the 1970s, the Phillips curve began to break down, as the relationship between inflation and unemployment became more complex. This was largely due to the impact of supply-side shocks, such as the OPEC oil crisis, which caused both inflation and unemployment to rise at the same time. As a result, many economists began to question the validity of the Phillips curve as a precise tool for policymaking. However, it remains a useful framework for understanding the relationship between inflation and unemployment, and has been the subject of extensive research and debate among economists ever since.

Overall, the history of the Phillips curve is a story of how a simple observation about wage and price movements in the UK led to a powerful idea that shaped economic policy for decades, before being challenged by changing economic conditions and evolving economic theory.

Phillips Curve Long-Run

In the long-run, the Phillips curve suggests that there is no trade-off between inflation and unemployment. This is because in the long-run, the economy will adjust to changes in inflation or unemployment, and the Phillips curve will shift accordingly.

In the long-run, wages and prices are flexible, and can adjust to changes in demand and supply. This means that if unemployment is too low, and there is upward pressure on wages and prices, businesses may eventually respond by increasing production and hiring more workers. This can lead to an increase in the supply of goods and services, and a decrease in the upward pressure on wages and prices.

Similarly, if inflation is too high, consumers may eventually adjust their expectations, leading to a decrease in demand for goods and services. This can lead to a decrease in the upward pressure on prices, and a decrease in inflation.

As a result, in the long-run, the Phillips curve is not a stable relationship, and can shift over time as the economy adjusts. For example, a supply-side shock, such as a change in technology or a natural disaster, could cause the Phillips curve to shift, making it more difficult to maintain low unemployment without generating inflation.

Overall, while the Phillips curve may be a useful framework for understanding the relationship between inflation and unemployment in the short-run, it is important to keep in mind that it is not a precise tool for policymaking, particularly in the long-run. Policymakers need to take into account a range of other factors, such as productivity growth, trade, and fiscal policy, when making decisions about how to manage inflation and unemployment in the long-run.

Short-Run Phillips Curve

The short-run Phillips curve is a graphical representation of the inverse relationship between inflation and unemployment in the short-run. It suggests that when unemployment is low, inflation tends to be high, and when unemployment is high, inflation tends to be low.

The short-run Phillips curve is based on the idea that in the short-run, wages and prices are relatively inflexible, and cannot adjust quickly to changes in demand and supply. This means that if demand for goods and services increases, but there is not enough supply to meet that demand, prices will rise, leading to inflation.

Conversely, if there is a decrease in demand for goods and services, but the supply remains the same, prices may fall, leading to deflation. In either case, changes in the level of unemployment can affect the balance of supply and demand, and therefore the level of inflation.

The short-run Phillips curve can be useful for policymakers, as it suggests that there may be a trade-off between inflation and unemployment in the short-run. For example, if the government wants to reduce unemployment, it may use expansionary monetary or fiscal policy to increase demand for goods and services, which could lead to a temporary increase in inflation.

However, it is important to note that the short-run Phillips curve is not a stable relationship, and can shift over time as the economy adjusts. For example, if consumers come to expect higher inflation in the future, they may demand higher wages and prices, leading to a shift in the Phillips curve.

Overall, while the short-run Phillips curve can provide useful insights into the relationship between inflation and unemployment in the short-run, it is important for policymakers to consider a range of other factors, such as productivity growth and structural changes in the economy, when making decisions about economic policy.

Phillips Curve and Stagflation

Stagflation is a term used to describe a situation where an economy experiences both high inflation and high unemployment simultaneously. Stagflation is often seen as a challenge for economic policymakers, as the Phillips curve suggests that high unemployment should be associated with low inflation, and vice versa.

During the 1970s, many advanced economies experienced stagflation, which challenged the traditional Phillips curve relationship. This was largely due to a combination of factors, including rising oil prices, declining productivity growth, and supply-side shocks.

The rise in oil prices during the 1970s led to higher costs for businesses, which they passed on to consumers in the form of higher prices. This created upward pressure on inflation, even as unemployment remained high. At the same time, declining productivity growth and supply-side shocks, such as the disruption to trade caused by the oil crisis, made it difficult for businesses to increase production and hire more workers, keeping unemployment high.

The persistence of stagflation challenged the traditional Phillips curve relationship, as it suggested that there could be high inflation and high unemployment at the same time. This led many economists to question the validity of the Phillips curve as a tool for policymaking, particularly in the long-run.

However, in more recent decades, the relationship between inflation and unemployment has become more stable, and the Phillips curve has regained some of its usefulness as a framework for understanding the short-run relationship between these variables.

Overall, stagflation represents a significant challenge for economic policymakers, and highlights the importance of considering a range of factors, such as productivity growth and supply-side shocks, when making decisions about economic policy. While the Phillips curve may be a useful tool in some circumstances, it is important to recognize its limitations and the potential for changes in economic conditions to affect its validity.

Phillips Curve Example

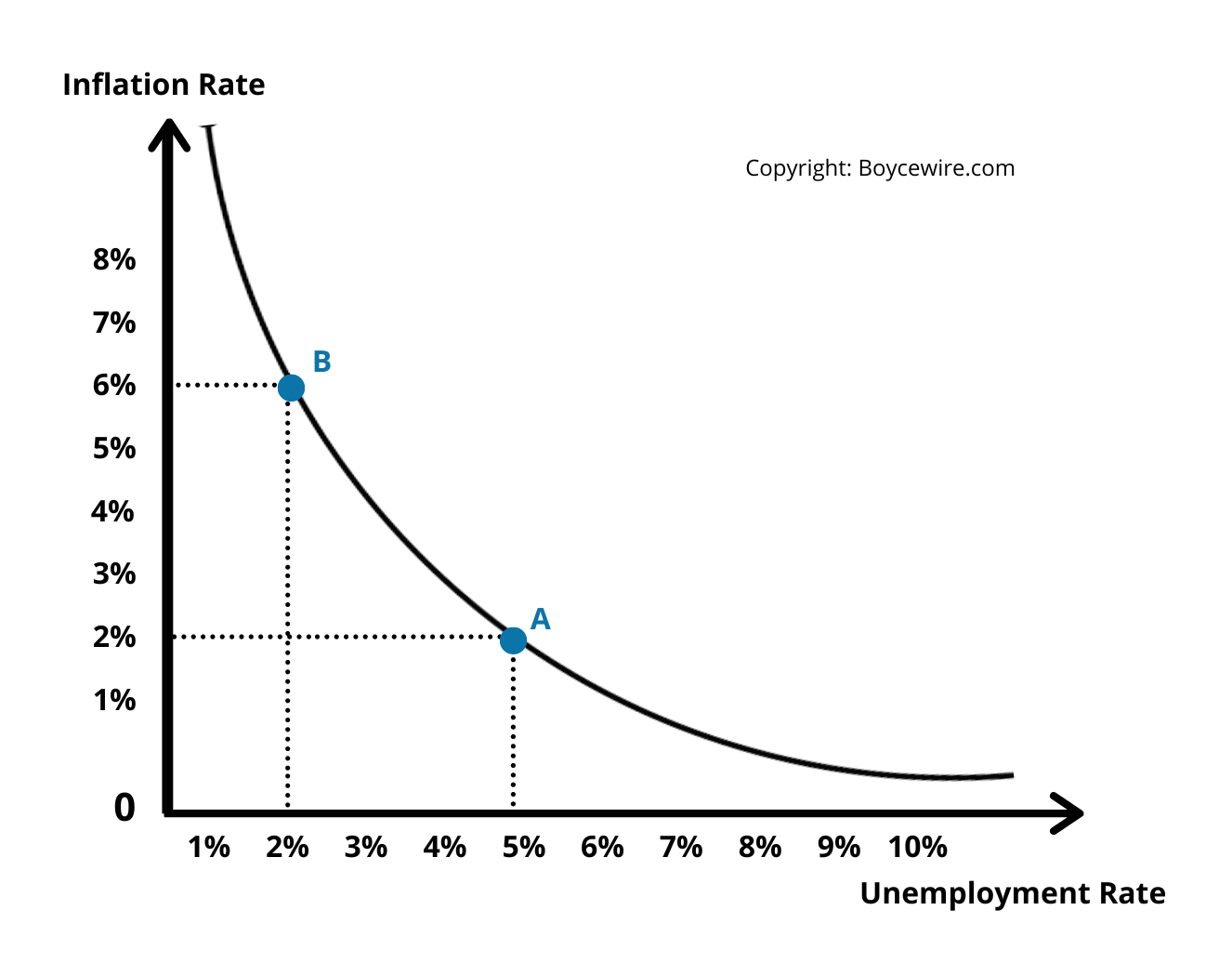

The Phillips Curve is a graphical representation of the inverse relationship between unemployment and inflation. As unemployment decreases, inflation tends to increase, and vice versa. Here is an example to illustrate this relationship:

Let’s say that the economy is currently experiencing high levels of unemployment, which means there are more people looking for work than there are available jobs. As a result, employers have little competition for workers, and wages remain low. At the same time, since there is less demand for goods and services due to the high unemployment rate, prices also remain low.

However, as the economy starts to recover and more people find jobs, the demand for labor increases, and employers have to compete for workers by offering higher wages. As wages increase, workers have more money to spend, and they increase their demand for goods and services, which pushes up prices. As prices increase, the rate of inflation also increases.

So, as unemployment decreases, inflation tends to increase, and this is represented by a downward-sloping Phillips Curve. Conversely, when unemployment increases, inflation tends to decrease, and this is represented by an upward-sloping Phillips Curve.

FAQs

A.W. Phillips was a New Zealand economist who first observed an inverse relationship between unemployment and wage inflation in the UK in the 1950s. His curve shows that as unemployment decreases, inflation tends to increase, and vice versa.

While the Phillips Curve was a popular framework for understanding the economy in the 1960s and 1970s, it has since been challenged by the stagflation of the 1970s and the lack of a clear relationship between inflation and unemployment in the 21st century. However, it is still sometimes used as a reference point for discussing macroeconomic policy.

The Phillips Curve suggests that there is a trade-off between unemployment and inflation. When unemployment is low, inflation tends to be high, and when unemployment is high, inflation tends to be low. This trade-off is not always exact, and there are many other factors that can affect inflation and unemployment, such as productivity growth, changes in oil prices, and shifts in aggregate demand.

The Phillips Curve can be a useful tool for central bankers in setting monetary policy, but it is not a perfect guide. Because of the many factors that affect inflation and unemployment, policymakers must also consider other indicators, such as interest rates, GDP growth, and financial market conditions.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Finance Charge - A finance charge is the fee or interest imposed by a lender on a borrower for the use of credit…

Finance Charge - A finance charge is the fee or interest imposed by a lender on a borrower for the use of credit…  Enron Scandal - The Enron scandal refers to a major corporate fraud involving the energy company Enron Corporation, characterized by deceptive accounting practices…

Enron Scandal - The Enron scandal refers to a major corporate fraud involving the energy company Enron Corporation, characterized by deceptive accounting practices…  Conspicuous Consumption: Definition & Examples - Conspicuous consumption is where the consumer spends excessive amounts in order to highlight their wealth to society.

Conspicuous Consumption: Definition & Examples - Conspicuous consumption is where the consumer spends excessive amounts in order to highlight their wealth to society.