Marginal Cost: How to Calculate, Formula & Examples

Marginal cost refers to the additional amount it costs to produce one extra good.

Marginal Cost: How to Calculate, Formula & Examples Read More »

Production theory looks at how businesses can most effectively combine labor and capital to achieve maximum efficiency. This can help firms increase output whilst also reducing output, thereby increasing profits.

Marginal cost refers to the additional amount it costs to produce one extra good.

Marginal Cost: How to Calculate, Formula & Examples Read More »

The factors of production are all the various elements that are required to come together to create a good.

Factors of Production: Definition, 4 Factors & Examples Read More »

The main difference between accounting and economic profit is that economic profit includes implicit costs. Whilst accounting profits include the raw costs of doing business, economic profit includes the opportunity cost of employing those resources for an alternative use.

An explicit cost is the clearly stated costs that a business incurs. For example, employee wages, inputs, utility bills, and rent, among others. These are the costs which are stated on the businesses balance sheet.

By contrast, implicit costs are those which occur, but are not seen. In other words, these are the costs that are not directly linked to an expenditure. For example, a factory may close down for the day in order for its machines to be serviced.

Explicit and Implicit Costs: Definition & Examples Read More »

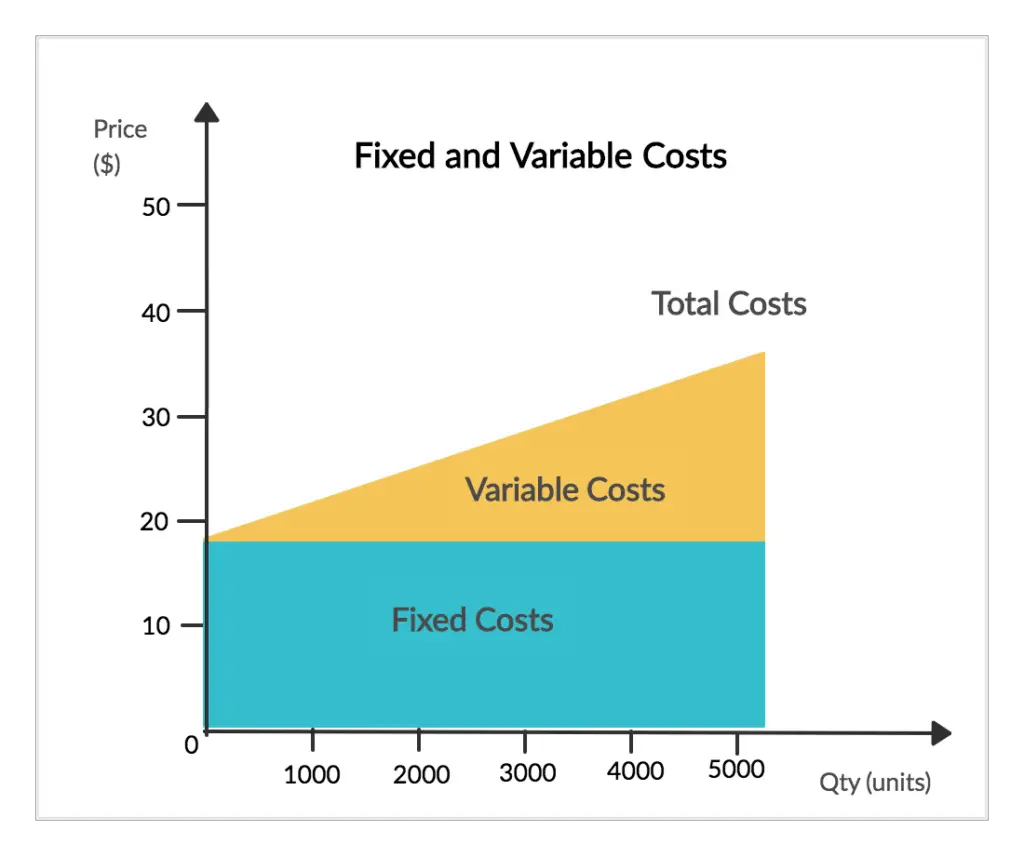

A fixed cost is a cost that a business must pay whether it produces one good or a million. Regardless of output, it must pay the same amount.