Intangible Assets: Definition, Types & Example

What is an Intangible Asset

An intangible asset is one by which has no physical presence. In other words, it cannot be seen or touched. For example, a firm’s brand name is an intangible asset. It has no physical presence, but is a valuable asset to the company.

A firm’s brand image is an important part of the company as it relays trust with the customer. When consumers buy from big brands such as Apple, they can trust the quality of the product. In fact, this is why Apple’s brand alone is said to be worth over $200 billion.

As intangible assets are non-physical, it can be extremely difficult to value them. For example, a patent is an intangible asset, yet its value is dependent on a number of factors. Among them include the firms cost of production. If the firm makes $10 million from the patent, then it could be concluded that it is worth that much.

However, there are a number of other variables at play. Among them are other intangible assets such as the firms brand image and reputation, the presence of franchises, software, and trade secrets. As such, this muddies the water as to how much of the profit is due to the patent, and how much is due to these other factors.

Key Points

- An intangible asset is a non-physical part of the business which has value in and of itself.

- Intangible assets can be difficult to value.

- Intangible assets are not financial instruments (such as accounts receivable).

It is important to note that an intangible asset is not a financial instrument. Although financial assets such as accounts receivable, stock certificates, or credit notes are all non-physical assets, they are financial instruments which have a clear and identifiable monetary value. An intangible asset is a non-physical asset which grants rights and privileges to the owners – such as trademarks or copyright.

Intangible Assets Explained

On occasion, firms market capitalization may vary dramatically from the value of its assets. For example, in 2020, Apple had tangible assets valued at over $320 billion, yet its market capitalization is close to $2 trillion. One of the main reasons for this is that intangible assets are not included on usual financial statements. This is because they do not have an identifiable value and useful lifespan.

For example, a machine may have a lifespan of 10 years, so can be amortized onto the firms balance sheet. However, the firm’s brand image has an unknown lifespan and its value is notoriously difficult to measure – largely due to the fact that there are a number of other intangible assets with unknown values.

With that said, there are some intangible assets which have a definite life-span. Examples include patents, copyrights, and franchise agreements. There is a set life-span by which the company can benefit, which can make its valuation straighter forward. Yet these ‘definite use’ assets are not accounted for on traditional financial statements because they do not have a clear and definable value.

Types of Intangible Assets

There are many types of intangible assets – most of which are unquantifiable. However, there are some intangible assets that have value and are on occasion traded. For example, broadcasting rights are an intangible asset. The value of which can be determined by the amount broadcasters pay for it. Yet the true value is likely to differ from this valuation.

If a broadcaster pays $1 billion for the rights to show the Super Bowl, it may bring in $1.1 billion in revenue through advertisements and subscribers. This would mean that the assets true value is in excess of the amount paid. At the same time, the firm may receive less – in which case, the firm would have to write off the difference.

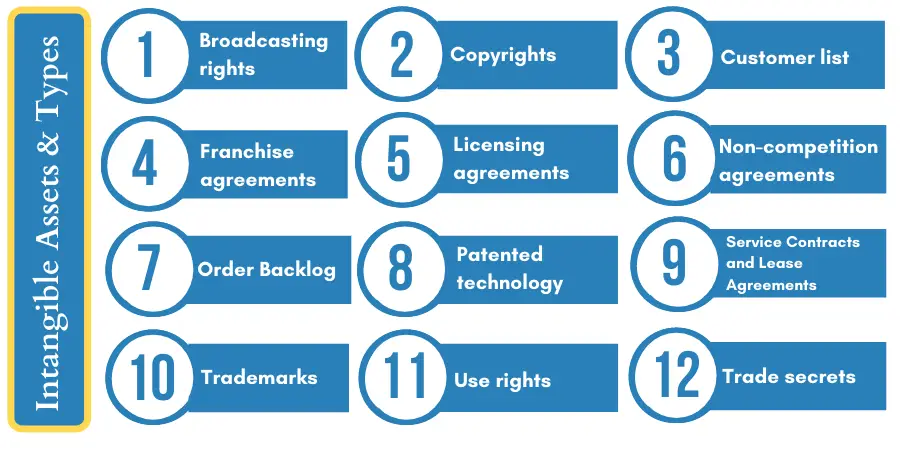

With that said, there are many types of intangible assets – such as:

1. Broadcasting rights

Broadcasting rights are largely employed in the sporting arena – particularly for pay per view events. Usually, the broadcaster will pay a fee to the event host for the right to broadcast. In turn, the firm will bring in additional revenues from advertisements, pay per view customers, and greater brand recognition.

2. Copyrights

Copyrights grant the owner the exclusive ownership of a piece of work. This is an intangible asset that provides legal protection to the owner and gives them the right to use and distribute their work. For example, certain plays may only be performed under a licensed copyright. Alternatively, there may be royalties due to the copyright owner for its use.

3. Customer list

Many firms build up a customer list over the years which can prove to be a crucial intangible asset. They may start with one customer, and build up many thousands over the years. This is particularly prevalent in the business-to-business sector where there are contracted relations between parties. In turn, this is a valuable asset as there is an established supplier/customer relation.

4. Franchise agreements

Franchise agreements can prove to be a successful way for businesses to expand exponentially. In fact, this type of intangible asset has helped McDonald’s expand right across the world. These agreements allow McDonald’s to obtain a fee in return for individual entrepreneurs using their brand and infrastructure.

5. Non-competition agreements

Non-competition agreements are legally binding contracts which stipulate that neither party can compete against each other. These are usually employed between employer and employee. It is designed to prevent the employee leaving with company knowledge and starting a competing firm, or, share this knowledge with another competitor.

These agreements can prove to be an extremely valuable intangible asset – particular in markets whereby the employee can take the firm’s clients with them. For example, these are common agreements within the legal profession.

6. Order Backlog

An order backlog is essentially a list of orders that the firm has, but has yet to be fulfilled. These are considered intangible assets as they present value to the firm, but have not been realized.

7. Patented technology

Patents are a type of intangible asset which allows the owner the legal right to use and produce an invention. This differs from a copyright in that a patent is on an invention rather than a physical product. For example, Apple has filed thousands of patents over the years, yet the firm hasn’t put them all into production. Instead, they are often used to prevent other firms from using that same invention.

8. Service Contracts and Lease Agreements

Service contracts can include those between businesses and their suppliers, or, it can be between a business and a customer. For example, a phone contract that ties the customer down for two years. These are treated as intangible assets as they allow for a smooth and guaranteed running of the firm. It can accurately anticipate how much revenue it brings in or spends as a result of these contracts, so can finance its operations more effectively.

9. Trademarks

Trademarks refer to a brands image and entity. For example, a trademark could cover the brands name, logo, slogan, or other branding item. This is treated as an intangible asset because it prevents other firms from using the brand to sell its goods. At the same time, it protects the brands image from other firms which may make ‘copy-cat’ products.

10. Use rights

Use rights including rights over drilling, water use, land use, and others which allow individuals and businesses exclusive rights. For example, many mining firms have exclusive rights to excavate a certain area. That way, the firm is able to fully benefit from an expensive project – something that would not be profitable with two or more firms. This is treated as an intangible asset because it prevents competition from exploiting those resources.

11. Trade secrets

Trade secrets include formulas and recipes that are key to a brands success. For example, Coca-Cola has a secret recipe that has made it a worldwide hit, but is said to be only known by a few people – with the recipe stored in a vault in Atlanta, USA. This type of intangible asset is invaluable to a firm like Coca-Cola which would come under severe competition if the recipe was released to the public. It could be argued that it is worth nearly as much as the firm itself.

Intangible Assets Example

It is important to understand that intangible assets are only included on the balance sheet if or when they are acquired by a third party. Only then does the intangible asset have a monetary value. For example, Company X may purchase a patented technology from Company Y for $1 million. This would then appear on the firms balance sheet as a long-term asset.

For intangible assets which have a definitive lifespan, such as patents, the asset is written off over the period of its lifespan via a process called amortization. Quite simply, if the patent cost $1 million and lasts 10 years – the cost would be amortized so that it cost $100k each year over 10 years. So instead of it being classed as a one-off cost, it is accounted for over 10 years.

By contrast, an intangible asset that has an indefinite life is valued on a yearly basis. For example, if Company X buys the trade secrets/recipe of Company Y for $10 million, its lifespan is unknown. Such an intangible asset is then assessed for impairment each year. If the deemed value falls beneath the initial cost, then this would be accounted.

FAQs

Examples of intangible assets include: Broadcast rights, Copyrights, Customer lists, Franchise agreements, Non-competition agreements, Order backlogs, Patented technology, Service Contracts and Lease Agreements, Trademarks, Use rights, and Trade secrets.

Intangible assets are characteristed in two main ways:

1) They are not physical goods.

2) They are not financial instruments.

The three major types of intangible assets are patents, copyrights, and the firms brand image.

Tangible assets are physical assets with a concrete, material presence, such as buildings, machinery, and inventory. Intangible assets, on the other hand, lack a physical form but still have value to the company due to their potential to generate future revenue or provide a competitive advantage.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Quantity Demanded - Quantity demand refers to the specific amount of a good or service that consumers are willing and able to purchase…

Quantity Demanded - Quantity demand refers to the specific amount of a good or service that consumers are willing and able to purchase…  Porter’s 5 Forces: Definition, Model & Example - Porters 5 forces is a method used to breakdown and understand the competitive nature of an industry or business.

Porter’s 5 Forces: Definition, Model & Example - Porters 5 forces is a method used to breakdown and understand the competitive nature of an industry or business.  Discount Rate in Economics - The discount rate is the interest rate by which the central bank charges commercial banks to borrow money or cover…

Discount Rate in Economics - The discount rate is the interest rate by which the central bank charges commercial banks to borrow money or cover…