Asymmetric Information: Definition, Causes & Examples

What is Asymmetric Information

Asymmetric information, or information asymmetry, is where one party in a transaction has more information than the other. In other words, the seller of a good may know more about its true worth than the consumer. As a result, the consumer pays more than the good is worth to them, had they known the full information.

The term ‘asymmetric’ refers to the absence of symmetry. This is where things are not equal. So with regards to an economic transaction, asymmetric information is where the buyer and seller have unequal information.

Key Points

- Asymmetric information is where one party in the economic transaction has more information than the other.

- Businesses are able to overcome asymmetric information by offering warranties, and providing a review system that reaffirms the quality of its goods.

- Asymmetric information is particularly prevalent in the second hand market, whereby the existing owner knows of any defects that might affect the price.

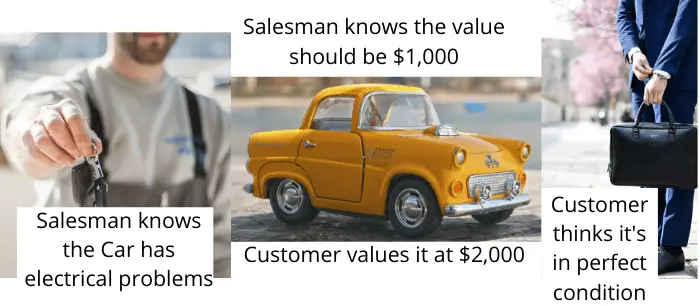

One of the classic examples used to demonstrate asymmetric information is the second-hand car salesman.

For instance, when selling the car, the salesman has full information on any defects it may have. This may include issues with steering, mileage, electrical problems, etc. However, the customer may be largely unaware of these problems, which, in turn, affects their valuation. As a result, the customer pays the full price for a faulty car, whilst the salesman makes off with a tidy sum.

Causes of Asymmetrical Information

Difficulty Obtaining Information (Absence of Information)

The main cause of asymmetrical information is the fact that we cannot have a full understanding of everything in the world. We may be able to understand specific parts, but not everything. For instance, we may be able to determine the best valued car based on its specification. Or, we may be able to determine that washing machines with certain features do not work well in closed off environments.

The point to be made is that customers do not always have a sufficient level of knowledge to make an informed purchasing decision. For example, the average consumer is unlikely to be well versed in the quality of new laptops.

To begin with, their knowledge on the best laptops may be non-existent. The only gauge is the price. They may purchase a new laptop for $300 without realizing the graphics are poor; something that was of great value to them.

The concept of a graphics GPU specification or the types of graphics cards such as an AMD Radeon VII is not common knowledge. Therefore, the customer either has to spend time acquiring the knowledge or base their decision on price or other mechanisms such as recommendations and reviews.

Inability to Obtain Information (Hidden Information)

When we say hidden information, we refer to the fact that, on occasion, the consumer is unable to obtain symmetrical information. For instance, a car salesman may know that the vehicle they are selling has been in two previous accidents. From the customer’s perspective, there is no way of finding out, particularly without great expense.

So in such a scenario, we have the seller withholding information that would devalue their goods.

We also have the example of insurance. Whilst they can obtain information such as age, location, sex, etc., they are unable to obtain how careful an individual is. Without the individual saying ‘Yes, I’m a reckless driver’, the insurance company is unable to obtain such information.

The insurance company may not know of any undisclosed medical conditions or whether the customer is more prone to lose their possessions. These are all pieces of information that the consumer has, but which the insurance company does not. One of the ways they counteract this is through a ‘no-claims’ bonus where the renewal charge declines the longer the customer does not make a claim.

Solutions to Asymmetric Information

The problem with asymmetric information is that either the consumer or the seller has a lack of information. What this means is that one side either over or underpays. Now the issue is that the other party is unable to obtain sufficient information to make an informed purchase. Sometimes this cannot be fully overcome, but there are potential solutions by which we are able to mitigate them.

1. Brand Image

A firm’s brand image is a key sign to customers that they can trust in what they are buying. For instance, McDonald’s is known across the world and its famous Big Mac is relatively consistent no matter where you go. Similarly, big brands such as Apple or Samsung are trusted to make high-quality phones. The brand name brings with it a signal to the consumer a reassurance of quality.

By contrast, ‘Big Mikes Phones’ does not have that same brand image. The information the average consumer has on ‘Big Mikes Phones’ will be virtually nil. Some may not even have heard of it before.

What we see are big brands that have a reputation for quality and reliability. In turn, they take great lengths to ensure that reputation remains unblemished. For instance, Cadburys spent 24 years trying to trademark their specific shade of purple.

Some other firms offer a money-back guarantee, free discounts, and other consumer benefits. The point is that it is in the interest of the business to keep consumers’ trust and belief that the company is reliable. Therefore the brand image by itself sends an informational signal to the rest of the market.

When a big brand such as Samsung produces defect phones, the company reacts in such a way to protect the brand image above its own profits. For instance, when its Galaxy Note 7 started catching fire due to a battery fault, Samsung called in the products back.

However, it also offered US consumers a $100 voucher if they exchanged it for another Samsung. In addition, they would also receive a $25 voucher if they went with a competitor.

2. Refunds and Return Policies

Under US Federal law, there is a three day ‘cooling off’ period on purchases over $25. That means consumers can get a refund if they change their mind. In addition, businesses are also legally obliged to provide a refund if the goods are faulty. So even if a warranty is not offered, a full refund is required.

However, the rules are different when the good has been opened and used. Most firms won’t offer a refund as it is unable to re-sell it. Therefore a consumer’s preference is generally insufficient to offer a refund.

With that said, there are some firms that employ a ‘try before you buy’ approach. Alternatively, some stores offer a complete refund if you don’t like the product. For instance, Udemy, a provider of online courses, offers a 30-day money-back guarantee if you do not like the course or find it useful. This overcomes asymmetric information in the fact that the customer doesn’t need to know anything about the product.

Bringing this all together, refunds and return policies help limit the potential costs associated with asymmetric information. For instance, a customer may purchase a refurbished laptop from a seller on eBay. However, upon delivery, it doesn’t switch on. Without a warranty or a refund policy, the consumer would be at a loss.

As there is a refund policy, the seller would be legally obliged to return the faulty good for a refund. Therefore even if the seller knows the product is faulty, they would have to provide a refund, thereby reducing the negative effect of asymmetric information.

3. Review Mechanisms

Most of the time we know almost nothing about the product we are buying, particularly with white goods such as fridges, washing machines, TV’s, etc. That puts the suppliers at a greater advantage as they have more knowledge than the average consumer.

For instance, Supplier A may realize the information asymmetry, cut costs, and make an inferior product. The average consumer may not know as they don’t make frequent purchases of white goods. So they may just assume that it’s the norm.

However, in today’s day and age, the feedback mechanism works quicker and more effectively than ever before. Reviews are readily available online and are seemingly available for almost anything.

This works two fold. First of all, it gives the consumer information quickly and easily. Thereby reducing the information deficit with the supplier. This allows the consumer to make a better informed decision based on any flaws in the product.

Second of all, it forces the supplier to ensure they are focusing on the consumer. Too many bad reviews and the brand becomes tarnished, which can significantly impact a business.

What we see is the degree of asymmetrical information reduces significantly, whilst also encouraging suppliers to make reliable products. Consumers become more aware of any pitfalls, and suppliers need to protect their brand image.

Asymmetric Information Examples

1. Doctors

Trained doctors undertake years and years of medical education. In turn, their knowledge over healthcare matters is naturally superior to the average patient.

Therefore, in an economic transaction, it is difficult for the consumer to contest the diagnosis. The prescribed treatment may cost $20k, but without having that medical knowledge, there is no way of plausibly disputing this.

Although the internet has allowed people to get a better understanding of their condition, there still exists a huge gap in understanding between the two parties.

2. Insurance

Insurance is a classic example of adverse selection which leads to asymmetrical information. When an insurer and a customer enter into an agreement, the customer has far more information on themselves than the insurer.

For instance, a health insurer has no idea of the customers habits. Do they smoke a packet of cigarettes a day, or do they eat enough fruit and vegetables? Such factors may make the transaction riskier to the insurer as it may lead to a greater risk of a serious illness.

The insurer may be able to overcome such asymmetrical information by hiring a doctor to do an examination for instance. This may allow it to obtain a greater deal of information of how healthy the customer is and price accordingly.

However, what we may see is a moral hazard. Even if the insurer is able to obtain information symmetry (have the same information as the customer), the customer may in fact become more reckless as a result of having insurance.

This may not necessarily be the case in health insurance, but is more prominent in the likes of gadget insurance. For example, someone who is insured may leave their laptop unattended whilst they go to the lavatory. This increases the risk of it being stolen; a risk than the customer knows they don’t have to bear.

3. Finance

One of the best examples of asymmetrical information was the circulation of toxic assets prior to the 2008 Financial Crisis. Banks that made sub-prime loans bundled them in with more secure loans and sold them on as financial securities.

What we saw was that the banks who sold the sub-prime loans packaged them up knowing there were toxic assets included. However, investors that purchased such bundled securities did not know of this significant risk.

The main indication they received was the AAA ratings that credit agencies gave such products. So the reality of the situation was that only the banks truly knew how risky these securities were.

FAQs on Asymmetric Information

Asymmetric information or information asymmetry is where one party in a transaction has more information than the other. In other words, the seller of a good may know more about its true worth than the consumer of that good.

Asymmetric information is caused by differences in information or knowledge better the buyer and seller in an economic transaction. As a result, there are higher costs associated with the transaction which leads to economic inefficiency.

One common example of asymmetric information is the second-hand car salesman. The salesman knows if there are any defects with the car such as faulty electrics, but the customer doesn’t. In turn, the customer is willing to pay more than they would otherwise, had they known about all the defects in the car.

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Market Share: Definition, Formula & Example - Market share refers to the percentage of a market a business owns, usually determined by its total revenue as a…

Market Share: Definition, Formula & Example - Market share refers to the percentage of a market a business owns, usually determined by its total revenue as a…  What Role Does Competition Play in International Trade - Competition plays a key role in promoting innovation, efficiency, and lower prices in international trade, benefitting both consumers and firms.

What Role Does Competition Play in International Trade - Competition plays a key role in promoting innovation, efficiency, and lower prices in international trade, benefitting both consumers and firms.