Arbitrage: Definition, Strategies & Examples

What is Arbitrage?

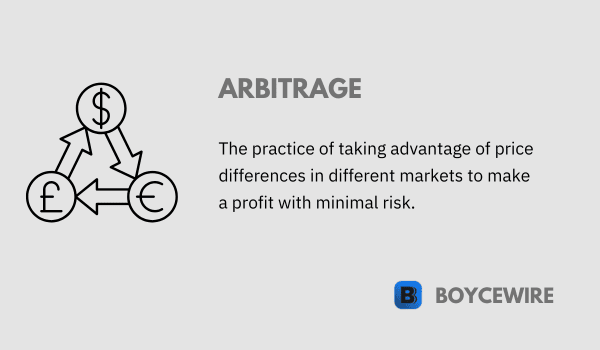

Arbitrage, a term derived from the French word ‘arbitrer’, meaning ‘to judge or arbitrate’, is a fundamental concept in financial markets. It refers to the simultaneous purchase and sale of the same or an equivalent asset or commodity from different markets to take advantage of a price discrepancy. Essentially, arbitrageurs buy a security at a lower price in one market and sell it at a higher price in another, thereby profiting from the price difference.

Key Points

- Arbitrage involves taking advantage of price differences in different markets to make a profit.

- It relies on the principle of buying low in one market and selling high in another.

- Arbitrage opportunities arise due to inefficiencies or temporary imbalances in pricing.

Understanding Arbitrage

1. Concept

At its core, arbitrage is a trading strategy that seeks to capitalize on price discrepancies in different markets or between different financial instruments. The primary objective of an arbitrageur (a person or entity engaging in arbitrage) is to identify these price discrepancies, execute trades simultaneously to profit from the difference, and do so with as little risk as possible.

2. The Basic Principles

The principle of arbitrage rests on the law of one price, which states that identical goods should sell for the same price in all locations. If this law isn’t holding true due to market inefficiencies, arbitrageurs can buy the cheaper good and sell it in the market where it’s priced higher. The simultaneous buy-sell action is important as it minimizes exposure to market risk. Over time, this activity should push prices back towards equilibrium across markets.

3. Types of Arbitrage

- Risk-Free Arbitrage This is the ideal form of arbitrage where the arbitrageur can make a profit with zero risk. It occurs when the same asset can be bought and sold simultaneously at different prices, leading to a risk-free profit.

- Risk Arbitrage Also known as merger arbitrage, this involves investing in securities of companies that are the target of a merger or acquisition. The risk lies in the possibility that the deal may not close, causing the price of the target company’s stock to fall.

- Statistical Arbitrage This form of arbitrage is based on complex mathematical modeling and predictions to identify trading opportunities. It often involves large quantities of securities and short time frames, and while it is not risk-free, it is designed to be low risk.

Arbitrage Strategies

Arbitrage strategies can vary significantly, and they often require complex mathematical calculations and a thorough understanding of financial markets. Fundamentally, the concept involves a trading strategy that aims to exploit inconsistencies in prices across different markets or financial instruments. The key objective of individuals or entities adopting this strategy is to identify these price discrepancies, conduct trades simultaneously to capitalize on the difference, and minimize risk to the best of their abilities.

1. Merger

Merger arbitrage, also known as risk arbitrage, is an investment strategy that capitalizes on the price discrepancies of merging companies. Typically, when a company announces its intention to buy another company, the stock price of the target company rises, while the acquiring company’s stock price may fall. An arbitrageur can profit by buying the stock of the target company and short selling the stock of the acquiring company. The risk in this strategy lies in the possibility of the merger or acquisition not going through.

2. Convertible Bond

This strategy involves buying a convertible bond and short selling the stock of the same company. A convertible bond is a bond that can be converted into a predetermined number of the company’s shares. When the price of the stock falls, the arbitrageur can profit from the short sale while still earning the bond’s interest. If the stock price rises, they can convert the bond into stock and benefit from the increased price. The risk here lies in the potential for the stock’s price to rise too high, causing a loss on the short sale that outstrips the profits from the bond’s conversion.

3. Long/Short Equity

This strategy involves taking a long position on an undervalued stock and a short position on an overvalued stock. Ideally, both stocks should be in the same sector or industry. The belief here is that market forces will eventually correct the mispricing, allowing the arbitrageur to profit from the convergence of the two stock prices.

4. Fixed Income

This strategy takes advantage of price differences in fixed income securities, such as bonds. For example, an arbitrageur might exploit price discrepancies between a Treasury bond and a bond issued by a corporation, or between a Treasury bond and an interest rate swap. The inherent risk in this strategy stems from the possibility that the price discrepancy might widen rather than narrow.

Role of Arbitrage in Efficient Markets

Arbitrage plays a pivotal role in the functioning of efficient financial markets. Here’s how:

1. Price Convergence

The primary function of arbitrage is to ensure that the same asset does not simultaneously trade at different prices in separate markets. If such a discrepancy occurs, arbitrageurs buy the asset in the lower-priced market and sell it in the higher-priced one, driving up the price in the lower-priced market and driving down the price in the higher-priced market. This action continues until the price difference has been eliminated. This process, known as price convergence, helps ensure that prices in different markets do not diverge significantly from each other over the long run.

2. Risk Reduction

Engaging in specific strategies, particularly those involving minimal risk, enables individuals to pursue profit opportunities. This is achieved by simultaneously buying and selling an asset, effectively eliminating the risk linked to holding the asset and being exposed to potential price fluctuations. As a result, such strategies can contribute to risk reduction in the financial markets.

3. Market Liquidity

By taking advantage of price differences in separate markets, arbitrageurs help ensure a higher level of activity within these markets. This increased activity contributes to the liquidity of the markets, making it easier for other traders and investors to buy and sell assets when they choose.

Risks and Limitations of Arbitrage

Despite the potential for profit, arbitrage is not without its risks and limitations. Here are some key points to consider:

1. Implementation Risk

One of the primary risks linked to certain trading strategies is the risk of implementation. This risk materializes when traders encounter challenges in promptly executing their trades to capitalize on price disparities. Considering the rapid movements of financial markets, the timeframe for taking advantage of such opportunities can be fleeting, thereby posing difficulties in timely trade execution.

2. Model Risk

Arbitrage strategies, particularly those related to statistical arbitrage, often rely on complex mathematical models to identify price discrepancies. If these models are based on incorrect assumptions or faulty data, they can lead to significant losses. This is known as model risk.

3. Market Risk

Even though arbitrageurs aim to reduce their exposure to market risk by executing their trades simultaneously, some level of market risk remains. For example, in merger arbitrage, there’s a risk that the merger or acquisition will not go through, leading to a drop in the stock price of the target company.

4. Regulatory Risk

Arbitrageurs must also be aware of regulatory risk. Financial markets are subject to laws and regulations that can change. Changes in financial regulations or tax laws could affect the profitability of arbitrage strategies.

Impact of Technology on Arbitrage

Technology has had a profound impact on arbitrage, reshaping the strategies used and the speed at which opportunities can be exploited.

1. Speed of Execution

With advancements in technology, transactions can now be completed in fractions of a second. High-frequency trading (HFT) uses complex algorithms to identify and exploit arbitrage opportunities almost instantaneously, leaving little room for human traders to compete.

2. Algorithmic Trading

Algorithmic trading, which employs computer programs to recognize patterns and execute trades, has become a key tool for arbitrageurs. These algorithms can process vast amounts of market data to identify arbitrage opportunities faster than human traders.

3. Globalization of Financial Markets

Technology has also facilitated the integration of financial markets around the world. Arbitrageurs can now easily execute trades in different markets across the globe, which has broadened the scope for arbitrage opportunities.

4. Decrease in Opportunities

While technology has certainly enhanced the ability to identify and exploit arbitrage opportunities, it has also led to a decrease in these opportunities. As algorithms quickly capitalize on price discrepancies, these discrepancies are corrected at an ever-increasing speed, meaning that they exist for shorter periods of time.

Examples of Arbitrage

Understanding arbitrage becomes easier with real-world examples. Here are a few cases that illustrate how it works in various contexts:

1. Stock Market

Suppose a stock is trading for $50 on the New York Stock Exchange (NYSE) and $50.05 on the London Stock Exchange (LSE). An arbitrageur could buy the stock for $50 on the NYSE and simultaneously sell the same stock for $50.05 on the LSE, making a profit of $0.05 per share (minus transaction costs).

2. Currency

Consider a situation where you can buy 1 euro for $1.20 in the U.S., 1 euro for 0.90 British pounds in the U.K., and 1 British pound for $1.25 in Canada. By starting with $1.20 in the U.S., you could buy 1 euro, exchange it for 0.90 British pounds in the U.K., and then exchange those pounds for $1.13 in Canada. This loop would net a profit of $0.07, constituting an arbitrage opportunity.

3. Sports Betting

In sports betting, different bookmakers often offer different odds for the same event. Suppose one bookmaker offers odds of 2.0 on Team A winning a game, while another offers odds of 2.0 on Team A not winning (either losing or drawing). By betting $100 on both outcomes with the two different bookmakers, no matter the result, the bettor will break even if Team A doesn’t win and make a $100 profit if Team A wins.

4. Retail

This form of arbitrage involves buying a product in one market at a low price and then selling it in another market where the price is higher. For instance, a seller might purchase a toy on clearance for $10 at a retail store and then sell it on an online marketplace for $25, netting a $15 profit before expenses.

FAQs

Arbitrage refers to the practice of buying and selling assets or securities in different markets to take advantage of price discrepancies and earn a risk-free profit.

Arbitrage involves simultaneously buying an asset at a lower price in one market and selling it at a higher price in another market, thereby exploiting the price difference and earning a profit.

The common types of arbitrage include spatial arbitrage (taking advantage of price differences across different geographic locations), temporal arbitrage (exploiting price differences that occur over time), and statistical arbitrage (using statistical models to identify and exploit price discrepancies).

While arbitrage is considered low-risk, there are still potential risks such as execution risk (inability to execute trades quickly and efficiently), market risk (unexpected price movements that erode profit margins), and regulatory risk (changes in regulations that impact opportunities).

About Paul

Paul Boyce is an economics editor with over 10 years experience in the industry. Currently working as a consultant within the financial services sector, Paul is the CEO and chief editor of BoyceWire. He has written publications for FEE, the Mises Institute, and many others.

Further Reading

Law of Demand: What it is, Examples & Diagram - The law of demand refers to how demand changes in reaction to price. So when prices rise, the law of…

Law of Demand: What it is, Examples & Diagram - The law of demand refers to how demand changes in reaction to price. So when prices rise, the law of…  Commercialization - Commercialization refers to the process of introducing a new product, service, or innovation into the market with the aim of…

Commercialization - Commercialization refers to the process of introducing a new product, service, or innovation into the market with the aim of…  Inferior Goods - Inferior goods are products or services that experience a decrease in demand as consumer income rises, typically due to the…

Inferior Goods - Inferior goods are products or services that experience a decrease in demand as consumer income rises, typically due to the…